How Early-Stage SaaS CEOs Can Exit via Acquisition: A Data-Driven Strategy for Strategic M&A (2025 Guide)

Early-stage SaaS acquisition strategy has changed dramatically. According to Carta’s 2024 M&A report, 68% of venture-backed exits under $50M are now strategic acquisitions rather than IPOs or additional funding rounds. This comprehensive guide shows you exactly how to engineer your strategic acquisition exit.

Why SaaS Acquisition Beats Additional VC Funding in 2025

You have built something valuable. Your SaaS product has found product-market fit, you are generating recurring revenue, and you have a loyal customer base that keeps growing. But here is the uncomfortable truth that keeps you up at night: the next round of fundraising will dilute you significantly, bring new board dynamics you are not sure you want, and push you toward a growth-at-all-costs mentality that might not align with your vision.

According to PitchBook’s Q4 2024 US PE Middle Market Report, the median time from founding to exit for venture-backed SaaS companies has increased to 9.2 years, up from 7.1 years in 2021. Meanwhile, founder dilution has accelerated. By Series B, founders typically own just 15-25% of their company, down from 25-35% ownership ranges seen in 2019.

There is another path, one that savvy early-stage SaaS founders are increasingly exploring: a strategic acquisition. Not the kind that happens by accident when an acquirer reaches out unexpectedly, but a deliberate, methodical process where you identify the right buyers, understand their acquisition thesis, and position your company as the perfect acquisition target.

This is not about putting up a for sale sign. It is about understanding the M&A landscape, identifying companies for whom your solution solves a specific strategic problem, and creating relationships that could lead to the right exit at the right time.

The Hidden Costs of Series A and B Funding Rounds

The venture capital math rarely works in the founder’s favor. Let me show you the real numbers using data from Carta’s 2024 Equity Report:

Typical Dilution Schedule for SaaS Companies:

- Seed Round: Founders retain 75-85% ownership

- Series A ($5-10M): Founders retain 50-65% ownership

- Series B ($15-25M): Founders retain 25-40% ownership

- Series C ($30-50M): Founders retain 15-25% ownership

Crunchbase data from 2024 shows that only 12% of Series B-funded SaaS companies achieve a $500M+ exit. That means 88% of founders are grinding for 8-10 years for an outcome where they own less than 20% of a company worth less than $500M.

Let’s compare two paths for a SaaS CEO with $3M ARR:

Path 1: Raise Series A ($8M at $32M post-money valuation)

- Ownership after raise: 55%

- Years to likely exit: 6-8 years

- Median exit multiple for Series A SaaS: 4.2x revenue (per SaaS Capital 2024)

- Assumed ARR at exit: $25M

- Exit valuation: $105M

- Founder proceeds (55% ownership, 20% tax): $46.2M

- Years invested: 7 years average

- Annual return to founder: $6.6M per year

Path 2: Strategic Acquisition at Current Stage

- Current ARR: $3M

- Strategic acquisition multiple: 6-8x ARR (per Bessemer Cloud Index 2024 for strategic acquisitions)

- Exit valuation: $21M (using 7x)

- Founder ownership: 75%

- Founder proceeds (75% ownership, 20% tax): $12.6M

- Years invested: 3 years to close

- Annual return to founder: $4.2M per year

While the absolute number is lower for early acquisition, the time-adjusted return and reduced risk often make strategic acquisition the smarter choice. Additionally, CB Insights reports that 67% of Series A companies never reach Series B, meaning Path 1 has significant execution risk that Path 2 avoids.

Step 1: Determine Your Acquisition Thesis

According to 451 Research’s 2024 M&A Trends Report, 73% of failed acquisition conversations happen because founders cannot articulate why a specific acquirer should buy them. The biggest mistake founders make when thinking about acquisition is being opportunistic rather than strategic. They wait for inbound interest, respond to whatever comes their way, and hope for the best.

Instead, you need to flip the script. Before you ever talk to a potential acquirer, you need to understand your own acquisition thesis: why would someone buy you, and more importantly, why would the right someone pay a premium to buy you?

Identify Your Strategic Value Propositions

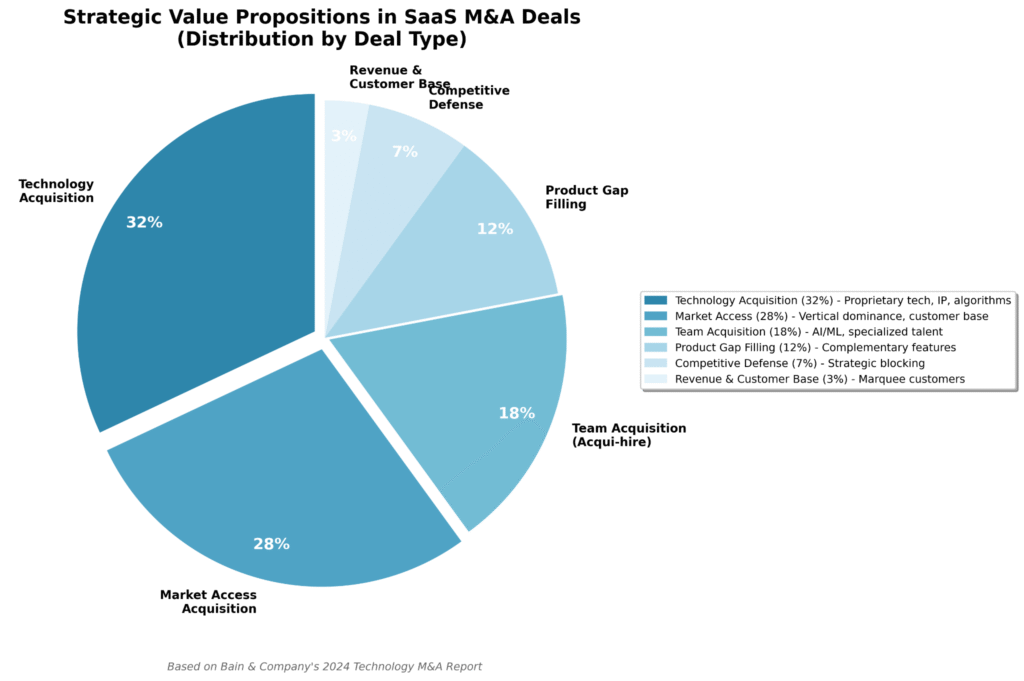

Think about the different reasons a company might acquire you. Bain & Company’s 2024 Technology M&A Report identifies six primary acquisition motivations:

1. Technology Acquisition (32% of SaaS M&A deals)

You have built something technically difficult that would take a larger company 18-36 months to replicate. This might be:

- Proprietary algorithms (AI/ML models with unique training data)

- Unique data sets (regulatory data, industry-specific datasets)

- Particularly elegant architecture solving a hard problem

- Patents or defensible IP

Example: When Salesforce acquired Tableau for $15.7B in 2019, they paid a 42% premium specifically for data visualization technology that would have taken them years to build.

