The SaaS-Pocalypse Is a Buying Signal

What PitchBook’s $5.4 Trillion AI Taxonomy Reveals About SaaS M&A Agentic AI Opportunity in 2026

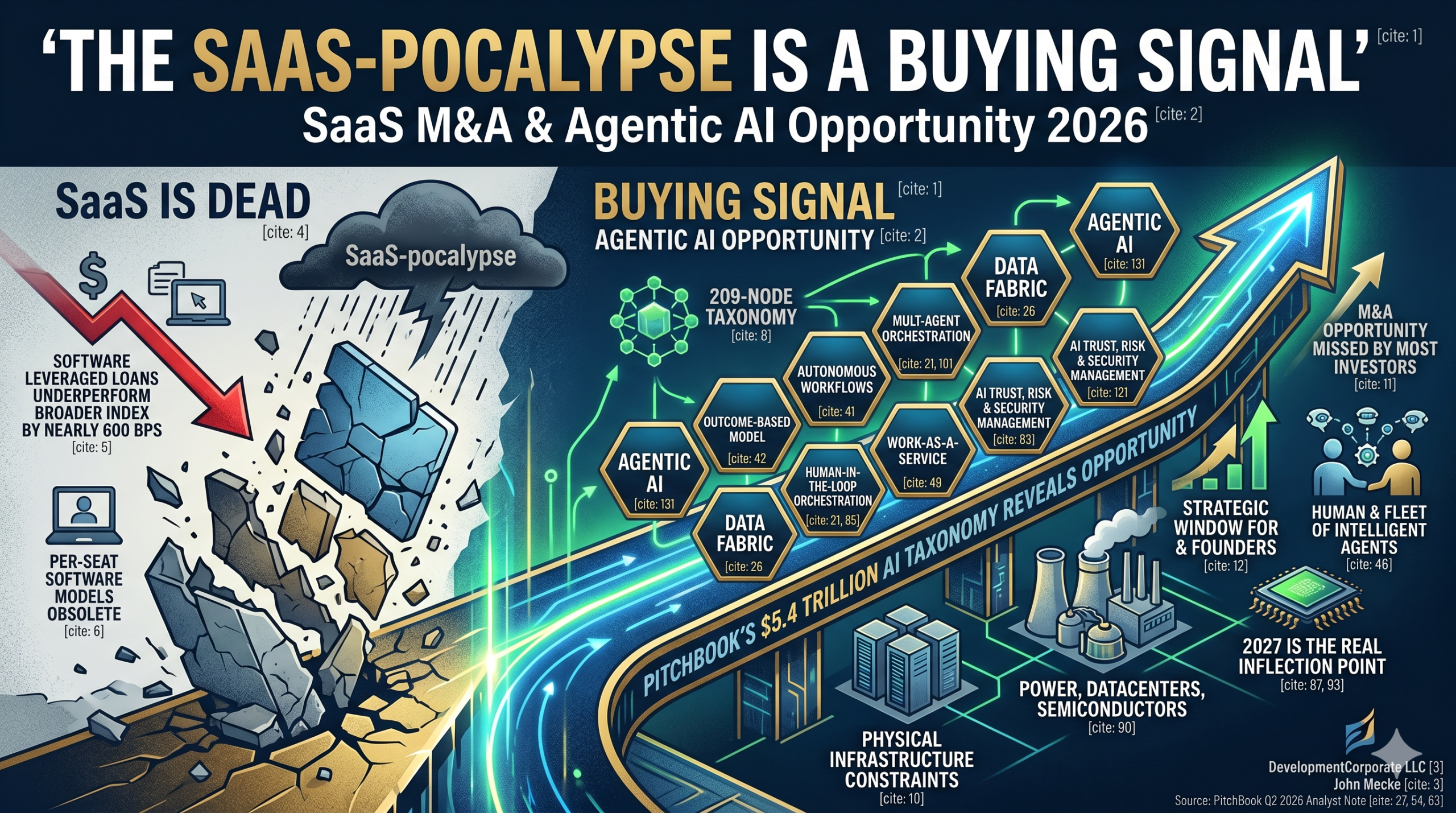

SaaS is dead. At least, that is what the credit markets believe right now. As of April 2026, software leveraged loans have underperformed the broader loan index by nearly 600 basis points year-to-date, according to PitchBook and the Morningstar LSTA US Leveraged Loan Index. Oracle is laying off employees. Block is rightsizing. Every LinkedIn post features some variation of the same thesis: agentic AI will eliminate the per-seat software model, autonomous agents will replace human workers, and legacy SaaS companies will be rendered obsolete within months.

Here is the problem with that story. It is directionally correct and temporally catastrophic.

PitchBook’s Q2 2026 Analyst Note, The SaaS-Pocalypse Opportunity, published on May 8, 2026, introduces a 209-node taxonomy tracking $5.4 trillion in global enterprise IT and hyperscaler capital expenditure. The report places us squarely in the ‘Investor Confusion’ phase of the AI adoption curve. But the same report also projects a five-to-ten year transition timeline constrained not by software readiness, but by physical infrastructure: power permitting, leading-edge manufacturing availability, and enterprise IT budget reallocation cycles.

The gap between the market’s panic pricing and the actual pace of structural transition is the M&A opportunity that most investors are missing entirely.

This article examines what PitchBook’s taxonomy reveals, why the conventional SaaS-pocalypse narrative overstates immediacy while understating the strategic window, and what PE/VC investors, SaaS founders, and enterprise technology leaders should actually do in the next 12 to 24 months.

The $5.4 Trillion Map: Why the Old Categories Are Broken

For decades, enterprise technology analysts organized software markets into familiar buckets: enterprise software, IT hardware, networking, and cloud infrastructure. These categories worked well enough when the dominant business model was selling per-seat licenses to human users executing defined workflows. They no longer capture reality.

PitchBook’s three-tree taxonomy replaces these legacy categories with a far more granular architecture designed around investment stack, total addressable market, and industry sector. The most granular level — what PitchBook calls the ‘deployment’ node — groups companies into 209 mutually exclusive sub-industries. No single technology product can belong to more than one deployment group, though companies with diverse product portfolios can span several.

The sheer scope of this taxonomy matters for M&A practitioners. When PitchBook identifies 15 deployment sub-industries within Agentic AI alone — including HITL exception routing, agentic evaluation and simulation, agentic memory and state management, multi-agent orchestration, autonomous code agents, autonomous cyber agents, and autonomous marketing agents — it is signaling that the ‘AI’ category as conventionally understood is meaninglessly broad for investment or diligence purposes.

The framework also maps physical-to-digital interdependencies that most software-centric analyses completely miss. True high-fidelity digital labor cannot scale until the lower layers of the physical stack are buildout-complete: foundational hardware inputs, hyperscale compute clusters, gigawatt-scale power generation, and specialized datacenter construction. PitchBook’s taxonomy traces these linkages explicitly, connecting chemical firms supplying semiconductor materials to heavy civil contractors pouring concrete for mission-critical datacenters.

Figure 1: PitchBook AI Taxonomy — Deployment Count by Map Category. Agentic AI (15) and Data Fabric (14) lead the software layer; Physical Infrastructure categories reflect the foundational build-out that must precede agentic scale. Source: PitchBook Q2 2026 Analyst Note; DevelopmentCorporate Analysis.

For SaaS M&A practitioners, this taxonomy provides a forcing function that abstract AI narratives cannot: it demands granular competitive segmentation before any investment or acquisition decision. The question is not ‘is this company an AI company?’ — virtually every software vendor claims that label. The question is which of the 209 deployment nodes does this company actually occupy, and is that node growing, contracting, or being cannibalized? We have been developing this analytical framework across our enterprise SaaS M&A Q3 2025 analysis, and PitchBook’s taxonomy now provides the definitional infrastructure to make it rigorous.

The Four-Stage Transition: Why ‘SaaS Is Dead’ Is Both True and Wrong

PitchBook lays out a four-stage transition model from traditional SaaS to what they call the Work-as-a-Service (WaaS) economy, projected to play out between 2026 and 2030 for early adopters and over a full decade for most industries.

Stage 1: Traditional SaaS (2004–2025)

The baseline model that has defined enterprise software for two decades. Software is sold as per-seat subscriptions to accelerate human workflows. Tools like Salesforce, ServiceNow, Asana, and Workday are purchased by organizations to help humans do their jobs faster. Human capital is valued for executing manual tasks and billing for time. The software is a productivity multiplier; the human is still the economic unit.

Stage 2: Service-as-Software (2025–2027)

The first phase shift. PitchBook uses the term SaS (Service-as-Software) to describe the transition from static seat-based tools to autonomous workflow engines. Software vendors stop selling access and start selling outcomes. The economic unit shifts from the licensed user to the completed task. Human capital is re-concentrated in agent-aided revenue-generating functions: customer experience, customer success, customer intelligence, and governance management. This is where we currently sit — right at the inflection between Stage 1 and Stage 2.

Stage 3: Individuals as Platforms (2027–2029)

Human capital is freed from manual execution entirely. Individual professionals stop being task executors and become orchestrators of specialized AI agent fleets. The individual becomes a scalable platform, leveraging digital labor to amplify creativity, empathy, and strategic judgment. Enterprise value migrates from headcount to orchestration capability.

Stage 4: Work-as-a-Service (2030+)

The AI economy fully realized. The fundamental unit of economic production transitions from the billable hour to the guaranteed outcome. Enterprises no longer purchase software seats or hire for execution capacity. They subscribe to human-led platforms that deliver SLA-backed results at machine speed.

Figure 2: The Four-Stage WaaS Transition (2026–2030). PitchBook places the current moment at the Investor Confusion phase between Stage 1 and Stage 2. Physical infrastructure constraints — not software readiness — determine the transition pace. Source: PitchBook Q2 2026 Analyst Note; DevelopmentCorporate Analysis.

Here is the contrarian insight that the market panic obscures: PitchBook explicitly projects that agentic AI will be viable for widespread enterprise deployment in late 2027 — not 2026, not this quarter. The transition is real. But it operates at the speed of power permitting and leading-edge manufacturing availability, not at the speed of model capability improvements. Enterprise IT budget reallocation cycles typically run 18 to 36 months. The companies experiencing loan covenant stress today are not necessarily the companies that will be structurally impaired by 2028. Many of them are being indiscriminately marked down by credit markets applying a generic ‘SaaS disruption’ discount that has not been calibrated against actual deployment timelines or durable moat analysis.

| 📊 FOR PE/VC INVESTORS: The Mispriced Opportunity WindowCredit market stress in software leveraged loans is creating a temporary dislocation between panic pricing and fundamental value. PitchBook’s taxonomy identifies specific deployment categories where legacy incumbents possess genuinely durable economic moats — deep vertical integration, proprietary data assets, and switching costs that agentic AI cannot replicate on a 12-24 month horizon. The actionable thesis: stress-test target company moats against the 209-node taxonomy before applying a blanket SaaS disruption discount. Legacy software with identifiable moats in System-of-Record categories (ERP, Clinical EHR, Financial Management, Revenue Cycle Management) should trade at lower discounts than the market is currently applying. Meanwhile, the same dislocation is creating compressed entry points for AI-native platform acquisitions in Agentic AI deployment nodes — specifically autonomous code agents, multi-agent orchestration, and HITL exception routing — before mainstream PE discovers these categories. |

The Credit Market Signal: What Loan Returns Tell M&A Buyers

PitchBook’s analyst note includes a striking chart that deserves more attention than it has received: US leveraged loan returns for 2026, broken down into all loans versus software-specific loans. As of April 27, 2026, software loans had underperformed the broader loan index by approximately 500 to 600 basis points from peak spread — a level of sector-specific credit stress not seen since the 2022-2023 rate shock that compressed SaaS multiples across the board.

Figure 3: US Leveraged Loan Returns — Software vs. All Loans (2026). Software credit underperformed the broader index by ~600 basis points from peak to trough in Q1 2026. Source: PitchBook | LCD, Morningstar LSTA US Leveraged Loan Index (as of April 27, 2026).

Two interpretations of this data compete for attention. The bearish read — dominant in credit markets right now — is that software loan spreads are widening because the underlying business models are impaired: declining ARR growth, NRR compression, and the secular shift away from per-seat licensing are making these credits genuinely riskier. The bullish read — the one PitchBook’s taxonomy supports — is that credit markets are applying a non-discriminating disruption discount that conflates structurally impaired software with genuinely durable software infrastructure that will remain mission-critical through and after the agentic transition.

This distinction has significant implications for SaaS M&A due diligence. A software company operating in the Financial Audit and Reporting deployment node is not the same credit risk as a generic knowledge management SaaS with no AI integration roadmap. The market is pricing them similarly.

We have written previously about the 35-point AI valuation expectation gap between what buyers expect (86% of targets to be AI-driven in 2026) and what they are actually finding in diligence (63% of 2025 targets had only limited AI use). The credit market dislocation amplifies this gap: sponsors with PE-backed software companies facing loan covenant pressure may be forced to transact at valuations that do not reflect their actual AI moat durability.

Jevons Paradox and the Human Capital Counterintuitive

One of the most important analytical contributions in PitchBook’s note is the application of Jevons Paradox to the AI economy — and the implications it carries for anyone building a workforce displacement thesis for SaaS M&A.

Jevons Paradox, first articulated by English economist William Stanley Jevons in 1865, observes that when a resource becomes more efficient to use, total consumption of that resource typically increases rather than decreases. In the context of AI: as the cost per token of intelligence drops toward zero, the total quantity of intelligence consumed grows, not shrinks. More AI usage, not less human employment — at least in the near term.

PitchBook’s formulation is precise: AI will consume tasks, not jobs. The global economy will experience temporary skills dislocation, not human obsolescence. The aggregate demand for human capital will reach an all-time high for those who can direct digital agents, manage physical AI integration, and maintain human-to-human trust relationships. This has happened in every prior technology platform transition — from mechanical automation to enterprise software — and AI is following the same pattern, just faster.

For SaaS M&A practitioners, the Jevons Paradox insight carries a specific implication: the ‘software seats eliminated by AI agents’ narrative systematically underestimates the new categories of digital labor management, agent governance, and human-in-the-loop oversight that will emerge as AI scales. Deployment categories like Digital Labor Workforce Management, HITL Exception Routing, Agentic Evaluation and Simulation, and AI Trust, Risk and Security Management are not abstract future-state categories — they are active investment areas that PitchBook identifies as current market leaders in the taxonomy today.

The investment thesis is not to avoid SaaS because AI will destroy it. The thesis is to identify which SaaS companies are positioned to own the human-in-the-loop orchestration layer as AI scales — and acquire them before the mainstream realizes that the agentic economy requires more enterprise software, not less, just different enterprise software.

| 🚀 FOR SAAS FOUNDERS: The Exit Window Is Time-SensitivePitchBook’s taxonomy provides a precise self-assessment framework: which of the 209 deployment nodes does your product occupy, and how durable is that position against AI-native alternatives? If your product operates in what VC firms have labeled ‘dead zone’ categories — thin workflow automation with no proprietary data moat, generic point solutions that AI agents can replicate in 6-9 months — the strategic clock is running. Legacy software incumbents are actively seeking agentic-native acquisitions to survive their own transition. That means there is currently a motivated buyer pool for agentic-native startups with genuine deployment node leadership. If you are a founder with proprietary data assets, deep vertical integration, or governance and compliance capabilities in AI oversight, the next 18 months represent a premium exit window before the acquirer universe narrows to only the largest strategics who have completed their own AI transitions. |

The Physical Bottleneck Thesis: Why 2027 Is the Real Inflection Point

The single most important constraint on the SaaS disruption timeline is not model capability, regulatory environment, or enterprise AI readiness. It is physical infrastructure.

Deploying hundreds of millions of autonomous agents at enterprise scale requires a massive physical buildout: hyperscale datacenters with advanced liquid cooling architectures, dedicated baseload power generation at gigawatt scale, and advanced semiconductor fabrication capacity that does not yet exist at the required volume. PitchBook’s taxonomy explicitly maps these dependencies — from power management integrated circuits to wafer fabrication equipment to colocation real estate — as the foundational constraints that determine the pace of the agentic transition.

AMD, NVIDIA, OpenAI, Anthropic, Broadcom, and the major hyperscalers all made announcements throughout 2025 that implied large-scale next-generation AI factories would come online in late 2027. PitchBook’s projection aligns precisely with that timeline: current hyperscaler capital expenditure in 2026 focuses on datacenter upgrades; large-scale next-generation AI factories come online in late 2027; agentic AI becomes viable for widespread enterprise deployment by late 2027.

This five-year transition horizon is fundamentally incompatible with the credit market’s current pricing of software loan stress. If agentic AI does not achieve enterprise deployment scale until late 2027, legacy SaaS companies with durable system-of-record positions have 18 to 24 months of relatively stable ARR before structural disruption arrives — longer than most leveraged loan covenants assume.

The implication for M&A buyers is specific. Acquirers who apply a generic ‘AI disruption’ discount to all SaaS targets without running them through the taxonomy are making the same analytical error we identified in our analysis of The Agentforce Illusion: treating a directionally correct macro narrative as if it applies uniformly across all software categories at the same pace and magnitude.

Build vs. Buy: The Strategic Imperative for Legacy SaaS Incumbents

PitchBook’s note makes one strategic prediction with unusual clarity: legacy software companies will seek acquisitions of agentic-native startups to survive or drive their transition. This is not speculative. It is the M&A playbook that has characterized every enterprise software platform transition cycle, from the client-server to web to cloud transitions.

The taxonomy provides the analytical framework for identifying which agentic-native acquisition targets are most strategically valuable to which legacy incumbents. The key is mapping deployment node adjacency: a legacy CRM vendor seeking to own the outcome-based digital labor layer should be acquiring in the Sales Automation autonomous agent node, the Autonomous Personal Assistant deployment, or the HITL Exception Routing category. A legacy ERP vendor seeking to survive the transition to Service-as-Software should be acquiring in the Business Process Intelligence and Mining node or the Digital Labor Workforce Management deployment.

The VC dead zone analysis we published earlier this year identified precisely which SaaS categories institutional investors are declining to fund on a go-forward basis. Those dead zone categories — where AI agents will replicate the core product in 6 to 9 months — are exactly the categories that legacy SaaS incumbents should be exiting through divestiture or consolidation, while simultaneously acquiring in the agentic-native adjacent nodes that will define their survival.

The build-versus-buy calculus has shifted decisively toward buy for established software incumbents. Building agentic capabilities organically requires 18 to 36 months of internal development, talent acquisition at a premium, and the organizational reengineering necessary to shift from a seat-license mentality to an outcome-delivery architecture. Acquiring an agentic-native startup in the right deployment node compresses that timeline to 6 to 12 months of integration — and the current credit stress environment is creating compressed entry prices that make the buy case even more compelling.

The New SaaS M&A Agentic AI Diligence Framework

PitchBook’s 209-node taxonomy is not just an investment mapping tool. It is a diligence framework. For any SaaS M&A transaction in 2026, the following questions must be answered before an investment decision:

- Which of the 209 deployment nodes does the target company’s primary product occupy? Is that deployment node growing, stable, or facing near-term agentic replacement risk?

- Does the target possess a durable economic moat in that deployment node — proprietary data assets, deep workflow integration, regulatory compliance positioning, or network effects that AI-native alternatives cannot replicate within 24 months?

- Is the target’s pricing model structured to capture agentic usage? Per-seat models with no consumption-based or outcome-based component will face structural ARR compression as AI agents replace human users.

- What is the target’s position in the physical-to-digital stack dependency chain? Companies in Agentic Memory and State Management, AI Tool Integration and Context Protocols, or MCP Interface Gateways benefit directly from hyperscaler infrastructure buildout.

- Is the target’s management team executing a credible SaS transition roadmap — or are they defending the existing per-seat model as if the transition is not coming?

This framework is a direct extension of the AI valuation gap analysis we have been developing over the past two quarters: the 35-point gap between buyer AI expectations and target AI reality is now addressable using PitchBook’s taxonomy as the analytical map. The taxonomy allows buyers to move beyond generic ‘AI-driven vs. non-AI-driven’ categorizations and into specific deployment node analysis that calibrates the actual disruption risk and opportunity for each target.

| 🏗️ FOR ENTERPRISE CTOs/CPOs: Vendor Risk Meets Infrastructure RealityPitchBook’s physical-to-digital interdependency map has direct implications for enterprise software procurement. Vendors occupying thin-layer point solution nodes without proprietary data integration face the highest replacement risk from agentic AI. Vendors in System-of-Record deployment nodes — EHR, ERP, Financial Management, Revenue Cycle Management — have deeper moats and longer runway. Two tactical recommendations: First, accelerate contract renegotiations with thin-layer vendors before they face financial distress — the leverage is yours now. Second, extend contract commitments and deepen integration with System-of-Record vendors who are investing credibly in agentic-native upgrades. The Governance deployment nodes in PitchBook’s taxonomy — AI Trust, Risk and Security Management, Digital Labor Workforce Management, Algorithmic Liability and Cyber Insurance — are the categories your enterprise will need most as agentic AI deploys at scale. Evaluate these vendors now, before the market discovers them. |

Capital Deployment in the Confusion Phase: Where the Money Is Going

PitchBook’s AI adoption expectation curve places us explicitly in the ‘Investor Confusion’ phase — the trough between inflated expectations and investor confidence. This is historically where the best risk-adjusted returns in technology M&A have been generated. The Q3 2025 enterprise SaaS M&A data we analyzed late last year showed exactly this pattern: headline deal volume masked valuation compression for non-premium assets, while category-leading platforms with genuine moats continued to attract premium acquisition prices.

