a16z: The SaaS Moat Scorecard

What a16z’s Seven Powers Framework Reveals About Software Valuations in 2026

SaaS M&A valuation frameworks are being rewritten — not by AI itself, but by the market’s panic about AI. Since January 2026, ETFs tracking public software companies have fallen roughly 30 percent, erasing every gain logged since ChatGPT’s launch. Salesforce, Adobe, Intuit, ServiceNow — bellwethers that compounded investor capital for a decade — are down 25 to 30 percent in weeks. The narrative has a name: the “SaaSpocalypse.”

The panic is real. The conclusion is wrong. And the gap between them is where M&A opportunity lives.

In a March 2026 analysis, a16z partners Alex Immerman and Santiago Rodriguez made the contrarian case: AI will not kill the software industry — it will split it. Companies with genuine moats will emerge stronger. Thin wrappers and archaic incumbents will face justified pressure. The market is currently pricing them all the same.

For M&A practitioners, that mispricing is an actionable signal. This article applies Hamilton Helmer’s Seven Powers framework — the analytical backbone of the a16z piece — to the 2026 SaaS acquisition market, with specific due diligence questions for each moat dimension.

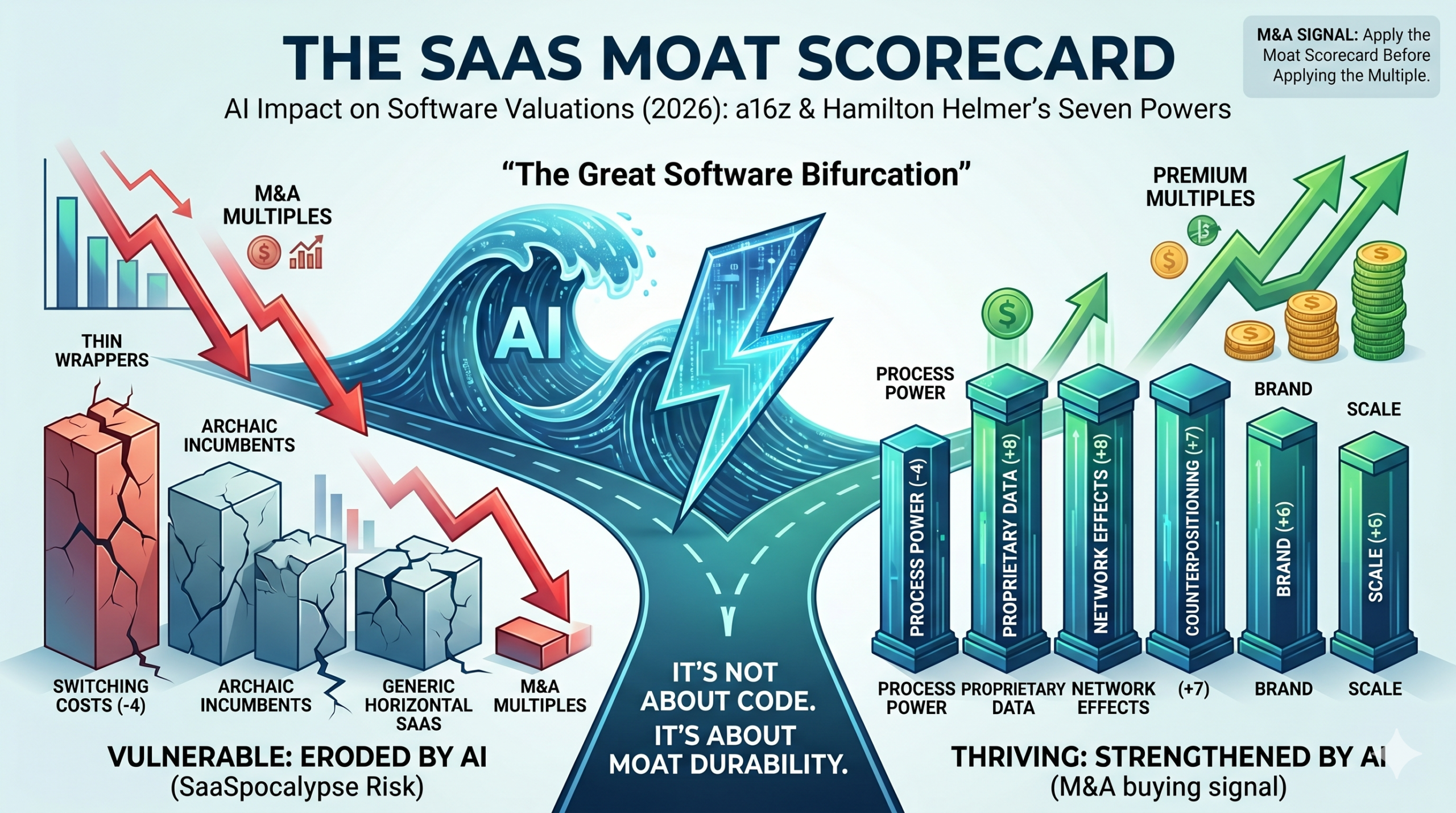

What a16z Actually Said — and What the Market Missed

The bearish case on software rests on a fundamental misunderstanding: the market is treating software companies as though their value lives in their code. It does not. Code was never the moat. If it were, these companies would have been killed by open-source software or offshore engineering years ago.

The a16z analysis identifies four specific bear arguments driving the SaaSpocalypse narrative: foundation model labs moving up the stack; enterprises “vibe-coding” internal replacements; incumbents expanding product breadth until they collide; and AI-native new entrants undercutting on price. Each argument is partially valid. None of them justifies the conclusion that software moats are gone.

DevelopmentCorporate has tracked this dynamic across the M&A market for months. As we documented in our analysis of VC rejection signals and SaaS M&A valuations, the companies being rejected or discounted are not “software companies” — they are companies that never had a durable competitive advantage to begin with. The AI era is making that previously obscured distinction visible.

| “AI isn’t going to destroy the software industry; it’s going to split it into two parts.” — a16z, March 2026 |

The Seven Powers Moat Framework: An M&A Due Diligence Lens

Helmer’s framework identifies seven distinct sources of durable competitive advantage. The a16z analysis evaluates each one against the AI disruption thesis. We translate each into a specific M&A diligence question for acquirers evaluating SaaS targets in 2026.

Figure 1: Hamilton Helmer’s Seven Powers — AI impact score per moat dimension. Positive scores indicate AI strengthens the moat; negative scores indicate erosion. Source: DevelopmentCorporate / a16z, 2026.

1. Process Power: The Highest-Value Moat in the AI Era

Application software is, at its core, a stored process — it encodes opinions about how an organization’s functions should operate, and those opinions calcify over years of use into something inseparable from the organization itself. The a16z analysis calls this “process engineering,” and argues it becomes more valuable as AI improves, not less.

Better foundation models do not make the application layer thinner. They make it more capable, because the hard part was never raw intelligence — it was knowing what to do with it. A Harvey AI that deeply understands how a specific law firm structures its work cannot be replicated overnight by a new entrant, even at zero marginal code cost.

M&A Due Diligence Question: Does the target’s software encode institutional workflow knowledge that would take a competitor 12–18+ months to replicate? If yes, this moat is durable — and likely underpriced in the current panic.

2. Network Effects: Getting Stronger, Not Weaker

Network effects in enterprise software are subtler than in consumer platforms, but no less real. Salesforce is not just a CRM database — it is an ecosystem. When every enterprise uses one platform, the network becomes self-reinforcing through third-party integrations and certified administrators. AI amplifies this effect: as the network grows more capable, each node adds more value.

AI-native companies are already building these network effects into their architecture. Harvey and Hebbia are creating finance and legal collaboration spaces where more users and more agents on the same platform make the platform more valuable. EliseAI’s maintenance product becomes more valuable with every unit and vendor added.

M&A Due Diligence Question: Does the target’s value proposition strengthen as more customers, users, or agents join the platform? If migration gets easier, aggregation gets easier — but network effects do not disappear.

3. Cornered Resources: Proprietary Data Is the New Infrastructure

As foundation model capabilities commoditize, the scarcity shifts from the model to the data. Bloomberg’s live market data, Abridge’s clinical conversations, OpenEvidence’s medical library, and VLex’s legal database are not easily replicable — and AI makes these resources dramatically more valuable than they were when models were weaker.

DevelopmentCorporate has tracked this dynamic directly in the credit markets. Our analysis of private SaaS lenders’ evolving criteria found that lenders and acquirers alike now make a single critical distinction: software companies with proprietary data moats and embedded workflows remain financeable. Companies with generic functionality that AI can replicate cheaply do not.

M&A Due Diligence Question: Does the target’s core product generate or rely on proprietary data that general-purpose AI models cannot access or replicate? If the data is publicly scrapeable, it is not a moat.

4. Brand: “No One Got Fired for Buying IBM” Endures

Brand power is often dismissed as soft. In enterprise software, it is structural. As AI lowers barriers to entry and floods the market with new entrants, the signal value of a trusted brand increases. The closer a product sits to business-critical functions — payment processing, compliance, core ERP — the more powerful brand effects remain.

The a16z analysis notes one nuance: as more decisions get delegated to AI agents optimizing for price, brand power may evolve. But as long as agents report to humans who worry about getting fired, the principle holds.

M&A Due Diligence Question: Does the target own recognized authority in a category where buyers self-identify as having low risk tolerance? Stripe’s default status in payment processing is a reference point.

5. Switching Costs: Eroding — But That’s the Point

This is the one moat that AI genuinely erodes. Agents can assist with migration work that previously took months. The a16z analysis is candid: legacy companies with “hostages, not customers” — to borrow a phrase from Alex Rampell — will face more pressure than they are accustomed to.

But the a16z authors frame this as a feature, not a bug. When companies must earn loyalty rather than rely on lock-in, the result is better products, faster innovation, and a healthier competitive ecosystem. For M&A buyers, declining switching costs are not a disaster — they are an unlock for acquirers who can offer a genuinely superior platform to newly liberated customers.

M&A Due Diligence Question: Is the target’s retention driven by genuine product value or by migration friction? If the answer is friction alone, re-model churn assumptions upward as AI-assisted migration matures.

6. Counterpositioning: The AI-Native New Entrant Advantage

Counterpositioning occurs when a new entrant’s business model is unattractive for the incumbent to copy without destroying its existing economics. The classic SaaS disruption case today: outcome-based pricing versus per-seat pricing.

Decagon prices its customer support product per conversation handled — not per agent seat — and will eventually price per resolution achieved. Zendesk cannot easily make that same move without cannibalizing its seat-based revenue. As we documented in our analysis of the Agentforce pricing transition, even Salesforce’s move toward consumption-based pricing represents a structural valuation signal — one that mid-market SaaS sellers need to price into their exit models today.

M&A Due Diligence Question: Does the target’s pricing model align incentives with customer outcomes? Is the incumbent’s pricing model structurally indefensible against an outcome-based competitor? Both conditions create transaction opportunity.

. Companies with moat scores above 6 command nonlinear acquisition premiums. Source: DevelopmentCorporate / PitchBook, 2026.")

Figure 2: Composite moat score vs. EV/Revenue multiple across closed SaaS M&A transactions (2025–Q1 2026). Companies with moat scores above 6 command nonlinear acquisition premiums. Source: DevelopmentCorporate / PitchBook, 2026.

The Great Software Bifurcation: Who Wins and Who Loses in M&A

The a16z analysis is explicit about the bifurcation outcome. Vulnerable categories include: frontend tools that are thin wrappers around commodity functionality, incumbent systems of record that raise prices annually while running on archaic interfaces, and companies with pricing models structurally inferior to what AI-native competitors offer.

Companies that will thrive: those delivering genuine value, co-evolving with customers around deep workflows, and building platforms where AI makes the network more capable, not more commoditized.

. Categories above the 70% premium threshold command durable acquisition multiples; those below face compressing valuations. Source: DevelopmentCorporate analysis, 2026.")

Figure 3: M&A multiple durability by software category (2026). Categories above the 70% premium threshold command durable acquisition multiples; those below face compressing valuations. Source: DevelopmentCorporate analysis, 2026.

This maps directly to what we have observed in the 2026 SaaS M&A valuation gap: 86% of buyers expect AI valuation premiums to continue, but only 63% of 2025 targets had more than limited AI use. The mismatch between expectation and evidence is compressing multiples for the wrong companies — and creating mispriced opportunities for acquirers who can distinguish process power from PowerPoint AI roadmaps.