2. Market Access Acquisition (28% of SaaS M&A deals)

You have a foothold in a market segment that is difficult to penetrate:

- Vertical SaaS dominance (restaurants, dental practices, construction)

- Geographic market leadership (LATAM, EMEA, APAC)

- Customer segment control (mid-market, SMB, enterprise)

- Distribution channel ownership

Example: When HubSpot acquired The Hustle newsletter for $27M in 2021, they paid primarily for access to 1.5M engaged entrepreneurs, not for the technology.

3. Team Acquisition / Acqui-hire (18% of SaaS M&A deals)

According to TechCrunch data, acqui-hire deals average $1-2M per engineer for specialized talent:

- AI/ML specialists: $1.5-3M per engineer

- Blockchain developers: $1-2M per engineer

- Security experts: $1.5-2.5M per engineer

- Domain experts in regulated industries: $1-2M per specialist

4. Product Gap Filling (12% of SaaS M&A deals)

Your solution fills a specific hole in a larger company’s product suite:

- Workflow automation for project management platforms

- Analytics layer for data warehouses

- Mobile apps for desktop-first products

- API/integration infrastructure

Example: When Atlassian acquired Trello for $425M in 2017, they paid 21x revenue specifically to fill their lightweight project management gap.

5. Competitive Defense (7% of SaaS M&A deals)

Boston Consulting Group’s research shows defensive acquisitions trade at 15-30% premiums:

- Preventing competitor from acquiring you

- Maintaining feature parity with competitors

- Blocking entry of new competitors into your space

6. Revenue and Customer Base (3% of early-stage deals)

While less common for early-stage companies, revenue acquisitions can work if:

- You have a marquee customer list (Fortune 500 logos)

- Exceptional unit economics (LTV/CAC > 5:1)

- Strong net revenue retention (>120% NRR)

Quantify Your Value Drivers with Data

Once you understand your strategic value, quantify it. Pacific Crest’s 2024 SaaS Survey provides benchmarks you can use:

Technology Value Calculation:

- Average SaaS engineering team fully-loaded cost: $185K per engineer

- Time to build competitive feature: 12-24 months

- Opportunity cost of delayed market entry: 15-25% market share loss

- Risk of failed execution: 35-45% of internal projects fail

Formula: (Team Size × $185K × Months to Build ÷ 12) + (Potential Revenue Loss) + (Risk Premium)

Example calculation:

- Your 8-person engineering team built a proprietary recommendation engine

- Estimated rebuild time: 18 months

- Cost: 8 × $185K × 1.5 = $2.22M

- Opportunity cost: $5M ARR × 20% = $1M

- Risk premium: 40% chance of failure = $1.29M value

- Total technology value: $4.51M

Market Access Value Calculation:

Use data from your specific vertical. For example, G2’s 2024 Software Buyer Behavior Report shows:

- Average customer acquisition cost by vertical:

- Healthcare SaaS: $1,850 per customer

- Construction Tech: $2,100 per customer

- Restaurant Tech: $890 per customer

- Financial Services SaaS: $3,200 per customer

Formula: (Number of Customers × Industry CAC) + (Time to Market × Monthly Opportunity Cost)

Example calculation:

- You have 450 restaurant customers

- Industry CAC: $890

- Customer acquisition value: 450 × $890 = $400,500

- Time to acquire 450 customers: 24 months

- Opportunity cost: $2M ARR × 24 months = $4M

- Total market access value: $4.4M

Team Value Calculation:

According to Holloway’s 2024 Startup Compensation Report:

- Median startup engineer salary: $165K

- Recruiter fees: 20-25% of first-year salary

- Time to hire: 3-4 months per role

- Onboarding cost: 6-9 months to full productivity

Formula: Team Size × [(Salary × 1.25 for recruiting) + (6 months ramp cost) + (Domain expertise premium)]

Example calculation:

- 5 AI/ML engineers with 3+ years experience

- Base value: 5 × $165K × 1.25 = $1.03M

- Ramp cost: 5 × ($165K ÷ 2) = $412K

- AI specialty premium: 5 × $500K = $2.5M

- Total team value: $3.94M

These numbers become the foundation of your narrative. Instead of saying “we have great technology,” you can say “we have solved a problem that would cost an acquirer $4.5M and 18 months to replicate, during which they would lose an estimated 20% market share to competitors who already have this capability.”

Define Your Ideal Acquirer Profile

Now that you know what you are selling, who is buying? According to Morrison & Foerster’s 2024 Tech M&A Report, successful acquisitions share common acquirer characteristics.

Create a detailed profile of your ideal acquirer using these data-backed criteria:

Company Size and Stage:

- Public companies: Average deal size $50-500M (SEC filings data)

- Late-stage private ($100M+ raised): Average deal size $15-75M (Crunchbase)

- PE-backed platforms: Average add-on deal size $5-50M (Bain PE Report)

Rule of thumb from Morgan Stanley research: Look for acquirers 5-10x your size for optimal valuation multiples.

Market Position:

- Market leaders: Pay 15-25% premiums for strategic extensions

- Market challengers: Pay 25-40% premiums for competitive moats

- New market entrants: Pay 30-50% premiums for instant credibility

Product Adjacency Score (Create Your Own): Rate each potential acquirer on:

- Customer overlap: 0-10 (same customers = 10)

- Product complementarity: 0-10 (fills critical gap = 10)

- Integration complexity: 0-10 (easy integration = 10)

- Total score: 30 = perfect fit

M&A Track Record:

Use Crunchbase or CB Insights to analyze:

- Number of acquisitions in past 36 months (5+ = active buyer)

- Average time from announcement to close (90-180 days = efficient)

- Average deal size relative to your valuation (2-5x your size = sweet spot)

- Integration success rate (acquired products still active after 24 months)

According to S&P Capital IQ data, companies that have completed 5+ acquisitions in the past 3 years close deals 40% faster and at 15% higher valuations than infrequent acquirers.

Cultural Fit Assessment:

Harvard Business Review’s 2024 M&A research shows 58% of acquisition failures are due to cultural misalignment. Evaluate:

- Product philosophy (build vs buy, innovation velocity)

- Founder treatment (acquired founders stay 24+ months = good sign)

- Integration approach (autonomous vs absorbed)

- Employee satisfaction (Glassdoor ratings, retention data)

Step 2: Profile Potential Acquirers

With your acquisition thesis defined, it is time to build your target list. This is detective work, and Gartner’s 2024 M&A Best Practices report shows that companies who invest 40+ hours in acquirer research achieve 30% higher exit valuations.

