European VC Valuations 2025: The AI Bubble Shows Cracks While Everyone Looks Away

European VC valuations 2025 tell a story that should concern every startup founder, investor, and board member paying attention. According to PitchBook’s 2025 Annual European VC Valuations Report, released in February 2026, the numbers look impressive on the surface: median valuations increased across all stages, down rounds hit near-record lows, and unicorn deal value doubled year-over-year. But beneath these headline figures lies a troubling reality that the industry seems eager to ignore.

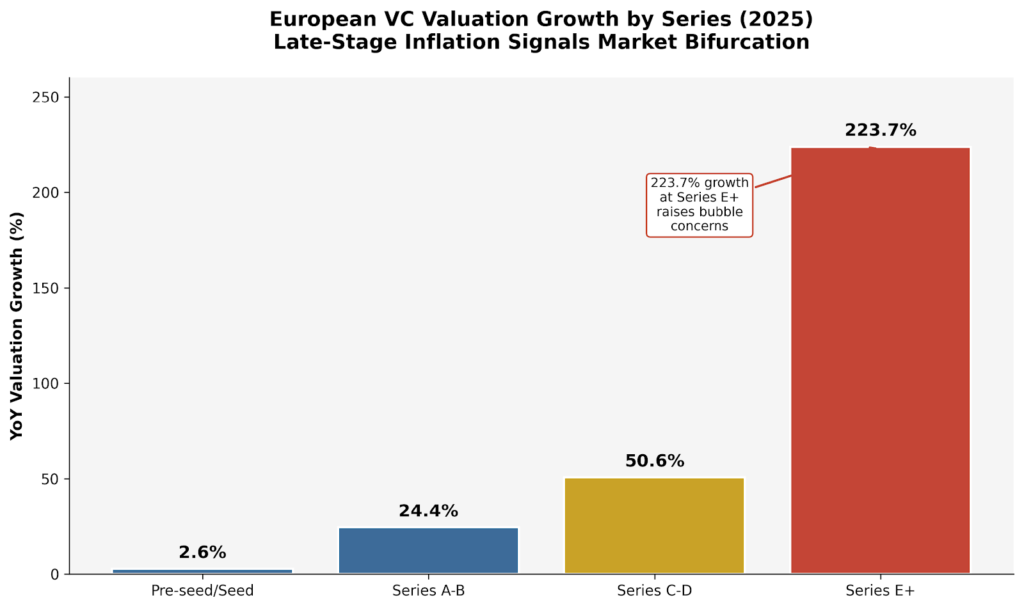

The data reveals a market increasingly bifurcated between AI-fueled late-stage excess and everything else struggling for air. While Series E+ valuations exploded by 223.7% to reach a median of €1.4 billion, pre-seed and seed valuations crawled up just 2.6%. This isn’t healthy growth—it’s the mathematical fingerprint of speculative capital chasing narrative rather than fundamentals.

The European VC Valuation Numbers That Should Keep You Up at Night

Let’s start with what PitchBook’s data actually shows about European VC valuations in 2025, because the devil is in the dispersion.

Figure 1: European VC valuation growth by series (2025) — Data source: PitchBook

The valuation step-ups tell a clear story of market stratification. At pre-seed and seed, the median valuation sits at €5 million—up a mere 2.6% year-over-year. Series A-B improved to €34.9 million (24.4% growth). Series C-D jumped 50.6% to €222.9 million. But Series E+ is where the music gets truly surreal: a 223.7% explosion to €1.4 billion median.

This pattern—muted growth at the bottom, exponential inflation at the top—isn’t a sign of a healthy ecosystem. It’s the signature of capital concentration driven by fear of missing out on AI, coupled with a severe shortage of viable exit paths forcing late-stage money to pile into an ever-narrower set of perceived winners.

