Product Managers: How to Survive an Acquisition

The pace of mergers and acquisitions in the tech market is on track to set new records this year. The Software Equity Group reported that there were 3,052 software M&A transactions in 2020. In the first half of 2021, there were 769 deals. They estimate that 2021 will set a new record. Acquisitions are challenging times for product managers. On the one hand, they can provide an opportunity for career growth. They can also result in the elimination of a product manager’s job. Product managers should learn how to survive an acquisition.

Backstory

I have been in the enterprise technology market for over 30 years. I have has led six global product management organizations for three public companies and three private equity-backed firms. I have led five acquisitions for a total consideration of over $175 million. I have led eight divestitures for a total consideration of $24.5 million in cash. I have held executive positions in product management, marketing, sales, development, customer service, and corporate development. I have first-hand experience in what it takes for product managers to survive an acquisition.

Product Managers Should Understand the Acquisition Process

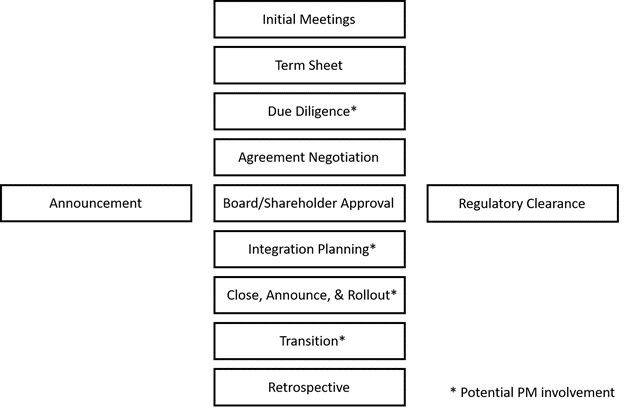

Most M&A projects follow a similar process. There are some variations depending on whether one or both of the companies is public and whether the deal requires regulatory approval. Unless they are actively involved in the deal team product managers are usually only involved in a couple of the processes at most. Product managers should understand the overall process so they can properly prepare themselves and set the appropriate expectations with their team, peers, partners, customers, and prospects. The overall process looks like this:

Depending on the type of deal, not all steps are required. Here is a brief overview of each step in the process.

Initial Meetings

Most acquiring organizations have a standard process of developing their acquisition strategy, identifying potential acquisition candidates, and monitoring market conditions. The first step in the overall process is for the acquirer to approach a potential acquisition candidate and conduct initial high-level meetings. Usually, a few senior executives and their advisors are involved in these meetings. The purpose of these meetings is to explore whether there is an interest and fit between two companies..

If one or more of the companies involved in the deal is public, then the chronology of these early meetings is usually disclosed in proxy statement filings with the SEC. For example, check out page 95 of Sendgrid’s proxy statement that was filed in conjunction with its acquisition by Twilio in 2018.

Term Sheet

If the initial meetings are positive, the next step is for the acquirer to submit an initial offer that is often known as a term sheet. The term sheet is usually a non-binding offer that describes the consideration (cash/stock) that is offered to acquire the company, along with the significant terms and conditions that would govern the deal. Most potential acquires require some type of formal offer before they will commit to entering into formal acquisition activities. They want to be able to judge the suitability of a potential deal as well as the likelihood that the acquirer can actually execute and close the deal.

Due Diligence

Once the basic terms of a transaction have been agreed to, the next step is for the acquirer to conduct legal, financial, and operational due diligence. Due diligence investigations help the acquirer understand the details of a target’s business, as well as risks and opportunities. This information helps the acquirer to assess whether their initial offer is fair and that they can obtain the anticipated benefits of the acquisition.

Legal due diligence looks at matters like corporate organization, stockholders, contracts, litigation, and regulatory matters to name a few. Financial diligence focuses on the quality and accuracy of the target’s financial statements, financial systems, cash flow, debt agreements, etc. Operational due diligence focuses on a detailed understanding of a company’s operations – marketing, product management, development, operations, customer service, sales, professional services, human resources, and finance/administration. Product Managers are often involved in operational due diligence activities due to their intimate knowledge of markets, customers, roadmaps, competitors, etc.