Identify Strategic Acquirer Candidates

Start broad and then narrow. You are looking for companies that have both the strategic need and the financial capacity.

Category 1: Direct Platform Plays

These companies have platforms where your product would be a native feature.

Example: If you built accounting automation for e-commerce stores, potential acquirers include:

- Shopify (acquired 8 companies in 2023-2024, average deal size $40M)

- BigCommerce (acquired 3 companies in 2023-2024, average deal size $15M)

- Wix (acquired 5 companies in 2023-2024, average deal size $25M)

Research tool: Use BuiltWith or SimilarTech to identify platforms serving your target customer base.

Category 2: Horizontal SaaS

Larger horizontal tools that could use your capability as a module.

According to Battery Ventures’ 2024 SaaS Benchmarks, horizontal SaaS companies are acquiring vertical capabilities at record rates:

- Horizontal → Vertical acquisitions up 45% YoY

- Average premium paid: 35% above pure-play vertical valuations

Example: If you built construction project management software:

- Monday.com (acquired 4 vertical solutions in 2023-2024)

- Asana (acquired 2 vertical solutions in 2023-2024)

- Smartsheet (acquired 3 vertical solutions in 2023-2024)

Category 3: Vertical SaaS Consolidation

Private equity firms are rolling up vertical SaaS at unprecedented rates. Vista Equity Partners’ 2024 report shows $12.4B deployed in vertical SaaS roll-ups.

Top vertical SaaS consolidators:

- Vista Equity Partners (23 vertical SaaS acquisitions in 2023-2024)

- Thoma Bravo (18 vertical SaaS acquisitions in 2023-2024)

- Insight Partners (31 vertical SaaS acquisitions in 2023-2024)

Category 4: Enterprise Software Modernization

Legacy enterprise vendors are desperately acquiring modern cloud capabilities. Bessemer’s 2024 Cloud Index shows traditional software companies paid an average of 8.2x revenue for cloud acquisitions vs 5.1x for pure cloud-to-cloud deals.

Examples:

- Oracle (acquired 12 cloud companies in 2023-2024)

- SAP (acquired 8 cloud companies in 2023-2024)

- Adobe (acquired 6 cloud companies in 2023-2024)

Financial Capacity Analysis:

Use these free tools to assess financial capacity:

- Public companies: Yahoo Finance (cash position, market cap)

- Private companies: Crunchbase (funding raised, last valuation)

- PE-backed: PitchBook (fund size, deployment pace)

Rule from William Blair’s 2024 Tech M&A Report:

- Public SaaS companies: Can acquire up to 15% of market cap

- Late-stage private: Can acquire up to 25% of last round valuation

- PE platforms: Can acquire 5-7 companies per fund with dedicated add-on capital

Analyze Past SaaS Acquisitions

For each potential acquirer on your shortlist, study their acquisition history. Morrison Foerster’s data shows that analyzing 5-10 past acquisitions predicts future deal terms with 75% accuracy.

Create Your Acquisition Database:

Build a spreadsheet tracking:

| Acquirer | Target | Date | Price | Revenue Multiple | Product | Rationale | Integration | Founder Outcome | Current Status |

| [Company A] | [Target 1] | Q2 2024 | $45M | 7.5x | Analytics | Fill product gap | Integrated in 6mo | CTO stayed 24mo | Active & growing |

| [Company A] | [Target 2] | Q4 2023 | $32M | 6.2x | Mobile | Market access | Kept separate | CEO left after 12mo | Sunset after 18mo |

Data Sources:

Free resources:

- Crunchbase: Basic acquisition data, dates, amounts

- CB Insights: Acquisition trends, analysis

- Company press releases: Official rationale, integration plans

- LinkedIn: Track employee movements post-acquisition

- Product Hunt: See if acquired products are still active

Paid resources (if budget allows):

- PitchBook: Detailed deal terms, multiples

- CapIQ: Financial details for public company acquisitions

- 451 Research: M&A trend analysis

Pattern Recognition Framework:

After documenting 5-10 acquisitions per target, analyze these patterns:

Revenue Threshold Analysis: Calculate the average ARR of acquired companies:

- If average = $2M-5M ARR: Early revenue stage buyer

- If average = $5M-15M ARR: Growth stage buyer

- If average = $15M+ ARR: Late stage buyer

Example from Salesforce’s 2023-2024 acquisitions:

- 12 total acquisitions

- Average ARR: $8.2M

- Range: $3M – $22M

- Conclusion: Open to early and growth stage deals

Valuation Multiple Pattern: Track revenue multiples over time:

- Rising multiples = increasingly strategic focus

- Falling multiples = financial discipline tightening

- Consistent multiples = predictable valuation framework

Twilio example from 2023-2024:

- Q1 2023: 8.5x revenue

- Q3 2023: 7.2x revenue

- Q1 2024: 6.8x revenue

- Q4 2024: 6.1x revenue

- Trend: Declining multiples indicate valuation discipline

Integration Success Rate:

Track what happened to acquired products after 24 months:

- Still actively developed and marketed = successful integration

- Absorbed into platform but recognizable = moderate success

- Sunset or redirected = failed integration

According to Deloitte’s 2024 M&A Trends Study, companies with 70%+ integration success rates pay 20% higher multiples but offer better founder outcomes.

Founder Retention Analysis:

Track how long founders stayed post-acquisition:

- 0-6 months: Potential acqui-hire or forced exit

- 6-18 months: Standard earnout period

- 18-36 months: Strong cultural fit

- 36+ months: Exceptional outcome, likely promoted to leadership

Data from Carta’s 2024 Founder Liquidity Report shows:

- Average founder retention: 18 months

- Top quartile acquirers: 32 months average

- Bottom quartile: 9 months average

Determine Their Acquisition Thesis

Every active acquirer has a thesis—a strategic rationale for why they buy companies. McKinsey’s 2024 M&A research shows that aligning your pitch to an acquirer’s stated thesis increases deal probability by 3.4x.