The same bifurcation logic applies to the recently documented “SaaSpocalypse is a buying signal” thesis: sponsors with PE-backed software companies facing loan covenant pressure may be forced to transact at valuations that do not reflect their actual moat durability. For strategics and patient acquirers, that pressure is an entry point.

| “The companies that win will be the ones delivering genuine value, not the ones that built the highest walls around their customer base.” — a16z, March 2026 |

M&A Strategy Implications: Sellers and Buyers in a Bifurcated Market

The a16z framework arrives at the same conclusion that DevelopmentCorporate has embedded in our advisory practice: the unit of M&A analysis is no longer ARR or NRR in isolation. It is moat quality. ARR is a trailing metric. Moat durability is a forward-looking one — and in a period of market dislocation, it is the variable that separates premium exits from distressed ones.

For sellers: the 30% ETF decline is not uniform. Moat-durable companies are being incorrectly marked down alongside thin-wrapper competitors. The advisory challenge is demonstrating moat depth before a transaction process begins — through AI search visibility, workflow ownership documentation, and NRR evidence that reflects genuine product stickiness rather than lock-in friction.

For buyers: the companies facing pressure in the current market are not all the same. Applying uniform multiple compression to every software asset is the analytical error that creates acquisition opportunity. The Seven Powers scorecard — applied systematically in due diligence — identifies which companies deserve the discount and which have been caught in indiscriminate selling.

| For PE/VC InvestorsApply the Seven Powers moat scorecard before adjusting valuation assumptions based on AI disruption narratives.Portfolio companies with documented process power and proprietary data moats are being incorrectly marked down alongside structurally weaker assets.Sponsors with covenant-pressured SaaS assets should model churn scenarios based on switching-cost erosion, not just on revenue trend.The SaaSpocalypse is a sorting mechanism. M&A teams with a rigorous moat framework will find mispriced assets in the current dislocation.Counterpositioning risk is real for legacy per-seat pricing models. Portfolio companies should accelerate transition to outcome-based pricing before a process begins. |

| For SaaS Founders Approaching ExitYour exit valuation is a function of your moat score, not just your ARR multiple. Document process power explicitly before a process.Network effects, proprietary data, and workflow depth — not AI feature bullets — are what sophisticated buyers will underwrite at premium multiples.If your retention is driven by migration friction rather than product value, re-engage your customer success motion before a transaction. Buyers will find the difference in due diligence.Outcome-based pricing signals a stronger moat than per-seat pricing in 2026. Consider whether your pricing model reflects your actual value delivery.Your LLM citation footprint is now a brand equity variable. Companies invisible to major AI models have an unpriced acquisition risk that is widening daily. |

| For Enterprise CTOs and CPOsThe a16z process power thesis is a product roadmap signal: embed your software deeper into your customers’ institutional workflows, not just their interfaces.Proprietary data generated by your product is your most defensible moat. Build capture and governance architecture before competitors replicate your surface-level features.Agent-speed workflows require infrastructure evolution. Companies that fail to adapt their architecture to agentic workloads will find their switching-cost moat erodes faster than the market expects.Brand in enterprise AI is a reliability signal. Demonstrated production accuracy and governance capability — not benchmark performance — is what enterprise buyers are now paying for.Counterpositioning opportunity exists for CTOs building AI-native tooling on outcome-based pricing. The incumbent’s inability to cannibalize its own seat revenue is your window. |

Conclusion: The Sorting Is the Signal

The a16z thesis is directionally correct, and the M&A market has not yet priced its implications. The 30% ETF decline is not a uniform verdict on software. It is indiscriminate selling in the face of a real structural shift — and indiscriminate selling always creates opportunity for analytical precision.

The Seven Powers framework gives M&A practitioners a rigorous vocabulary for the distinction the market is failing to make. Process power, network effects, proprietary data, and brand are not going away. They are being amplified by AI in the companies that were already building with discipline. The companies without those foundations are facing justified pressure for the first time.

For the M&A market, the implication is clear: apply the moat scorecard before applying the multiple. The SaaSpocalypse, applied properly, is not a risk framework — it is a buying signal.

DevelopmentCorporate LLC is an M&A advisory firm focused on enterprise SaaS transactions. We work with founders approaching exit, PE/VC sponsors evaluating platform acquisitions, and enterprise technology leaders navigating strategic transactions. For a preliminary moat assessment or M&A advisory consultation, contact us at DevelopmentCorporate.com.

Related Reading | AI Valuation Gap · VC Rejection Signals · The SaaSpocalypse Is a Buying Signal · Agentforce Illusion