Agreement Negotiation

Upon completion of due diligence, the next step is to draft and negotiate the formal definitive agreements to effectuate the acquisition. These can include stock purchase agreements or asset purchase agreements. Often the drafting of these agreements occurs in parallel with due diligence. These are very detailed documents that cover every aspect and contingency of the deal. For example, you can check out the definitive agreement for SendGrid to be acquired by Twilio here starting on page 68.

Board/Shareholder Approval

Once the definitive agreements have been negotiated, the next step is for the board of directors and in many cases shareholders to approve the deal. If both companies are privately owned usually board approval is the only thing required. Sometimes lenders/debt holders also have to approve the deal. If one or both of the parties is public, then a shareholder vote is required in addition to the board approval. Usually, a special meeting is called and a formal proxy statement is filed with the SEC and sent to all shareholders of record. Depending on corporate by-laws, specific notice (often 30 days) is required before the shareholder vote can be held. If the deal requires regulatory approval, that approval must be obtained prior to holding the shareholder vote.

Regulatory Clearance

Many acquisitions, even between two privately held companies, must obtain regulatory approval before they can be completed. In the USA, the Hart-Scott-Rodino act governs mergers. If one of the parties to the merger has more than $50 million in annual revenue HSR approval is required. Companies file a notification with the Federal Trade Commission that reviews it for antitrust concerns. Usually, most requests are approved within 30 days. In rare cases, the FTC makes a ‘second request’ for additional information before approving the deal. In rare cases, the FTC will sue the companies in federal court in an effort to block the deal. Some deals involving foreign companies must also obtain national security clearance from the Committee on Foreign Investment in the United States (CFIUS). Deals involving UK operations or businesses require approval from the UK Competition and Markets Authority. Deals involving EU participants may require approval from the European Commission.

One regulatory matter product managers should be aware of is the Worker Adjustment and Retraining Notification Act (WARN Act). The WARN Act requires that employers provide workers with a 60-day notice of plans to terminate 50 or more employees from a location that employs at least 100 workers. California and 12 other states have their own version of the WARN Act that imposes additional employer obligations. Some aggressive acquirers will issue WARN notices prior to the closing of a deal.

Integration Planning

This is the process the acquirer uses to plan how to merge the two companies. Product managers, because of their deep insight into products and markets are often involved in integration planning activities. The integration process will depend a lot on how the acquirer plans to blend the two companies together. The basic options are discussed in the next section. Most integration planning activities consist of:

- Organization Chart & Roster Development

- Business Plan Development

- Transition Plan Development

- Separation Planning

- Announcement

- Transition Plan Management

For more details about integration planning check out M&A Basics for Product Managers. Part III: M&A Process.

Close, Announce & Rollout

Closing is the formal legal process of completing the acquisition. Depending on the situation this can include the execution of definitive agreements, conducting a shareholder meeting and proxy vote, notification of appropriate governmental agencies/stock exchanges, and the disbursement of funds. This step is generally not held in public.

Concurrent with the closing the acquisition is rolled out to employees, shareholders, customers, partners, industry analysts, and the press. Generally, all-hands employee meetings are held after notifications to terminated employees are conducted. Individual organization and team meetings are often held after the general all-hands meeting. Press releases are issued and industry analysts are briefed. Sometimes analysts are briefed before the rollout on an embargoed basis – they agree not to publish anything until the public rollout date.

Transition

Transition is the process of executing the changes required by the integration. This includes mundane things like updating company signage and websites, transitioning employees to new benefit plans, updating security badges, etc. Sometimes the activities are more significant like closing office locations, divesting non-core businesses, etc. Some employees might not have been selected to continue employment with the new company, but are retained for a period of time to transition their responsibilities to other employees.

Retrospective

60 to 90 days after the completion of the acquisition a post rollout assessment or retrospective is often held. The goal of this assessment is to identify what worked, what did not work, and how the process can be improved for the next acquisition. There is an old saying that “No battle plan survives the first contact with the enemy”. The same is true for acquisitions. Detailed planning and experience can help, but there are so many moving parts in an acquisition that there are always opportunities to improve.

Product Manages Should Understand Acquisition Integration Scenarios

Once you understand the overall M&A process, the next step is to assess what is the most likely scenario about how your company will be integrated into the acquiring company. The integration scenario will drive what happens in terms of headcount changes and investment levels. There are three common scenarios: strategic business unit, hybrid strategic business unit, and full business integration.

Strategic Business Unit

In this scenario, the acquired company continues to operate as a standalone entity. By definition, the acquired company’s stockholders are retired through some type of payout (cash/stock). The board of directors is also retired, although in some deals one or more members of the board may join the board of directors for the acquiring company. The CEO, executive team, and employees are largely left intact. Some positions may be eliminated at the closing of the deal for housekeeping purposes – these employees would have been terminated anyway – the acquisition just provided an opportunity to do it now instead of later.

In some cases, the CEO and one or more members of the executive team may decide to leave at the closing of the acquisition and be replaced by individuals from the acquiring company. This is done sometimes to ensure that there is “an adult in the room” for the new business unit. Depending on the structure of their employment agreements executives of the acquired firm may have to commit to staying with the new business unit for a specific period of time to maximize their compensation from the transaction.

Hybrid Strategic Business Unit

In this scenario portions of the acquired company are consolidated into the acquiring company, while the remaining parts continue on as a business unit. Typically, overhead functions such as accounting, legal, tax, human resources, IT, and data center operations are consolidated into their equivalents in the acquiring organization. Core functions like sales, marketing, product management, development, customer service, and professional services stay in the business unit. The primary driver of this strategy is to maximize efficiency and productivity while preserving the unique aspects of the acquired company’s talent, capabilities, and culture.

There are a couple of challenges with this scenario. First, for the functions that are consolidated into the acquiring organization, there are often headcount reductions. Product Managers are usually not impacted by these changes. Second, the acquiring company often introduces some of their standard infrastructure software into the business unit like salesforce automation, marketing automation, customer service, call center management, etc. This can impact the employees who maintain, administer, and operate the displaced systems. Third, the employees of the new business unit often experience what is known as “little fish / big pond” syndrome. Prior to the acquisition, the employees may have been “big fish” in what was admittedly their “little pond”. In the new scenario, they are “little fish” in a much bigger pond. This can take some getting used to and some employees never fully get comfortable with the new situation. They decide to move on to another opportunity. Conversely, some employees take advantage of the new situation to move into different or promotional opportunities in the acquired company.

Full Business Integration

This is the most common scenario. In this case, the operations of the acquired company are fully incorporated into the operations of the acquired company. For example, product managers report to the Director/VP of product management or the Chief Product Officer. Product Marketers join the acquiring company’s Product Marketing Team, salespeople join the sales team, etc. Middle and upper management positions are often eliminated. Depending on the potential the acquiring company sees, investment in development and customer support can be reduced, sometimes significantly.

Cost reduction/profit improvement is usually the primary driver of these changes. This is the area of most risk for product managers. Once an acquisition is announced, product managers should do some quick basic research to determine the potential scale of headcount reductions the deal might drive.

If the acquiring company is publicly traded you can access their complete financials via filings with the SEC. If you are unfamiliar with accessing reading and interpreting filings like 10-Ks, check out Why Product Managers Need to be Able to Read 10-K Reports. One important clue is when the deal is announced, does the acquirer state that “the acquisition will be immediately accretive to EPS”. This means that they expect that the acquired business, when integrated into the acquiring company, will generate profits at a level that is higher than the acquiring company currently generates.

An example of this is Broadcom’s recent acquisition of CA, Inc. CA (fka Computer Associates) has been a long-term acquirer of mature software businesses, although in recent years they have launched a number of initiatives to organically grow their business. Broadcom was a very profitable semiconductor software solutions. In 2018 they had a net income of $12.6 billion on revenues of $20.8 billion – a 61% net income margin. CA had net income of $486 million on revenues of $3.3 billion, or 11%. Broadcom stated in their announcement press release that the deal would be “immediately accretive to earnings per share”. To achieve that goal Broadcom would have to reduce CA’s operating expenses by over $2 billion. Significant headcount reductions are the only way that scale of cost reductions could be achieved.

When both the acquirer and acquired company are private you will need to do some more detective work. Look at past companies that the acquirer has bought. LinkedIn is the easiest source to use. Do a search for executives, using ‘past companies’ as one of the search filters. Try titles like the VP of Product Management, Director of Product Management, or Senior Product Manager. See when specific people left the acquired company – if it is close to the date that the acquisition closed there is a chance they were terminated as part of the deal. This is not a foolproof technique, people leave acquired companies for a lot of reasons but it can provide you with some valuable hints.

Product Managers Should Prepare for Acquisition Integration Planning

Product managers are generally not involved in the acquisition process, but sometimes they are invited to participate in the merger integration planning process. Product managers can be extremely valuable in integration planning because they are often experts in the market, product/market fit, current, and future roadmaps, customer relationships, industry analyst relationships, etc. You should assemble the standard product management artifacts like personas, customer buying journeys, value equations, positioning docs, sales battle cards, roadmaps, backlogs, go-to-market plans, etc. If you are lucky enough to be invited into the process there are some things you can do to maximize your success. T

Research the Acquirer

To start, you should do some basic research about the acquirer to understand their acquisition history and operating model. There are a number of free sources you can review.

Crunchbase. Crunchbase is an excellent free resource that provides a ton of information about both public and private companies. They provide a detailed profile that includes funding, investors, acquisitions, web stack technology, competitors, etc. For example, click here to see a list of the 236 acquisitions that Google has completed since its founding.

SEC Filings. For publicly traded companies regulatory filings like 10-K annual reports and 10-Q quarterly reports provide a lot of detailed information. To learn how to read and interpret these filings check out Why Product Managers Need to be Able to Read 10-K Filings

Other Open Source Sites. There are a number of other free resources like LinkedIn, D&B Hoovers, and user review sites like Capterra, Software Advice, and Gartner Insights. For more details check out Open Source Competitive Intelligence for Product Managers

Research Past Acquisitions

Most acquirers have a track record of past acquisitions. Understanding the types of acquisitions will help you understand the primary motivation behind your deal. You should identify and briefly investigate each acquisition they have completed. 10-K filings for publicly traded acquirers will detail all of their acquisitions. For privately held companies, search Google for Company Name + Acquisition or Company Name + Merger to get a list.

Generally, there are four common types of acquisitions:

Acceleration Deals. Acceleration acquisitions speed an acquirer’s entry into a market they want to participate in. Instead of building and launching a new product, the company acquires a player already in that market. An example of this was Ford Motor Company’s acquisition of Spin, the scooter startup.

Diversification Deals. Diversification deals enable the company to enter a market that is different than the core markets they currently target. A recent example of this was Twilio, a provider of enterprise messaging, integrated VoIP and communications SaaS, acquired SendGrid, a provider of web and mobile email marketing SaaS.

Consolidation Deals. In consolidation deals, an acquirer purchases a competitor that is in the same market they currently serve in to increase market share. Broadcom’s acquisition of CA is a classic example of a consolidation deal.

Financial Deals. In financial deals, the acquirer purchases a company because they believe that it is significantly undervalued and that through restructuring, financial engineering, and investment they can earn significant returns. Vista Equity Partners’ acquisition of Marketo and sale three years later to Adobe for a $2 billion gain is an example of this.