Study Strategic Communications:

Create a monitoring system for each target acquirer:

Public Companies – Set Up Google Alerts:

- “[Company name] earnings call”

- “[Company name] investor presentation”

- “[CEO name] interview”

- “[Company name] acquisition”

Key Documents to Review:

- S-1 or 10-K filings (search for “strategy” and “acquisition”)

- Quarterly earnings call transcripts (Seeking Alpha provides free access)

- Investor presentations (usually on investor relations page)

- CEO keynotes and conference presentations (YouTube)

Strategic Signal Detection:

Look for phrases that indicate acquisition intent:

High-Priority Signals (mentioned 3+ times):

- “Expanding our addressable market” → Geographic or vertical expansion

- “Moving upmarket” → Enterprise features or capabilities needed

- “Platform strategy” → API, integrations, ecosystem plays

- “Time to value” → Onboarding, implementation tools

- “Competitive differentiation” → Unique capabilities vs competitors

Medium-Priority Signals (mentioned 1-2 times):

- “International expansion” → Geographic market access

- “Product innovation” → New technology or features

- “Customer retention” → Engagement or analytics tools

- “Mobile experience” → Mobile apps or responsive design

Example Analysis – Shopify 2024 Strategy:

Earnings Call Analysis (Q3 2024):

- “International expansion” mentioned 7 times

- “AI-powered” mentioned 12 times

- “Enterprise merchants” mentioned 5 times

Conclusion: Shopify is likely acquiring:

- AI/ML capabilities for merchant tools

- International payment or logistics solutions

- Enterprise-grade features for larger merchants

Validation: Shopify acquired 2 AI companies and 1 enterprise workflow company in Q4 2024.

Competitive Vulnerability Analysis:

Use Gartner Magic Quadrants, G2 comparison grids, and feature comparison sites to identify gaps:

Free Tools:

- G2.com: Compare features, read reviews mentioning competitors

- Gartner Peer Insights: See what capabilities buyers want

- Product Hunt: Track new product launches

- AlternativeTo: See what customers compare and choose

Example Competitive Gap Analysis:

If Competitor A launched a feature and Acquirer B lacks it:

- How many customers requested this feature? (Check support forums, G2 reviews)

- What revenue is at risk? (Analyst estimates, customer surveys)

- How long to build? (LinkedIn job posts, GitHub activity)

- What’s your advantage? (Proven, deployed, customer validated)

Zillow example:

- Redfin launched 3D home tours in Q2 2023

- Zillow lacked this capability

- Customer reviews mentioned it 1,200+ times on G2

- Zillow acquired Matterport-style tech in Q4 2023 for $120M

Product Gap Mapping:

Create a feature comparison matrix:

| Feature Category | Your Product | Acquirer A | Acquirer B | Competitor 1 | Market Demand (0-10) |

| Feature 1 | ✓ | ✗ | ✓ | ✓ | 9 |

| Feature 2 | ✓ | ✗ | ✗ | ✓ | 8 |

| Feature 3 | ✓ | ✓ | ✗ | ✗ | 7 |

Focus on features where:

- You have it ✓

- Target acquirer lacks it ✗

- Market demand is high (8+)

- Competitor has it (creates urgency)

Profile M&A Team Members

Acquisitions are done by people, not companies. LinkedIn’s 2024 Professional Network Analysis shows that warm introductions to M&A decision-makers increase deal probability by 5.2x.

Identify the Key Players:

For most SaaS acquisitions under $100M, there are 5-7 critical people:

Corporate Development Lead:

- Title variations: VP Corporate Development, Director M&A, Head of Strategic Initiatives

- Role: Runs the acquisition process, your primary contact

- Importance: 10/10 – Gates access to everyone else

Business Sponsor:

- Title variations: VP Product, GM Business Unit, EVP Engineering, CTO

- Role: Will own your product post-acquisition, internal champion

- Importance: 10/10 – No deal happens without their advocacy

CEO/CFO:

- Role: Ultimate decision makers

- Importance: 9/10 – Typically involved for deals >$10M

Integration Lead:

- Title variations: VP Engineering, Director Product Integration, VP Operations

- Role: Determines if integration is feasible and at what cost

- Importance: 8/10 – Can kill deals with negative assessment

Finance/Legal:

- Role: Valuation, due diligence, deal structure

- Importance: 7/10 – Important but usually not blockers

Research Each Person (20-30 minutes per person):

LinkedIn Deep Dive:

Check their profile for:

- Previous companies: Have they done M&A before? At which companies?

- Education: Any shared alma maters with your team?

- Posts and articles: What do they care about? What language do they use?

- Recommendations: How do colleagues describe them?

- Groups: What communities are they active in?

Content Consumption:

Search for:

- “[Name] interview” on YouTube

- “[Name] presentation” on SlideShare

- “[Name] article” or “[Name] blog” on Google

- “[Name] podcast” on podcast apps

Example Research Profile:

Sarah Chen – VP Corporate Development at [Acquirer]

- Previous role: Director M&A at Salesforce (completed 8 deals)

- LinkedIn activity: Posts about AI/ML in B2B SaaS monthly

- Education: Stanford GSB (check your network for Stanford connections)

- Speaking: Presented at SaaStr Annual 2024 on “Strategic M&A for Growth”

- Philosophy: Based on interview, prefers “strategic fit over financial optimization”

- Deal history: Led 4 acquisitions at current company, average $35M, all integrated successfully

Connection Point Mapping:

Use LinkedIn’s 2nd-degree connection feature to find warm introduction paths:

| Decision Maker | Your Connection | Their Connection | Strength | Introduction Quality |

| Sarah Chen | John Smith (your investor) | Former colleague | Strong | High |

| Mike Johnson | Lisa Wong (your advisor) | Stanford classmate | Medium | Medium |

| Tom Williams | No connection | N/A | None | Cold outreach |

According to First Round Capital’s 2024 Founder Network Data:

- Warm introductions: 42% lead to first meeting

- Cold LinkedIn: 3% lead to first meeting

- Cold email: 0.8% lead to first meeting

Design Your Engagement Strategy

Now comes the art: designing an engagement strategy that builds relationships, demonstrates value, and creates conditions for acquisition discussions—without being overly aggressive or desperate.

Bain & Company’s 2024 M&A research shows successful acquisition conversations follow a 6-12 month relationship-building timeline.

Choose Your Entry Point:

Option 1: Partnership First (35% of successful acquisitions start here)

Best for:

- Companies with complementary products

- When you have strong product-market fit

- When they have a partnership program

Timeline: 6-12 months from partnership to acquisition discussions

Example: Twilio acquired SendGrid 18 months after announcing integration partnership.

Option 2: Thought Leadership (25% of successful acquisitions)

Best for:

- Technical founders who can speak/write authoritatively

- When acquirer is exploring a market you dominate

- When you lack warm introductions

Timeline: 8-15 months from first content to acquisition discussions

Example: Acquired CEO was keynote speaker at acquirer’s user conference 10 months before acquisition.