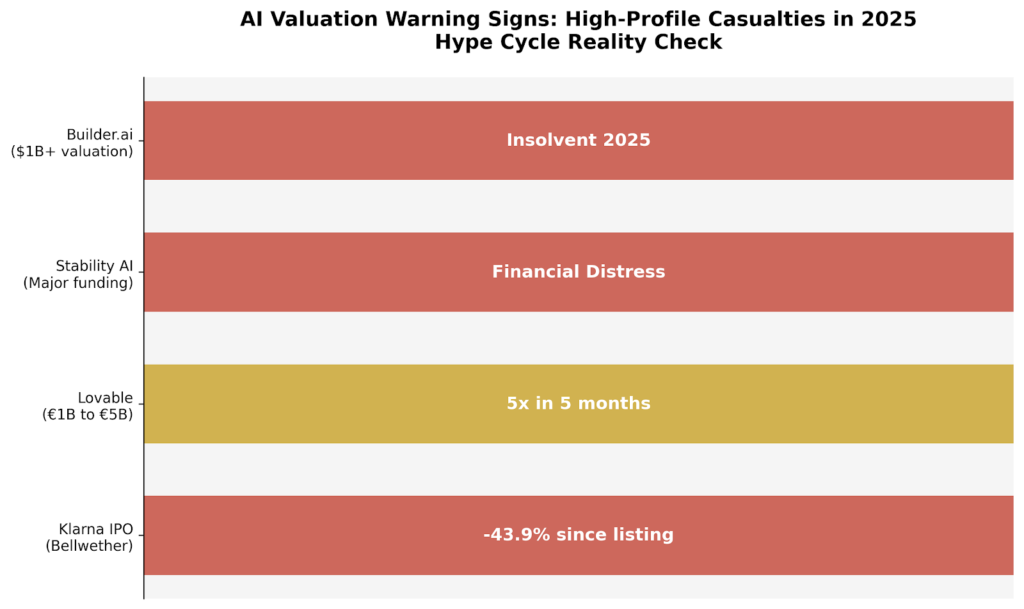

The AI Valuation Casualties Nobody Wants to Discuss

While the industry celebrates AI’s dominance in European VC valuations 2025, PitchBook’s report quietly documents the casualties that should serve as warning flares.

Figure 2: High-profile AI valuation casualties in 2025

Builder.ai, once valued at over $1 billion and backed by major institutional investors, became insolvent in 2025 following allegations of inflated revenues and overstated AI capabilities. The company’s collapse represents more than a single failure—it’s a case study in how AI narrative can paper over fundamental business problems until it suddenly can’t.

Stability AI, the developer behind Stable Diffusion that was once hailed as a European AI champion, has faced severe financial distress, leadership changes, and governance challenges—despite significant early funding. The company that was supposed to democratize AI image generation now serves as a cautionary tale about the gap between technical achievement and sustainable business models.

Then there’s Lovable, which exemplifies the speculative mania still gripping the market. The company’s valuation reportedly jumped from over €1 billion in July 2025 to over €5 billion by December—a 5x increase in roughly five months. As PitchBook notes, this occurred “during what many viewed as the ‘hype phase’ of the J curve.” History suggests that J curves eventually find their inflection point.

The Klarna Warning: When Bellwether IPOs Disappoint

Perhaps no data point better illustrates the gap between private and public market valuations than Klarna’s post-IPO performance. The Swedish fintech giant was supposed to validate years of private market pricing and restore confidence in the European tech exit environment.

Instead, as of late January 2026, Klarna’s share price was down 43.9% since its listing.

This isn’t an isolated case. PitchBook’s report notes that other high-profile 2025 listings—including US companies Hinge Health, CoreWeave, and Circle—all had to revise their valuations downward from their last private rounds at IPO. The message from public markets is clear: private market valuations, particularly for AI and tech companies, have overshot sustainable levels.

The European exit environment shows structural strain. Over the past three years, there have been 153 PE take-privates in Europe compared to just 55 IPOs. When private equity finds more value in buying public companies than public markets find in pricing private ones, something fundamental has broken in the capital formation cycle.

The Hidden Data Problem: What the Down Round Numbers Aren’t Telling You

European VC valuations 2025 data shows down rounds at near all-time lows—just 14.6% of deals, second only to 2022’s 13.5%. The industry has seized on this figure as evidence that the valuation reset is complete and the market has found its footing.

But PitchBook’s own analysis raises a critical caveat that deserves far more attention: “There is potentially some upward bias in the data, as the number of companies reporting valuations also significantly decreased (down 37.1% YoY), meaning those seeing step-downs may not be disclosing them.”

Read that again. The number of companies willing to report valuations dropped by more than a third. In a market where transparency is already limited, this selection bias suggests the true down round rate may be significantly higher than reported. Companies with good news share; companies with bad news go quiet.

This data opacity problem compounds when you consider that AI companies—which dominate late-stage deal flow—saw their down round rate decrease from 15.6% to 13.4%. Sounds positive until you realize these are precisely the companies with the strongest incentive to maintain valuation narratives for future fundraising and exit positioning.