PitchBook’s framing is instructive: ‘The current market turmoil is an opportunity for investors and strategy officers to assess the entire AI ecosystem at the most granular level of our taxonomy and deploy capital into companies with the strongest product-market fit that are geared for the new human-accelerated AI economy.’ The key phrase is human-accelerated. Not human-replaced. Not human-obsolete. Human-accelerated.

PitchBook’s taxonomy provides a precise sequencing of where the $5.4 trillion in combined enterprise IT and hyperscaler spending is actually flowing:

- Physical infrastructure first: Advanced semiconductor fabrication, gigawatt-scale power generation, specialized datacenter construction. Capital is flooding the foundational layers before agentic software can scale.

- Platform layer second: Agentic AI deployment nodes — particularly multi-agent orchestration, autonomous code agents, and enterprise AI search and knowledge discovery — are attracting disproportionate venture investment as the software layer closest to agentic deployment.

- Application software third: The transition from per-seat SaaS to Service-as-Software in application categories (CRM, ERP, HCM) is real but slower — governed by enterprise contract renewal cycles and organizational change management timelines, not by technical readiness.

The sequencing matters for M&A strategy. Physical infrastructure buildout peaks in 2026-2027. Platform layer investment peaks in 2027-2028. Application software disruption manifests most fully in 2028-2030. An M&A strategy calibrated to this sequence — acquiring platform layer assets now, at confusion-phase valuations, before the application software disruption becomes undeniable — is the thesis that PitchBook’s taxonomy most directly supports.

The Private Credit Cascade and SaaS Exit Timing

One structural factor that PitchBook’s note does not fully develop — but which is directly relevant to SaaS M&A timing — is the private credit market stress cascade. The software leveraged loan underperformance visible in PitchBook’s chart is not just a public market signal. Private credit lenders, including Business Development Companies (BDCs) and direct lending funds that have provided the majority of PE software deal financing since 2020, face the same repricing pressure on their software loan portfolios.

When private credit lenders to PE-backed software companies begin to see covenant stress, the cascade effect flows through exit timelines. PE sponsors holding software assets acquired at 2021-2022 peak multiples, financed with private credit at elevated leverage ratios, face converging pressures: deteriorating loan performance, limited IPO window access, and a strategic buyer universe that is itself focused on AI transition strategy rather than opportunistic SaaS consolidation. The forced-exit dynamic this creates is exactly the kind of distressed acquisition opportunity that historically rewards well-capitalized strategic buyers and PE funds with genuine dry powder.

For SaaS founders evaluating exit timing outside the PE-sponsored context, the private credit cascade provides a different but equally important signal: the buyers most likely to transact at premium valuations today are strategic acquirers, not PE-backed platforms. Legacy software incumbents pursuing AI transformation have both the strategic imperative and the balance sheet capacity to pay premium multiples for agentic-native assets. PE sponsors are, in many cases, managing existing portfolio stress rather than aggressively acquiring new assets. This mirrors the pattern we identified in our AI funding apocalypse analysis: capital concentration is narrowing, and the window for founder-favorable exits is time-bounded.

Conclusion: The Taxonomy Is the Strategy

Every technology disruption cycle produces the same analytical error: the market prices the long-run structural outcome into near-term valuations, ignoring the transition timeline constraints that slow the actual pace of disruption. The dot-com era priced the internet’s ultimate dominance into 1999 valuations, collapsing in 2000-2002, then recovering to confirm the long-run thesis by 2010. The 2021 SaaS peak priced cloud software’s long-run dominance into multiples that compressed 60-80% as interest rates normalized.

The SaaS-pocalypse narrative is doing the same thing: it is pricing the 2030 outcome — agentic AI displacing per-seat software models at scale — into 2026 loan and equity valuations. PitchBook’s taxonomy is the corrective instrument. It maps the 209 deployment nodes of the $5.4 trillion AI ecosystem, traces the physical-to-digital interdependencies that constrain transition timing, and places the current moment precisely at the Investor Confusion phase — not the end of software value creation, but the temporary dislocation that precedes the next investment cycle.

The SaaS M&A agentic AI opportunity is not abstract. It is specific, taxonomically mappable, and time-bounded. The companies that will generate the strongest risk-adjusted returns over the next three to five years are those that use frameworks like PitchBook’s 209-node taxonomy — combined with granular diligence on deployment node moat durability, physical stack dependency, and transition timeline calibration — to find the buying signals hidden inside the market’s panic.The SaaS-pocalypse is real. The opportunity within it is larger. And the analytical tools to find it now exist. Contact DevelopmentCorporate to discuss how these frameworks apply to your specific acquisition strategy or exit planning process.