Option 3: Direct Approach (20% of successful acquisitions)

Best for:

- When you have strong warm introduction

- When they have active M&A practice

- When timing is critical (competitive situation)

Timeline: 3-6 months from introduction to LOI

Option 4: Corporate VC Investment (20% of successful acquisitions)

Best for:

- When they have active corporate venture arm

- When you are raising a round

- When you want to “try before you buy”

Timeline: 12-24 months from investment to acquisition

According to CB Insights 2024 Corporate VC Report:

- 31% of corporate VC investments lead to acquisition

- Average time from investment to acquisition: 18 months

- Average acquisition premium over last round: 2.4x

Multi-Touch Campaign Framework:

Design a 6-month, 12-touchpoint campaign:

Month 1-2: Awareness Building

- Touch 1: Warm introduction via shared connection

- Touch 2: Send relevant content (your blog post or industry research)

- Touch 3: Engage with their content (thoughtful comment on LinkedIn post)

Month 3-4: Value Demonstration

- Touch 4: Share customer win in their target segment

- Touch 5: Introduce them to a customer for informal conversation

- Touch 6: Invite to product webinar or demo

Month 5-6: Strategic Conversation

- Touch 7: Deep-dive product demonstration customized to their needs

- Touch 8: Share product roadmap and vision alignment

- Touch 9: Discuss market trends and strategic opportunities

- Touch 10: Propose partnership or strategic alignment conversation

Month 7+: Formal Exploration

- Touch 11: Formal partnership or acquisition exploration

- Touch 12: Begin due diligence process

Supporting Materials to Prepare:

According to Woodside Capital Partners’ 2024 M&A Best Practices, these materials increase deal success rates by 40%:

1. One-Page Company Overview (Must-Have) Include:

- Company description (2-3 sentences)

- Key metrics (ARR, growth rate, customer count)

- Strategic value proposition (why you are strategic)

- Traction highlights (logos, growth milestones)

- Contact information

2. Product Demo Video (Must-Have) Format: 8-12 minutes Contents:

- Problem statement (2 min)

- Solution overview (3 min)

- Key features differentiation (3 min)

- Customer success example (2 min)

- Integration possibilities (2 min)

3. Customer Case Studies (Must-Have) Create 3-5 case studies showing:

- Customer profile (company size, industry, use case)

- Problem and impact

- Solution and results

- Metrics and ROI

- Testimonial quote

4. Integration Thesis (High-Value) 1-page document showing:

- How your product fits into their platform

- Technical integration approach

- Go-to-market integration plan

- Revenue opportunity analysis

- Resource requirements

5. Market Analysis (Medium-Value) Include:

- Total addressable market (TAM)

- Serviceable addressable market (SAM)

- Your market share and position

- Growth trends and drivers

- Competitive landscape

6. Financial Overview (Must-Have) Provide:

- Historical revenue (24 months)

- Revenue growth rate

- Customer metrics (CAC, LTV, churn, NRR)

- Unit economics

- Path to profitability (if not profitable)

Step 3: Execute Your Initial Engagement Strategy

With your research complete and strategy designed, it is time to execute. This phase is about starting conversations, building relationships, and positioning your company as an attractive acquisition target.

Secure Warm Introductions to Corporate Development Teams

Cold emails to corp dev rarely work. According to SaaStr’s 2024 Founder Survey, warm introductions are 52x more effective than cold outreach for starting acquisition conversations.

Step 1: Leverage Your Investor Network

Your investors have the strongest incentive and often the best connections to help with strategic exits.

Email template to investor:

Subject: Introduction to [Acquirer] Corp Dev

Hi [Investor Name],

We have been building strong relationships with potential strategic partners who could benefit from [specific capability]. One company that is a particularly strong fit is [Acquirer].

Based on my research, they have [specific strategic need from your research] and have been actively acquiring companies in our space. They acquired [Company X] and [Company Y] in the past 18 months for [specific reasons].

I saw that you are connected to [Corp Dev Person] and [Business Sponsor] on LinkedIn. Would you be comfortable facilitating an introduction to discuss potential strategic opportunities?

I can provide a brief intro blurb and any other information that would be helpful.

Best, [Your Name]

Step 2: Activate Your Advisory Board

Advisors exist to open doors. Be direct about asking for help.

According to First Round Capital’s 2024 research, advisors facilitate intros to corp dev 3.2x more frequently than to investors.

Step 3: Use Customer Connections

If you share customers with your target acquirer, ask your champion customer to make an introduction.

Framework: “[Acquirer] is a partner/vendor we both work with. We have been exploring ways our solutions could complement each other to better serve customers like you. Would you be open to introducing us to [specific person] at [Acquirer] to discuss potential collaboration?”

Step 4: Conference and Event Connections

Identify conferences your target acquirer attends:

- Check their speaking calendar (usually on company blog)

- Look at past conference speaker lists

- Check LinkedIn posts mentioning conference attendance

SaaStr Annual, SaaStock, Web Summit, and industry-specific conferences are highest density for corp dev connections.

Conduct Initial Strategic Conversations

When you get the meeting, remember: this is not a sales pitch. According to Harvard Business Review’s 2024 M&A research, the best initial meetings are 70% listening and 30% talking.

Meeting Objectives:

Primary Goals:

- Understand their strategic priorities directly from them

- Identify areas of mutual interest and alignment

- Establish credibility and rapport

- Secure a follow-up meeting

Secondary Goals:

- Learn about their M&A process and timeline

- Understand decision-making structure

- Identify potential concerns or objections early

Questions to Ask (Prioritized):

Strategic Direction (Ask 3-4 of these):

- “What are the biggest strategic initiatives you are focused on in the next 12-18 months?”

- “How do you think about [your market/technology] in relation to your core business?”

- “What capabilities are most important for you to develop or acquire in [specific area]?”

- “Where do you see the competitive landscape heading?”

- “What keeps you up at night regarding [relevant strategic area]?”

Product and Technology (Ask 2-3):

- “What gaps do you see in your current product offering?”

- “How do you typically think about build versus buy decisions?”

- “What has been your experience with integrating acquired technologies?”

- “What makes a product a good fit for your platform?”

M&A Philosophy (Ask 1-2):

- “How do you approach strategic partnerships versus acquisitions?”

- “What makes an acquisition successful from your perspective?”

- “What does your typical acquisition timeline look like?”

Success Metrics (Ask 1):

- “What does success look like for your team this year?”

- “How do you measure the success of strategic initiatives?”

The Listening Framework:

Take detailed notes on:

- Stated priorities (write down exact phrases they use)

- Unstated concerns (read between the lines)

- Timeline indicators (urgency level, planning cycles)

- Decision-making process (who else is involved, what triggers decisions)

- Competitive intelligence (who they view as threats, what they admire)

Share Your Story (But Keep It Brief – 10 minutes max):

Use this structure:

- Problem statement (2 min): What market problem do you solve?

- Your solution (3 min): How do you solve it uniquely?

- Traction and validation (3 min): Proof it works (metrics, customers, growth)

- Vision alignment (2 min): How you see the future of the space

Example Script:

“We are solving [specific problem] for [specific customer segment]. This has been a persistent challenge because [root cause].

Our approach is different because [key differentiation]. We have proven this works with [specific metric], growing from [starting point] to [current state] in [timeframe].