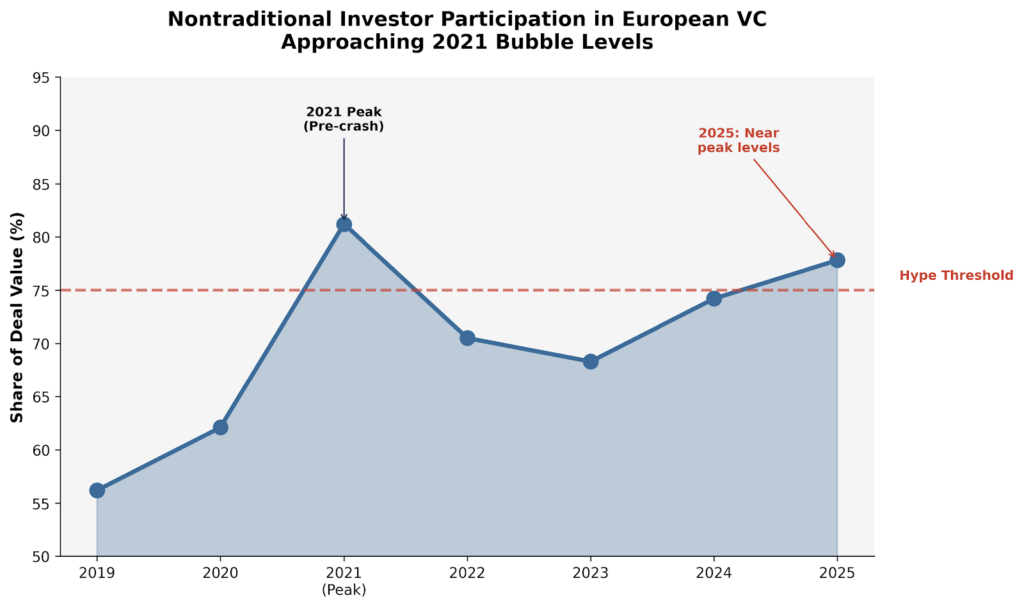

European VC Valuations 2025: The Nontraditional Investor Warning Signal

One of the most telling indicators in the 2025 data is the surge of nontraditional investor participation to 77.8% of deal value—approaching the 81.2% peak reached in 2021, just before the market correction began.

Figure 3: Nontraditional investor participation approaching bubble-era levels — Data source: PitchBook

PitchBook attributes this shift largely to AI: “We believe this shift has been driven largely by the growing presence of AI in Europe, where nontraditional investors have wanted to enter venture markets to gain exposure to the theme and technology.”

The numbers support this. Of the €31.6 billion in deal value with corporate venture capital (CVC) participation in 2025, over one-third (€11.9 billion) related to technologies with AI applications—more than double the prior year’s proportion.

When tourism-level capital chases a single theme with this intensity, valuations detach from fundamentals. Corporate strategics buying options on the future is rational behavior individually. Collectively, it creates the conditions for systemic mispricing that unwinds painfully when narrative shifts.

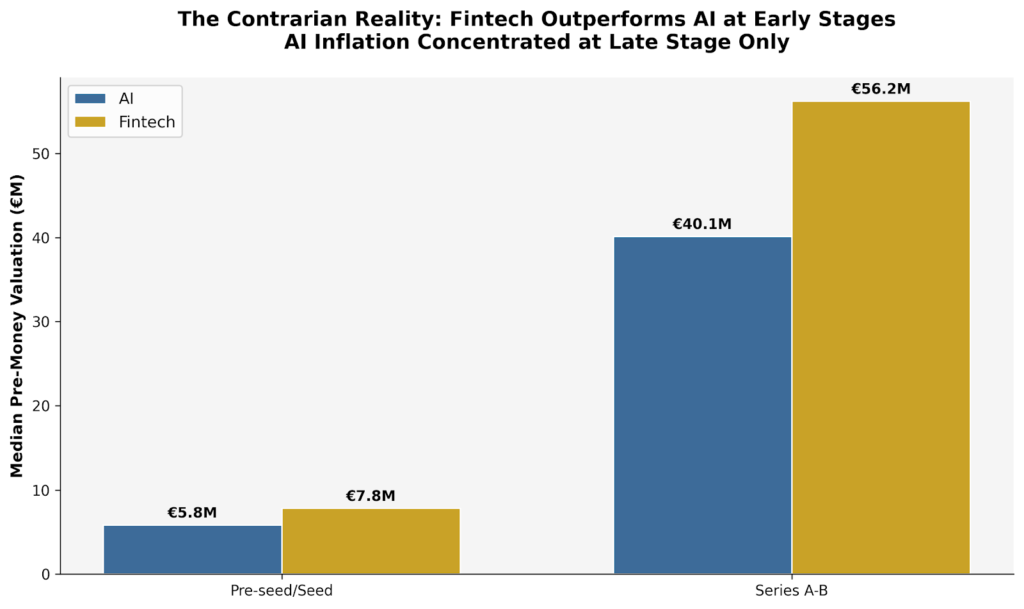

The Contrarian Reality: Where the Smart Money Isn’t Looking

Here’s what the AI hype obscures: at the stages where genuine company-building happens, AI isn’t even the top performer.

