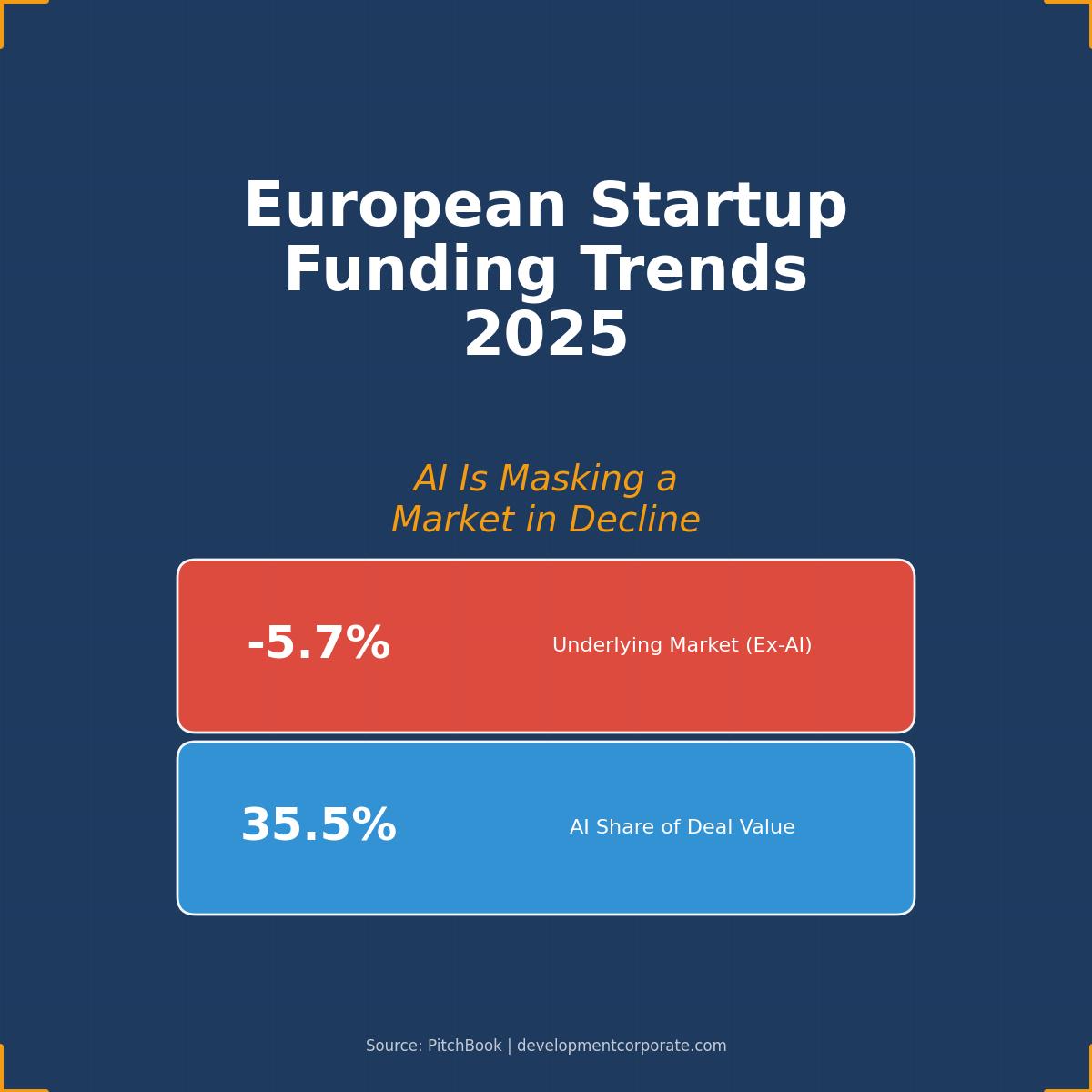

European Startup Funding Trends 2025: AI Is Masking a Market in Decline

European startup funding trends tell a story of two markets in 2025. On the surface, deal value climbed 5.1% to €66.2 billion, suggesting a recovering ecosystem. But strip away artificial intelligence investments, and a different picture emerges: underlying deal value contracted 5.7% year-over-year, falling to €42.7 billion. According to PitchBook’s 2025 Annual European Venture Report, the European venture capital market isn’t growing—it’s increasingly dependent on a single vertical that now accounts for more than a third of all investment activity.