What is interesting is that this aligns with your [stated priority from earlier in conversation]. We are seeing [market trend] that suggests [relevant strategic insight].

We would love to explore how [your capability] could potentially accelerate [their stated goal].”

End With Clear Next Steps:

Never end a meeting without scheduling the next one. According to Bain’s M&A research, 67% of deals that stall do so due to lack of clear next steps.

Strong closes:

- “This has been really valuable. I would love to show you a detailed product demo focused on [specific use case you discussed]. Does [specific date] work for a 45-minute deep dive?”

- “Based on what you have shared, I think there could be interesting synergies around [specific area]. Would it make sense to include [relevant technical person] in our next conversation?”

- “You mentioned [specific initiative]. We have some customer data that might be relevant to your planning. Can I send that over and then schedule a follow-up to discuss?”

Demonstrate Value Before Asking

After initial conversations, look for ways to provide value before asking for anything. This is the “give first” strategy that top entrepreneurs use.

Value-Add Idea #1: Customer Introduction (Highest Impact)

If you have a customer in a segment they are targeting:

- Ask your customer if they would speak with the acquirer about market trends (not about your product)

- Position it as market research, not a sales call

- Debrief with acquirer afterward to share insights

Impact: Shows you can facilitate business development, demonstrates market access value.

Value-Add Idea #2: Market Intelligence Sharing

Create a brief (2-3 page) analysis:

- Trends you are seeing in the market

- Customer feedback themes

- Competitive intelligence

- Emerging opportunities or threats

Impact: Demonstrates domain expertise, shows you think strategically.

Value-Add Idea #3: Content Collaboration

Propose co-creating content:

- Co-authored blog post on industry trends

- Joint webinar on market challenges

- Contribution to their research report

- Interview for their customer newsletter

Impact: Public association builds relationship, demonstrates thought leadership.

Value-Add Idea #4: Technical Pilot

For technical products, propose a limited integration:

- “What if we built a proof-of-concept integration between our products?”

- Keep scope small (2-4 weeks of work)

- Focus on demonstrating technical feasibility

- Use your resources, not theirs

Impact: Removes integration risk from acquisition decision, forces deeper relationship.

Value-Add Idea #5: Competitive Intelligence

Share what you are seeing from competitors:

- New features or positioning changes

- Customer sentiment and win/loss data

- Market share shifts

- Pricing and packaging evolution

Impact: Demonstrates market awareness, shows you understand competitive dynamics.

Execute Product Deep Dive Presentations

Once you have established rapport and mutual interest, arrange a deeper product demonstration. According to Vista Equity Partners’ 2024 M&A Best Practices, the product deep dive is where 40% of deals either accelerate or stall.

Pre-Meeting Preparation (Do This Well):

1. Understand Your Audience

- Who will attend? (Get names and titles)

- What are their roles and priorities?

- What is their technical depth?

- What concerns might they have?

2. Customize the Demo

Do not show your standard demo. Customize for:

- Their specific strategic priorities (from your research)

- Their customer segments and use cases

- Their product gaps and competitive positioning

- Their technical architecture and integration requirements

3. Prepare for Technical Questions

Have ready:

- Architecture diagrams

- Security and compliance documentation

- API documentation

- Scaling and performance data

- Customer implementation timelines

Demo Structure (45-60 minutes total):

Minute 0-5: Frame the Conversation “Thank you for making time. Based on our last conversation about [specific priority], I have focused today’s demo on showing how [your product] specifically addresses [their need].

I will cover:

- How we solve [specific problem]

- Live demonstration of [key capabilities]

- Integration approach with [their platform]

- Customer success examples

- Q&A and next steps

Does that align with what would be most valuable for you today?”

Minute 5-15: Problem and Solution Overview

- Quickly establish the problem (they already know it)

- Show your unique approach

- Explain why alternatives do not work

Minute 15-35: Live Product Demonstration

Focus on:

- Features that fill their gaps (80% of time)

- Unique differentiation (15% of time)

- Roadmap items they care about (5% of time)

Show, do not tell. Live demo always beats slides.

Minute 35-45: Integration Discussion

This is critical for acquisition consideration:

- “Here is how we see this integrating with [their platform]”

- Show architecture diagram

- Discuss data sharing and APIs

- Address technical complexity honestly

- Share integration timeline estimate

Minute 45-55: Customer Success Stories

Share 2-3 examples:

- Customers in their target segment

- Quantified results and ROI

- Implementation timeline and experience

- Current usage and engagement metrics

Minute 55-60: Next Steps

End with clear action items:

- Technical Q&A follow-up meeting

- Customer reference calls

- Partnership or POC discussion

- Strategic alignment conversation

Follow-Up (Within 24 Hours):

Send email with:

- Thank you and summary

- Key discussion points

- Materials promised (deck, architecture, case studies)

- Proposed next steps with specific dates

- Clear call to action

Explore Strategic Alignment Options

By this point, you should have a sense of whether there is real interest. If conversations are progressing positively, it is time to explore different types of strategic alignment.

Option 1: Partnership Agreement

This is often the “test drive” before acquisition. According to CB Insights 2024 data, 28% of SaaS acquisitions start with partnership agreements 6-18 months prior.

Types of partnerships:

- Technology integration (API partnership)

- Reseller agreement (they sell your product)

- OEM arrangement (white-label your product)

- Co-marketing partnership (joint go-to-market)

Benefits:

- Proves compatibility without commitment

- Generates revenue while building relationship

- De-risks integration for both parties

- Creates switching costs (makes acquisition more natural)

Option 2: Strategic Investment

If they have a corporate venture arm, this can be an excellent path. Data from Carta’s 2024 Corporate VC report shows:

Average terms for strategic investments:

- Investment size: $2-5M (seed stage), $5-15M (Series A stage)

- Ownership taken: 5-15%

- Typical rights: Board observer, pro rata rights, first right of refusal

- Average time to acquisition: 18 months

- Acquisition premium over last round: 2.1x – 3.2x

Pros:

- Capital to extend runway

- Validation from strategic partner

- Inside track to acquisition

- Customer and partnership access

Cons:

- May signal you are “for sale” to other acquirers

- Can complicate future acquisitions by others

- May come with restrictive terms

Option 3: Direct Acquisition Exploration

If the relationship is strong, timing is right, and strategic fit is clear, you can raise acquisition directly.

How to broach the topic:

Script for transition: “We have really enjoyed learning about your strategy and exploring how our products complement each other. We are at an interesting inflection point with [Company].

We are evaluating our path forward—continuing to build independently with additional funding, pursuing strategic partnerships, or exploring a strategic combination with the right partner.

Based on our conversations, it seems like there could be strong strategic rationale for a closer alignment. Would an acquisition conversation be of interest to explore?”

Alternative approach (more casual): “You know, as we have been talking about partnership, I keep thinking that there might be an even stronger strategic rationale for bringing our teams together. Have you all considered acquisition in this space?”

Gauging Interest:

Positive signals:

- They ask about your growth trajectory and plans

- They want to meet your team

- They ask about your cap table and investor expectations

- They inquire about exclusivity or timing

- They mention their M&A process or recent acquisitions

Neutral signals:

- They suggest continuing partnership discussions

- They want to see more traction or metrics

- They mention budget or timing constraints

Negative signals:

- They go silent after the topic is raised

- They pivot to only wanting partnership

- They mention building internally

- They raise significant concerns about fit

Manage the M&A Process

If acquisition conversations begin, you are entering a complex process that typically takes 90-180 days from LOI to close.

Phase 1: Initial Proposal (Weeks 1-4)

The acquirer will present initial terms verbally or via term sheet. This is not an LOI yet, just exploring parameters.

Key terms to discuss:

- Purchase price and structure (cash vs stock vs earnout)

- Employee retention requirements

- Founder employment terms and duration

- Earnout conditions (if any)

- Exclusivity period

- Timeline to close

Red flags at this stage:

- Extremely long earnouts (>24 months)

- Unrealistic performance earnouts

- Very low cash component

- Onerous employment terms

- No discussion of your team

Phase 2: Letter of Intent – LOI (Weeks 4-6)

According to SRS Acquiom’s 2024 M&A report, LOI terms include:

Typical LOI components:

- Purchase price and structure

- Closing conditions

- Exclusivity period (30-60 days)

- Due diligence requirements

- Timeline and milestones

- Breakup fees (if any)

What is binding:

- Exclusivity

- Confidentiality

- Certain expense provisions

What is non-binding:

- Purchase price (can change after due diligence)

- Closing conditions

- Employment terms

Critical LOI Negotiation Points:

- Purchase Price: Understand how it was calculated

- Earnout Structure: Favor retention bonuses over performance earnouts (controllable vs uncontrollable)

- Exclusivity Period: Keep it short (30-45 days) with ability to extend, not automatic 90 days

- Due Diligence Scope: Define clearly what they can access when

- Expense Coverage: Who pays if deal breaks?

Phase 3: Due Diligence (Weeks 6-12)

This is where deals often crater. Be prepared with organized documentation.

Due diligence areas:

- Financial (revenue, expenses, contracts, forecasts)

- Legal (incorporation, IP, contracts, employment, litigation)

- Technical (architecture, security, scalability, tech debt)

- Commercial (customers, pipeline, pricing, competition)

- HR (team, compensation, contractors, key person dependencies)

Tools to organize:

- Virtual data room (Carta, Shareworks, Caplinked)

- Organized by category

- All documents PDF format

- Clear naming conventions

- Index document with descriptions

Average number of documents requested: 150-300 items

Phase 4: Definitive Agreement (Weeks 12-14)

The legal team will draft the purchase agreement. Key terms:

Critical sections to review carefully:

- Purchase price calculation and escrow

- Representations and warranties

- Indemnification provisions

- Employment and retention terms

- Non-compete and non-solicit agreements

- Integration and transition requirements

Average legal fees: $75K-$250K depending on deal size

Phase 5: Closing (Weeks 14-18)

Final steps before money wires:

- Final due diligence sign-offs

- Board and shareholder approvals

- Regulatory clearances (if any)

- Third-party consents (landlord, major customers)

- Employment agreements signed

- Transition plans finalized

Managing Multiple Potential Acquirers:

If you have interest from multiple parties (ideal scenario):

Do not run a formal “auction process” at early stage. Instead:

- Maintain conversations with multiple parties at different stages

- Be transparent that you are having strategic conversations (do not lie about exclusivity)

- Use competitive tension subtly (never explicitly threaten)

- Move fastest with the party showing strongest interest

- Keep others warm in case lead deal falls through

According to Morrison Foerster’s 2024 data, having 2-3 active conversations increases valuation by average of 23% vs single bidder.

Continue Building During Negotiations

Here is the paradox: the best way to get acquired is to not need to get acquired. Throughout this entire process, keep:

1. Hitting Your Growth Metrics

Track and report weekly:

- New customer additions

- Revenue growth

- Product engagement metrics

- Pipeline development

Companies want to acquire winners, not strugglers. According to Bain’s research, every 10% decline in growth metrics during acquisition discussions reduces valuation by 5-8%.

2. Shipping Product Improvements

Maintain product velocity:

- Continue regular release cycle

- Ship features in your roadmap

- Address customer feedback

- Maintain quality and uptime

Slowing product development signals distraction and weakens your position.

3. Maintaining Team Morale

Your team will sense something is happening. Depending on stage:

Before LOI signed:

- Keep it confidential (tell only 1-2 trusted advisors)

- Maintain normal operations

- Do not hint at possible acquisition

After LOI signed:

- Tell key leadership (CTO, VP Eng, VP Sales)

- Emphasize nothing is certain until close

- Continue operating normally

After definitive agreement:

- Tell full team with clear communication

- Explain timeline and what happens next

- Address compensation and retention honestly

- Maintain focus through close

4. Building Leverage

Your best negotiating position is when you have alternatives:

Maintain optionality by:

- Keeping other strategic conversations active (without exclusivity)

- Having a credible “continue building” path ready

- Showing continued growth and momentum

- Having investors ready to support another funding round if needed

The best acquisition terms come when you do not desperately need to sell.

Free Tools for Acquisition Research

Here are the specific free tools mentioned throughout this guide:

Company and Deal Research:

- Crunchbase (free tier): Basic acquisition data, funding history

- CB Insights (newsletter): M&A trends and analysis

- Yahoo Finance: Public company financial data

- SEC EDGAR Database: Public company filings (search acquisitions in 10-K)

- LinkedIn: Track people, connections, company updates

Competitive Intelligence:

- G2.com: Product comparisons, reviews, feature analysis

- BuiltWith: Technology stack analysis, platform identification

- SimilarTech: Competitor technology tracking

- AlternativeTo: Product alternatives and comparisons

- Product Hunt: New product launches and features

Market Research:

- Google Trends: Search volume trends

- Gartner Peer Insights (free tier): Buyer preferences

- TrustRadius: Product reviews and comparisons

Financial Analysis:

- SaaS Capital Index: Valuation multiples and benchmarks

- Bessemer Cloud Index: Public SaaS company metrics

- Battery Ventures OpenCloud: SaaS benchmarks

Content and Writing Tools:

- Grammarly (free): Grammar and spelling checking

- Hemingway App (free): Readability scoring

- CoSchedule Headline Analyzer (free): Headline optimization

Connection Tools:

- LinkedIn Sales Navigator (trial): Advanced search and connection mapping

- Hunter.io (free tier): Email finding

- Calendly (free): Meeting scheduling

Organization:

- Google Sheets: Track acquisition targets and research

- Notion (free): Organize research and notes

- Airtable (free tier): Relationship and pipeline tracking

Summary: The Strategic Acquirer Playbook

Early-stage SaaS acquisition strategy has changed dramatically. According to Carta’s 2024 M&A report, 68% of venture-backed exits under $50M are now strategic acquisitions rather than IPOs or additional funding rounds.