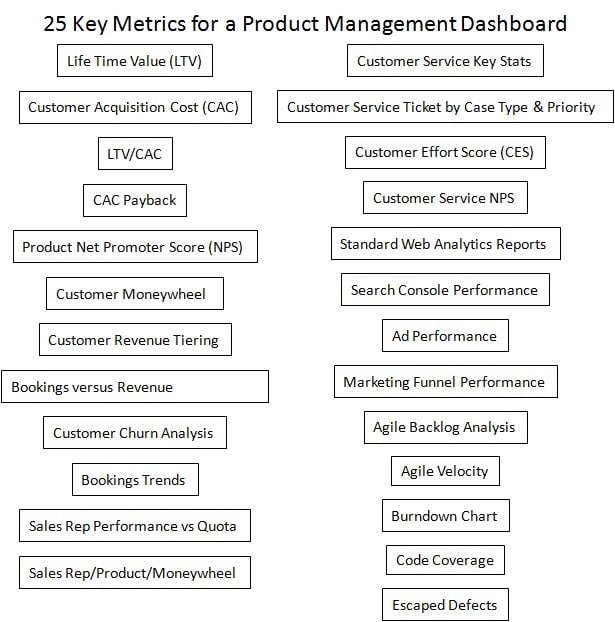

Know Your Numbers

Being able to crisply and clearly communicate your knowledge of your products and markets is critical during integration planning. Team members from the acquiring company may or may not be experts in your markets and technology. Numbers are the lingua franca of the merger integration process. They reduce complex topics down to simple facts that can be readily communicated you should brush up on the metrics and numbers associated with your products. Depending on how product management is structured at your company you should be familiar with some or all of the following metrics:

For more information about these types of metrics check out 25 Key Metrics for a Product Management Dashboard

In addition to knowing what your numbers are, you need to be able to explain how and why the numbers change over time. For example, why has onboarding cycle time decreased 18% in the past year? Why has the number of severity one defects increased after each of the past four Sprints? Why has the Life Time Value of enterprise customers decreased 9% over the past year? How has the release of a new version of your main competitor’s product impacted the win rate for net new enterprise customers? Being able to intelligently discuss matters like this with members of the integration team will enable them to more effectively plan and execute the integration.

Even if you are not invited to participate in the merger integration process you should brush up on your numbers and product management artifacts just in case questions arise during the process and somebody from the integration team raises a question. Your responses and evidence of preparation will be noted and remembered.

Product Manager Acquisition Do’s and Don’ts

Acquisitions represent significant change and that can be uncomfortable for a lot of people. Change management professionals call the time between when an acquisition is announced and it actually closes the ‘valley of death’. Based on experience there are some definite Do’s and Don’ts during this difficult time:

Do’s

- Accept that you are not in control. It is difficult, but as a product manager, you have little control over the acquisition process. You can just control how you choose to behave and react.

- Learn about the acquirer and its history. Spend some time doing basic research about the acquirer. You will find things you like and things you dislike. Most successful acquirers know that while they need to imbue their culture in the acquired company, they also must learn how to adopt the best of what the acquired company has into their company.

- Understand and support the process. Learn what you can about the planning and integration process. Provide whatever support is asked for in a timely and professional manner.

Don’ts

- Break confidentiality of the integration process. If you are fortunate to be invited into the integration planning process never, ever, break the confidentiality of those activities. While you may be tempted to tell your friends what you are learning about strategy changes or job cuts, don’t. More than one employee has been abruptly terminated as a result of breaking confidentiality.

- Speculate about job cuts. While it may be tempting, do not speculate about potential job cuts. Integration planning exercises are fluid processes and things can change up to the last minute.

- Feed/spread rumors. Rumor mongering between the time an acquisition is announced and it actually closes is almost a national sport. Spreading rumors will just serve to upset people. When you are not in control of a process it is natural to be frustrated by lack of information.

- Post negative items on social media. Venting on social media is a common thing, but doing it during an acquisition is almost a sure-fire ticket to get put on the “Cut” versus “Keep” list. A classic example of this is the infamous Cisco Fatty story.

Summary

Acquisitions are challenging times for product managers. On the one hand, they can provide an opportunity for career growth. They can also result in the elimination of a product manager’s job.. Product managers are uniquely positioned to be very valuable during the M&A process. M&A projects can be stressful,. Product managers should learn how to survive an acquisition.