For startup founders operating outside the AI gold rush, this bifurcation has immediate implications for fundraising strategy, competitive positioning, and exit planning. As we’ve analyzed in our European VC Valuations 2025 report, the data reveals an ecosystem where capital concentration creates both winners and losers—and where the fundamental question isn’t whether you’re building a great company, but whether you’re building in a sector that can still attract meaningful investment.

The Headline Numbers Are Misleading

PitchBook’s 2025 Annual European Venture Report delivered what appeared to be positive news: deal value increased to €66.2 billion, Q4 activity strengthened, and several marquee transactions demonstrated continued appetite for European technology companies. The largest included Revolut’s €2.6 billion round and Mistral AI’s €1.3 billion raise.

But the volume story tells a fundamentally different narrative. Deal counts declined 20.6% year-over-year, dropping to just 10,206 transactions—the lowest level since 2017. Fewer companies are raising money. The companies that do raise are raising larger rounds. And the sector driving those larger rounds is overwhelmingly artificial intelligence. This pattern mirrors what we documented in our analysis of the decline of exits and VC returns—a structural shift that continues to reshape capital allocation.

Figure 1: European VC deal value with and without AI investments (2019-2025). Source: PitchBook

The mathematics are straightforward: AI-related deals captured €23.5 billion of the €66.2 billion total, representing 35.5% of all European venture investment. This concentration has grown from 28.1% in 2024 and just 19.5% in 2020. Remove AI from the equation, and European venture deal value declined from €45.3 billion in 2024 to €42.7 billion in 2025—a contraction that headlines never captured.

The AI Concentration Problem: Europe’s Single-Vertical Dependency

AI’s dominance in European venture isn’t merely notable—it represents a structural shift in how capital flows through the ecosystem. In 2015, AI accounted for just 9.3% of European deal value. By 2021, during peak market exuberance, that figure reached 20.9%. Today, at 35.5%, AI commands more than double its pre-pandemic share. We’ve tracked this acceleration in our coverage of Europe’s AI SaaS startups.

Yet Europe’s AI concentration still lags significantly behind the United States, where AI now represents 65.4% of all venture deal value—nearly double Europe’s share. This gap raises two competing interpretations: either Europe has room to grow its AI investment substantially, or the US market serves as a cautionary tale of concentration risk taken to extremes.

Figure 2: AI share of total VC deal value, Europe vs. United States (2015-2025). Source: PitchBook

PitchBook’s analysts posed the question directly: “Is there an AI bubble? And if so, could we see it burst next year in 2026?” Their projection suggests that by end of 2026, AI will account for 50% of European deal value—a nearly 15-percentage-point increase from current levels. This forecast implies continued crowding out of non-AI sectors and deepening dependence on valuations that may not reflect underlying business fundamentals.

The report draws an important distinction between AI companies whose core intellectual property resides in AI technology versus companies employing AI as “functional add-ons in legacy software.” The former category commands premium valuations; the latter may face reckoning as the market matures. This distinction matters particularly for SaaS founders—as we’ve documented, even AI coding tools have failed to deliver promised productivity gains, slowing developers by 19% in controlled studies.

Non-AI Sectors: The Crowding Out Effect

Capital concentration in AI creates direct consequences for founders operating in other verticals. The sector ranking shifts from 2024 to 2025 reveal clear winners and losers in the competition for investor attention.

Figure 3: Sector ranking changes by deal value (2024 → 2025). Source: PitchBook

Climate tech experienced the steepest decline, falling from seventh to eleventh place in deal value rankings. This four-position drop represents a significant pullback in investor appetite for climate-focused companies, despite the long-term regulatory and market tailwinds that should theoretically support the sector. Clean tech similarly declined, dropping from fourth to sixth position.