Figure 4: Fintech consistently outperforms AI at early stages — Data source: PitchBook

At pre-seed and seed, fintech median valuations reached €7.8 million—34% higher than AI’s €5.8 million. At Series A-B, fintech led at €56.2 million versus AI’s €40.1 million. The AI premium only materializes at Series C-D and beyond, precisely where speculative capital concentrates.

Meanwhile, cleantech—a sector with genuine long-term structural tailwinds—has been “crowded out by AI,” as PitchBook notes. Cleantech investment fell from fourth place by total euros to sixth in 2025. Down rounds in cleantech actually increased to 16.7% from 15.3%, making it one of the only sectors moving in the wrong direction.

This creates a contrarian opportunity. If you’re evaluating European VC opportunities, the unloved sectors trading at fundamental-based valuations may offer better risk-adjusted returns than the AI darlings commanding astronomical premiums that require perfect execution and continued narrative support to justify.

What PitchBook’s Own Analysts Are Warning

Credit to PitchBook for including explicit warnings in their own analysis. Their conclusion deserves direct quotation:

“Despite the resilience in valuations in the market, especially in the AI space, we still believe that there is a rationalisation to come for AI. In 2025, valuations within the space significantly increased during what many viewed as the ‘hype phase’ of the J curve.”

The report explicitly calls out the Builder.ai and Stability AI failures as indicators that “a need for valuation discipline and due diligence as the AI investment cycle moves past its early hype phase” exists. This isn’t contrarian analysis from the sidelines—it’s the data provider’s own assessment embedded in the report.

Looking ahead, PitchBook characterizes the European VC market as in a position of “conditional stability rather than broad-based strength.” Their 2026 outlook suggests the market will “test the sustainability of current pricing, particularly in non-AI sectors and earlier stages, where valuation support remains more sensitive to shifts in sentiment, capital availability, and the pace at which private market valuations are forced to converge with public benchmarks.”

A Practical Framework for Navigating European VC Valuations in 2025-2026

Based on this analysis, here’s how different stakeholders should approach European venture valuations:

For Startup Founders

- Avoid the valuation trap. Raising at inflated valuations creates downside risk when market sentiment shifts. Sustainable runway beats impressive paper valuations.

- Focus on fundamentals. With down rounds potentially underreported, companies with genuine unit economics and path to profitability will weather corrections better than narrative-dependent peers.

- Consider alternative sectors. Fintech’s early-stage premium over AI suggests the market still values proven business models over hype.

For Investors

- Apply enhanced due diligence to AI. Builder.ai’s collapse shows that major investors can miss fundamental business problems when narrative overpowers analysis.

- Watch the NTI signal. Nontraditional investor participation near 2021 peaks historically precedes corrections. This metric deserves monitoring.

- Exploit contrarian opportunities. Cleantech and other out-of-favor sectors may offer better risk-adjusted returns than consensus AI bets.

For Corporate Development and M&A

- Expect valuation gaps. The 43.9% Klarna decline and broader private-public valuation gap suggests acquisition targets may have unrealistic price expectations.

- Look for distressed opportunities. As the AI rationalisation unfolds, quality companies with unsustainable valuations may become available at reasonable prices.

- Use structure creatively. Earnouts, ratchets, and other structured elements can bridge valuation gaps while protecting against downside scenarios. For more on M&A structuring in volatile markets, see our guide to SaaS M&A due diligence frameworks.

The Bottom Line on European VC Valuations 2025

European VC valuations 2025 present a market that appears healthy in aggregate while exhibiting increasingly concerning structural dynamics. The 223.7% explosion in Series E+ valuations, concentrated AI exposure among nontraditional investors approaching bubble-era levels, and the growing gap between private and public market pricing all point to a correction that remains more a question of timing than possibility.

PitchBook’s own analysts expect this rationalisation. The market’s casualties—Builder.ai, Stability AI’s distress, Klarna’s post-IPO decline—demonstrate that it has already begun for some. The question facing every participant in European venture is whether they’re positioned for resilience when the broader correction arrives, or dependent on the continuation of conditions that increasingly resemble the end of a cycle rather than sustainable growth.

The data is there for anyone willing to look. The question is whether the industry is listening.

Related Reading: