The Answer Economy: Why AI Search Visibility Is the M&A Due Diligence Gap Nobody Is Pricing

How Generative AI Is Rewiring the Enterprise Software Buying Journey — and What It Means for SaaS Valuations

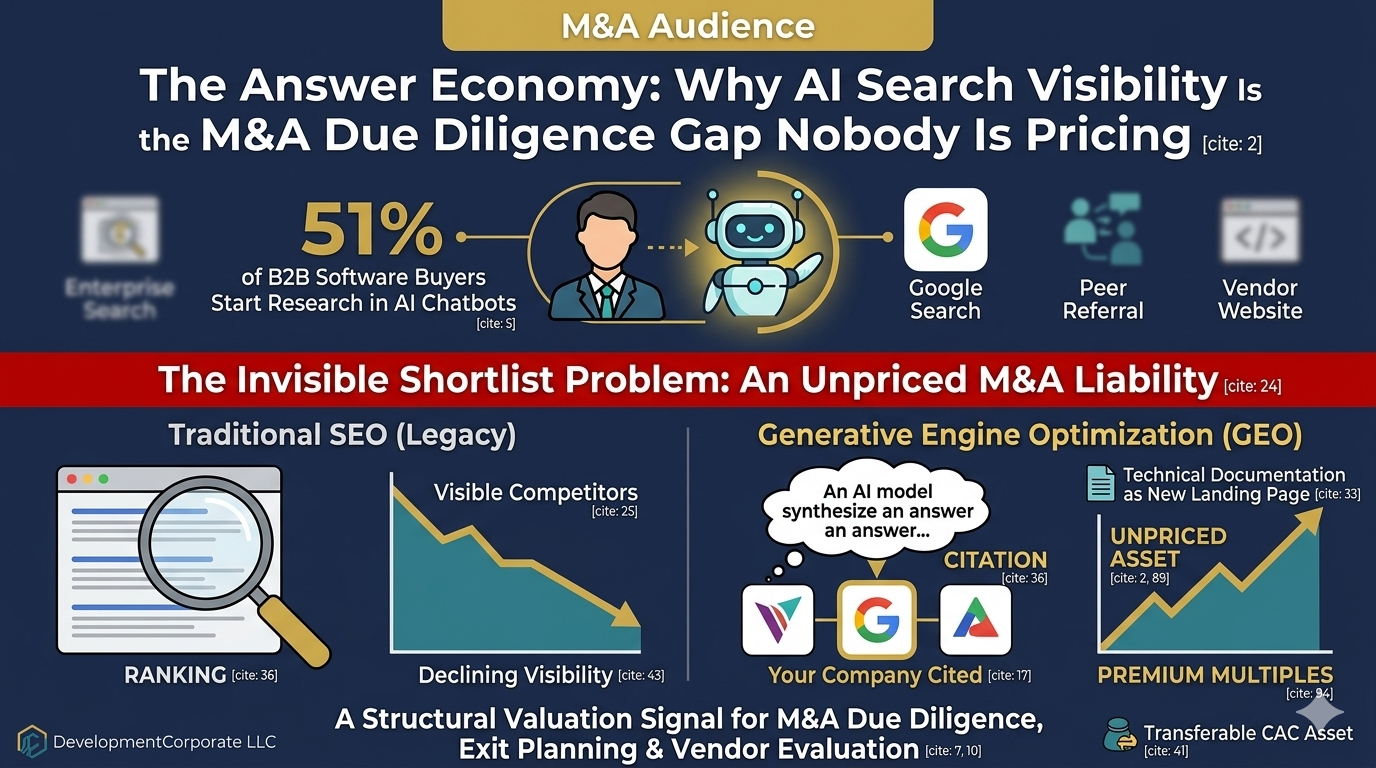

The Answer Economy has arrived, and it is quietly destroying the customer acquisition infrastructure that most enterprise SaaS companies were built on. According to Q1 2026 industry data, 51% of B2B software buyers now initiate their research journey inside an AI chatbot — not Google, not a vendor website, not a peer referral. For M&A practitioners, this statistic is not a marketing curiosity. It is a structural valuation signal that has not yet penetrated deal room practice.

The consensus view among enterprise SaaS operators is that generative AI search is a marketing channel to optimize. That framing is popular, intuitive, and dangerously incomplete. What the data actually reveals is a fundamental rewiring of how enterprise buyers form purchase intent — a shift that creates a new category of transferable asset for companies that have invested in it, and a hidden liability for those that have not.

This analysis reframes the Answer Economy through the lens that matters for our three core audiences: M&A due diligence, exit timing, and vendor evaluation. The implications are more severe — and more actionable — than the marketing playbooks suggest.

Figure 1: Where B2B software buyers start their research journey, Q1 2026. The AI chatbot channel has overtaken Google Search as the primary entry point.

The Post-Search Reality: When Citations Replace Rankings

For twenty years, enterprise software GTM strategy followed a predictable playbook: SEO captured intent, content marketing nurtured leads, and sales reps closed the gap. That architecture assumed a buyer who navigated a list of results and made comparative judgments across multiple vendor pages.

That buyer is disappearing. The new buyer asks a model a specific question — “What is the best agentic AI platform for financial risk management with SOC2 compliance?” — and receives a synthesized answer with three or four named vendors. If your company is not cited in that answer, you have lost the deal before you knew it existed.

69% of enterprise buyers recently chose a different vendor than originally planned because of an AI chatbot recommendation. This is not channel substitution. This is category-level purchase intent rewriting.

The data point that should alarm every SaaS founder approaching an exit: 69% of buyers changed their intended vendor based on an AI chatbot recommendation. This is not a marginal channel effect. It means that nearly seven in ten enterprise software purchase decisions are now being influenced — and frequently redirected — by an algorithm that most SaaS companies have never audited, optimized for, or even measured.

Figure 2: The “Invisible Shortlist” effect. AI chatbot recommendations are actively redirecting enterprise purchase decisions away from pre-selected vendors.

The “Invisible Shortlist” Problem: An Unpriced M&A Liability

In the traditional search model, competitive positioning was observable. You could see your competitors in search results, track your ranking relative to theirs, and adjust your strategy accordingly. In the Answer Economy, the shortlist is invisible. The model constructs it from training data, documentation quality, peer validation signals, and technical specificity — none of which appear in standard due diligence frameworks.

For M&A buyers, this creates a specific and quantifiable risk. A target company’s trailing twelve-month revenue may look healthy, but if that revenue was generated during a period when the company still appeared in AI citations — and has since been displaced by competitors with better documentation or more recent peer reviews — the forward revenue trajectory is impaired in a way that no standard financial model will capture.

What AI Models Actually Index

Enterprise buyers are increasingly using “Deep Research” modes in AI chatbots. They are not searching for broad keywords. They are asking about specific technical constraints: API latency, integration capabilities with legacy ERPs, data residency policies. AI engines answer these questions by parsing technical documentation, public GitHub repositories, and peer review platforms like G2 and TrustRadius. Ninety percent of high-intent buyers then click through to the citations the AI provides — making your documentation the new landing page.

| The Gap Thesis AppliedThe vendor benchmark claim: “We rank #1 on Google for our category.” The production reality: the buyer never searched Google. They asked Claude, and Claude cited three competitors with better-structured technical documentation. The gap between SEO authority and AI citation authority is the new unpriced risk in SaaS M&A. |

From SEO to GEO: The Valuation Implications of Generative Engine Optimization

Standard SEO is about ranking. Generative Engine Optimization — GEO — is about citation. The distinction is not semantic. It represents a fundamentally different asset class in M&A terms, and one that we have been analyzing in detail as part of our advisory framework.

A well-developed LLM citation footprint represents a compounding, algorithm-resistant customer acquisition channel with no click cost. It produces qualified traffic from buyers who have already been pre-educated by the AI response. It generates brand mentions at zero marginal cost per impression. And critically, it is transferable to an acquirer who can sustain and extend the content strategy post-close.

The inverse is equally consequential. A target whose customer acquisition depends primarily on Google PPC spend, without any AI search presence, carries a specific risk: as the proportion of buyer research shifting to AI chatbots accelerates, the cost per acquisition from traditional channels will increase — creating a hidden margin compression that does not show up in trailing metrics but will show up in post-acquisition performance.

Figure 3: The M&A due diligence gap. GEO-optimized SaaS companies outperform on AI citation metrics while legacy SEO-optimized companies carry declining visibility in the channel that now initiates 51% of buyer journeys.

Three Pillars of GEO That Translate to M&A Value

Structural clarity. Models prefer structured data. Clear, semantic HTML with detailed technical specifications in formats that LLMs can easily parse — JSON-LD, structured tables, explicit schema markup — directly increases citation probability. This is measurable, auditable, and transferable.

The source advantage. When 90% of high-intent buyers click through to the citations provided by the AI, your technical documentation becomes the primary conversion asset. Documentation quality is no longer a support function cost center. It is a revenue-generating asset that should be valued accordingly in M&A.

Peer validation signals. AI models heavily weight third-party validation. Mentions in funding trackers, technical forums, and peer review sites are the primary signals for a model to recommend a startup over an incumbent. For PE/VC investors evaluating a portfolio company, the question is no longer just “What is your NPS?” but “How often does your brand appear in AI-generated answers?”

The Mega-Seed Paradox and the Noise Floor Problem

We are currently in an era of mega-seed rounds exceeding $100 million for pre-revenue AI labs. This creates a noise floor that is difficult to pierce for traditional early-stage firms with $5M to $15M seed rounds — the range we documented in our enterprise value analysis of 2025 seed-stage acquisitions.

For senior executives at these companies, a massive funding round by a competitor is a signal of “staying power” to both human buyers and AI models. The visibility strategy for a $10M seed company must rely on technical superiority that is easily verifiable by an AI agent — not marketing spend that only registers on traditional search.

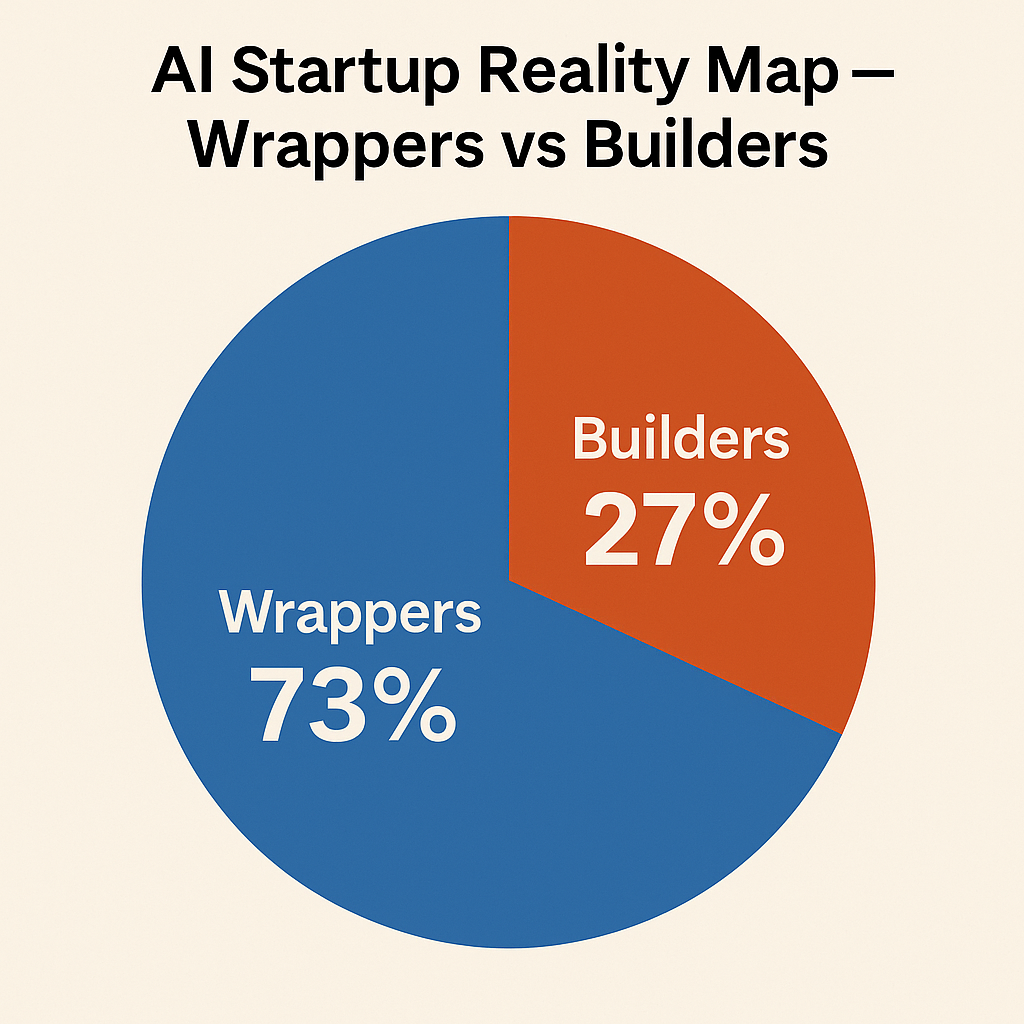

This connects directly to what we found in our analysis of 200 reverse-engineered AI startups: 73% of venture-funded AI companies are primarily thin wrappers on top of foundation model APIs. In the Answer Economy, these companies face a specific existential risk: if an AI model can determine that the underlying technology is not differentiated, it will not cite the company in its recommendations. The wrapper premium evaporates in the exact channel where 51% of buyer journeys now begin.

The visibility strategy for a $10M seed company must rely on technical superiority that is easily verifiable by an AI agent — not marketing spend that only registers on traditional search.