Life sciences contracted 6.2% year-over-year, with €8.4 billion in investment—underperforming even the already-depressed underlying market. For biotech and pharma founders, this decline coincides with broader public market challenges for life sciences companies. Notable exceptions included Isomorphic Labs (€536 million) and Tubulis (€308 million), but both combined AI with traditional life sciences approaches.

Fintech stands as a notable exception to the non-AI decline, with investment reaching €13.4 billion—a 29.3% increase year-over-year. However, this growth was substantially driven by Revolut’s €2.6 billion round. Excluding Revolut, fintech investment still showed resilience, suggesting the sector benefits from AI tailwinds as financial services companies integrate machine learning into their core offerings. Other major fintech rounds included Binance’s €1.9 billion raise in Malta.

European VC Fundraising Hits Record Low

While deal activity tells a story of AI-driven resilience, the fundraising market reveals deeper structural stress. European VC funds raised just €12 billion across 148 vehicles in 2025—the lowest figures on record for both capital raised and fund count. This collapse has immediate implications for founders, as we’ve analyzed in our pre-seed funding landscape overview.

Figure 4: European VC fundraising activity (2015-2025). Source: PitchBook

The 49% year-over-year decline in capital raised represents more than cyclical adjustment. Consider the trajectory: in 2022, European VC funds raised €38.8 billion across 572 vehicles. Three years later, capital raised has contracted 69% while fund count collapsed 74%. The magnitude of decline suggests structural challenges beyond normal fundraising cycles.

Regional leadership also shifted meaningfully. For the first time on record, the UK and Ireland lost their top position in capital raised to the DACH region (Germany, Austria, Switzerland). UK share of capital raised fell to 22.5%—also a record low—while DACH captured 26.9%. The top fund closes included Sofinnova Capital (€650 million), Medicxi (€500 million), and Cherry Ventures (€500 million).

The LP distribution problem remains central to fundraising challenges. Limited partners cannot commit new capital to venture funds without receiving distributions from existing investments. With exit markets constrained—only 19 VC-backed IPOs occurred in Europe during 2025, a record low—the capital recycling mechanism that sustains venture fundraising has effectively stalled. This dynamic directly impacts founders’ access to capital, particularly at earlier stages where we’ve seen seed and early-stage European VC trends shift significantly.

Exit Markets: The Illusion of Recovery

Exit value reached €67.8 billion in 2025, appearing to match historical highs. But the concentration tells a different story: the Klarna IPO alone contributed €12.7 billion, while the eToro listing added another €3.5 billion. Together, the top ten transactions accounted for nearly 40% of all exit value. Remove Klarna, and the underlying exit market showed little growth from 2024.

The structural question for European venture centers on whether public listings remain a viable exit path. Despite favorable market conditions—valuations and volatility stayed within the “IPO window” throughout 2025—only 19 VC-backed companies went public. This represents a record low and suggests that for venture-backed companies, going public has become a less attractive option as companies choose to stay private longer. Our analysis of the SaaS exit crisis details why this matters for technology founders specifically.

The nature of successful IPOs has also shifted. Profitable companies now account for nearly 90% of listings, up from 66.4% in 2024. Public market investors have grown more selective, creating higher bars for companies considering IPO paths. M&A dominated exit activity, with notable transactions including Nexthink’s €2.6 billion buyout. As we’ve documented in our Q3 2025 Enterprise SaaS M&A analysis, PE-backed acquisitions continue to dominate the landscape.

Secondary markets are emerging as meaningful liquidity channels. PitchBook estimates the European direct secondaries market at $47.5 billion in their base case. As we’ve covered in our analysis of secondary markets as a strategic shift in seed-stage VC, this represents an increasingly important consideration for founders and early investors seeking liquidity in a constrained environment.

The Value-Volume Divergence: Fewer Deals, Bigger Checks

The 2025 European startup funding data reveals a persistent pattern: deal value increasing while deal count declines. This divergence carries significant implications for founders at different stages.

Figure 5: European VC deal value versus deal count divergence (2019-2025). Source: PitchBook

Late-stage deals drove the bifurcation. Series D and later rounds increased 45.2% year-over-year, while seed and Series C stages saw double-digit declines in value. Capital is flowing to fewer, larger companies—typically AI-related—while early-stage founders face a more competitive environment for smaller pools of available capital. For context on early-stage valuations, see our analysis of pre-seed and seed stage acquisition values.

The top deals of 2025 illustrate this concentration: Revolut (€2.6 billion), Binance (€1.9 billion), Mistral AI (€1.3 billion), and Nscale (€1.3 billion). Three of these four companies operate in AI or AI-adjacent verticals. Other notable rounds included Oura’s €775 million raise, Helsing’s €600 million defense AI round, and Brevo’s €500 million for AI-powered marketing technology.

Strategic Implications for Founders in 2026

The European startup funding trends documented in PitchBook’s report translate into concrete strategic considerations for founders planning 2026 fundraising or exit activities.

For AI founders: The window of elevated valuations may not persist indefinitely. PitchBook explicitly raises the bubble question, and the report notes that “any shift in sentiment towards AI valuations could reverberate across the broader venture landscape.” Companies like Black Forest Labs (€259 million) demonstrate continued appetite for foundational AI companies, but founders should consider whether current market conditions favor accelerated fundraising to lock in valuations.

For non-AI founders: Capital scarcity is real and likely to persist. The crowding-out effect means competing with AI companies for investor attention, not just dollars. Founders should expect longer fundraising timelines, greater emphasis on profitability metrics, and potentially smaller rounds than historical comparables would suggest. Our strategic acquisition exit guide for early-stage SaaS offers frameworks for founders considering alternative paths.

For founders considering exits: Public markets increasingly require profitability. The 90% profitable share of 2025 IPOs suggests that the traditional venture playbook—grow at all costs, figure out unit economics later—no longer translates to public market success. As we’ve detailed in our Plan B exit strategy analysis, building M&A optionality should be part of every founder’s strategic toolkit.

For all founders: The fundraising environment reflects structural constraints, not merely cyclical weakness. With LP distributions constrained and fund managers struggling to raise new vehicles, available capital for startups may remain limited even if macro conditions improve. The Software Equity Group’s 2024 SaaS M&A review provides additional context on how these dynamics affect valuation multiples.

The 2026 Outlook: Questions Without Easy Answers

European startup funding trends entering 2026 remain characterized by uncertainty. PitchBook’s analysts project continued AI dominance, potentially reaching 50% of deal value by year end. They expect IPO windows to remain open for profitable companies. They anticipate ongoing fundraising challenges until LP distributions improve.

The geopolitical and macroeconomic backdrop adds complexity. Potential rate hikes in Europe following 2025’s dovish stance, ongoing tariff discussions, and defense reshoring priorities create a mixed environment for technology investment. Venture debt, which held relatively resilient at €19.2 billion in deal value, may benefit from rate movements as companies seek alternative financing. Notable venture debt transactions included Flix’s €1.1 billion and FINN’s €1 billion raise.

But the fundamental question remains unanswered: how resilient is the European venture market without AI’s artificial support? If AI valuations correct—whether through bubble dynamics, regulatory intervention, or simply market rationalization—the underlying venture ecosystem has shown declining activity for multiple consecutive years. The recovery narrative depends heavily on a single vertical that may or may not justify current capital allocation levels.

The Bottom Line

European startup funding trends in 2025 tell two stories. The headline story is resilience—€66.2 billion in deal value, marquee transactions from companies like Revolut and Mistral AI, and growing AI investment. The underlying story is contraction—fewer deals, collapsing fundraising, constrained exits, and increasing dependence on a single vertical that may or may not represent sustainable value creation.

For founders and investors navigating this bifurcated landscape, the data suggests caution. The market rewards AI exposure but concentrates risk. The fundraising environment creates operational constraints regardless of company quality. The exit pathways demand metrics that many venture-backed companies cannot deliver.

Understanding these dynamics—rather than relying on headline numbers that obscure underlying trends—provides the foundation for strategic decision-making in an environment where the rules continue to shift.

Development Corporate advises enterprise SaaS companies on strategic M&A transactions. If you’re evaluating exit timing, market positioning, or strategic alternatives in the current environment, explore our strategic acquisition advisory services to discuss how these market dynamics affect your specific situation.