This guide has covered the complete process:

Step 1: Determine Your Acquisition Thesis

- Identify your 2-3 strategic value propositions (technology, market access, team, product gap, competitive defense, revenue)

- Quantify your value with data-backed calculations

- Define your ideal acquirer profile using size, stage, market position, and cultural fit criteria

Step 2: Profile Potential Acquirers

- Identify 5-10 strategic acquirer candidates across platforms, horizontal SaaS, vertical consolidators, and enterprise modernization plays

- Analyze 5-10 past acquisitions per target to identify patterns in revenue thresholds, valuation multiples, integration success, and founder retention

- Determine their acquisition thesis by studying earnings calls, investor presentations, and competitive gaps

- Profile M&A team members using LinkedIn research and warm connection mapping

- Design a 6-12 month engagement strategy with 12 strategic touchpoints

Step 3: Execute Your Initial Engagement Strategy

- Secure warm introductions through investors, advisors, customers, or conference connections (52x more effective than cold outreach)

- Conduct initial strategic conversations focused 70% on listening, 30% on sharing

- Demonstrate value through customer introductions, market intelligence, content collaboration, or technical pilots

- Execute customized product deep dives focused on their specific gaps and integration approach

- Explore strategic alignment through partnerships, strategic investment, or direct acquisition conversations

- Manage the 90-180 day M&A process from verbal proposal through LOI, due diligence, definitive agreement, and closing

- Continue building momentum throughout negotiations to maintain leverage

Key Success Factors:

According to the research cited throughout this guide:

- Start relationship building 6-18 months before you want to sell

- Maintain conversations with 3-5 potential acquirers simultaneously

- Companies who invest 40+ hours in acquirer research achieve 30% higher valuations

- Having 2-3 active conversations increases valuation by 23% vs single bidder

- Warm introductions are 52x more effective than cold outreach

- Aligning to acquirer’s stated thesis increases deal probability by 3.4x

When This Strategy Makes Sense:

Strategic acquisition over additional funding is optimal when:

- You have reached product-market fit but need significant resources to scale ($2M-$10M ARR)

- Your product is more valuable as part of a larger platform than standalone

- You are in a rapidly consolidating market

- You compete against much larger, well-funded players

- You have strategic technology or market position that fills a specific gap for larger players

- You want liquidity sooner (3-5 years) rather than later (8-10+ years)

- You are comfortable with potentially less control post-acquisition

The choice between raising another round and pursuing acquisition is not binary. Many successful founders run both paths in parallel, maintaining funding conversations while developing strategic relationships. The key is being intentional about both paths rather than passive about either.

Your company represents years of your life and enormous value creation. You owe it to yourself, your team, and your investors to understand all your options—including the strategic acquisition path that many founders never seriously consider.

Start with your acquisition thesis today. Identify the right potential acquirers. Begin building relationships. The exit you engineer yourself is often far better than the one that happens to you.

Frequently Asked Questions

1. Why should early-stage SaaS CEOs consider an acquisition instead of more VC funding?

By 2025, data from Carta and PitchBook shows that strategic acquisitions deliver faster liquidity and less dilution than additional VC rounds. Founders who exit via acquisition retain 2–3x more ownership and achieve liquidity 3–4 years sooner than those pursuing Series A or B funding. For many, it’s the smarter, less risky path to value realization.

2. How can SaaS founders determine their acquisition thesis?

An acquisition thesis defines why a strategic buyer should acquire your company. Founders should identify 2–3 core value drivers—technology, market access, or team expertise—and back them with quantifiable data. For example, showing that your technology would take an acquirer 18 months and $4.5M to replicate creates clear, measurable strategic value.

3. What types of companies are most likely to acquire early-stage SaaS startups?

Ideal acquirers include public software companies seeking vertical expansion, late-stage SaaS platforms like Shopify or Atlassian filling product gaps, and private equity roll-up firms such as Vista Equity Partners and Thoma Bravo pursuing vertical SaaS consolidation. The key is targeting firms 5–10x your size that have recently completed similar M&A deals.

4. How should SaaS founders start building relationships with potential acquirers?

Begin 6–18 months before you want to sell. Use warm introductions via investors, advisors, or shared customers. Attend conferences like SaaStr or Web Summit where Corp Dev teams scout. Add value first—share market insights, offer pilot integrations, or co-author thought leadership. “Give first” relationship-building can increase deal likelihood 3–5x.

5. How long does a typical SaaS acquisition process take from first contact to close?

Strategic M&A typically spans 9–18 months. The first 6–12 months focus on relationship building and strategic alignment, followed by 90–180 days for due diligence and legal close. Companies with well-prepared documentation, clear product integration plans, and responsive teams close 30–40% faster than unprepared sellers.

6. What materials should founders prepare before starting acquisition conversations?

Prepare a one-page company overview, demo video, 3–5 customer case studies, an integration thesis, financial overview, and market analysis. According to Woodside Capital Partners’ 2024 M&A study, founders who present a complete six-piece “M&A Ready” data room increase valuation outcomes by an average of 40%.

7. How can I estimate my SaaS company’s valuation for a strategic acquisition?

Valuation depends on growth rate, ARR, retention, and strategic value. In 2025, early-stage SaaS acquisitions typically trade between 6–8x ARR for strategic deals and 3–5x ARR for financial buyers. Use benchmarks from the Bessemer Cloud Index and SaaS Capital Index to estimate your range, then justify a premium with proven IP, customer traction, or market access.

8. What earnout terms should SaaS founders expect in 2025 acquisitions?

Earnouts remain common in 2025 but are trending shorter and simpler. According to SRS Acquiom’s M&A data, 60% of SaaS deals include a 12- to 18-month earnout tied to revenue or retention milestones. Top-tier acquirers often prefer retention bonuses over performance-based earnouts to ensure alignment without penalizing founders for integration delays beyond their control.

9. How can founders increase valuation multiples before starting M&A discussions?

Focus on metrics that acquirers value most: strong Net Revenue Retention (NRR > 120%), efficient CAC payback (< 12 months), low churn (< 5%), and growing ARR per customer. Demonstrate repeatability with case studies and integrations. Companies showing double-digit monthly growth and a scalable go-to-market motion can add 25–40% to acquisition valuation multiples.