The MQL-to-AQR Transition: A New KPI Framework for M&A Readiness

The operational imperative for executives preparing for a transaction is to shift marketing KPIs from MQLs (Marketing Qualified Leads) to what we are calling AQR — AI Query Relevance: how often does your brand appear in the top three answers for your core category across Claude, ChatGPT, Perplexity, and Gemini?

This is not a theoretical metric. It is measurable today using tools like Profound, Otterly.AI, and Semrush’s AI Toolkit, as we detailed in our AI Search Visibility Audit analysis. The companies that can demonstrate a rising AQR trend during diligence will have a concrete, data-backed story for why their customer acquisition cost is declining while their close rates are improving — the exact narrative that commands premium multiples.

The Executive Playbook: Three Actions Before Your Next Board Meeting

1. Audit Your AI Footprint

Run 50 queries across Claude, ChatGPT, and Perplexity using the exact pain points your customers describe in discovery calls. If your company does not appear in at least 20% of the citations, your “invisible” market share is zero. Identify the training data gap: is it a lack of technical documentation, or a lack of third-party peer reviews? The distinction determines the investment required.

2. Invest in Technical Content Over Thought Leadership

Generic thought leadership is easily ignored by both humans and LLMs. Deep, technical documentation that explains how your product solves a specific problem — complete with code snippets, schema definitions, and architecture diagrams — is the fuel that generative engines use to recommend you. As we noted in our AI valuation gap analysis, the distinction between “AI-adjacent” and “AI-driven” determines whether you qualify for premium multiples. The same logic applies to content strategy: surface-level content gets surface-level citation.

3. Leverage the Rep-Free Journey

Since 67% of enterprise buyers want a rep-free experience, your website must function as an autonomous sales environment. Interactive AI assistants, self-serve sandboxes, and transparent pricing are no longer differentiators — they are table stakes for the buyer segment that now represents the majority of enterprise software research. The Agentforce Illusion analysis showed that buyers who adopted commercial AI after failed internal builds are buying out of necessity, not conviction. The rep-free journey is how you convert that necessity into closed revenue.

What This Means for You

| ▶ PE/VC InvestorsAdd AI search visibility assessment to your due diligence checklist immediately. A target with a strong and growing LLM citation footprint has a compounding, zero-cost customer acquisition channel that is transferable post-close. A target with zero AI search presence carries a hidden CAC liability that will compress margins within 12–18 months of close. Neither metric appears in trailing financials. Both appear in post-acquisition performance. See our M&A due diligence checklist for the full framework. |

| ▶ SaaS FoundersIf you are considering an exit in the next 12–24 months, your GEO investment window is closing. AI citation footprint takes 6–12 months of sustained technical content production to build. The founders who invest now will enter diligence with a measurable, differentiated asset. The founders who wait will enter diligence with a marketing channel that is visibly losing share to a channel they never participated in. As we documented in our AI SaaS investment trends analysis, VCs are already flagging companies in “dead zones” where AI agents will soon do the same job better and cheaper. |

| ▶ Enterprise CTOs/CPOsEvaluate your vendor stack through the GEO lens. Vendors with strong AI citation footprints are more likely to be recommended to your peers, which means they are attracting a broader user base, which means they are iterating faster on product. Vendors that are invisible to AI chatbots are losing the R&D feedback loop that comes from being discovered by technical evaluators. The McKinsey Lilli security analysis showed that enterprise AI deployments require rigorous security evaluation. Apply the same rigor to evaluating whether your vendors are keeping pace with how buyers now discover software. |

The Future Is Synthesized — and the Market Has Not Priced It

The enterprise software buying journey is no longer a funnel. It is an answer. The 33% of buyers who are now discovering their vendors through AI alone represent the leading edge of a structural shift that will reach majority adoption within 18 months.

For the M&A market, the implications are clear: AI search visibility is now a measurable, transferable asset with direct consequences for customer acquisition cost, brand authority, and long-term revenue resilience. The market has not yet priced this. Standard due diligence frameworks do not include AI search audits. Most SaaS companies have no systematic process for measuring their LLM citation footprint.

That gap creates opportunity — for founders who invest in GEO before a transaction, for buyers who incorporate AI visibility analysis into their acquisition screening, and for advisors who can quantify this dimension of digital asset value.

At DevelopmentCorporate, we are incorporating AI search visibility assessment into our advisory framework for clients approaching M&A transactions. The companies that master GEO and the nuances of the Answer Economy will not just survive the transition from search to synthesis — they will command the premium multiples that come with owning a customer acquisition channel the market has not yet learned to value.

About the AuthorJohn Mecke is Managing Director at DevelopmentCorporate LLC, where he advises SaaS executives and startup founders on M&A strategy, competitive positioning, and exit planning. With over 30 years in enterprise technology, John has led six global product management organizations and personally led five acquisitions totaling over $175 million in consideration.