SaaS Private Credit Lenders Are Done With ARR. Your M&A Buyer Will Be Too.

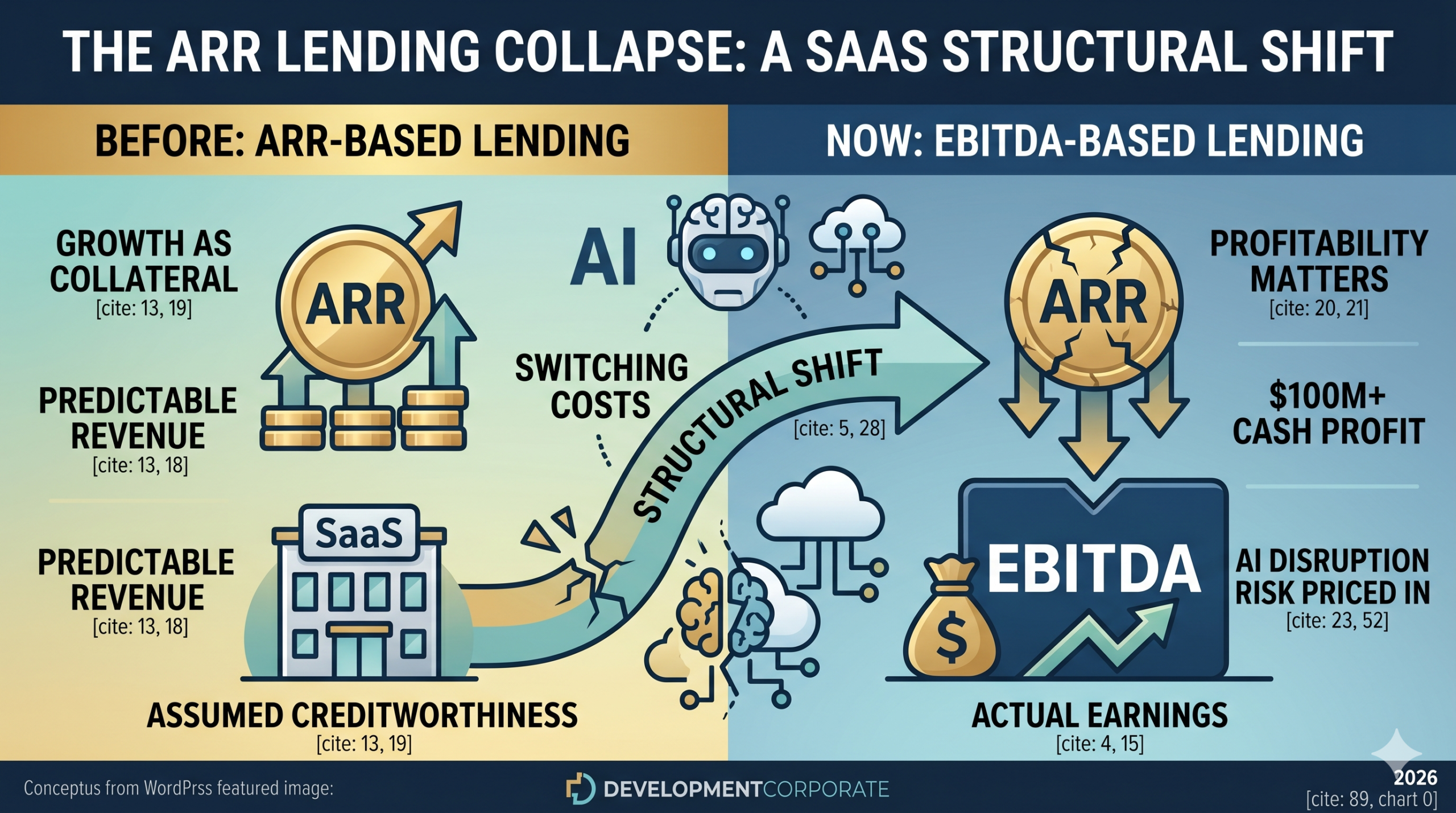

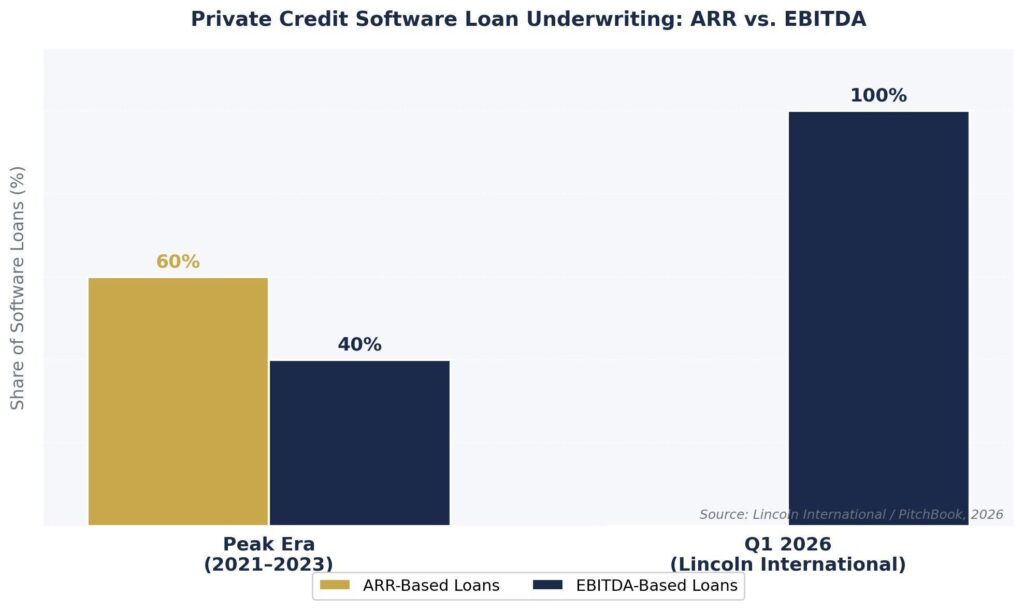

SaaS private credit lenders have made a decision that every SaaS founder and PE sponsor needs to hear: ARR is no longer sufficient collateral for a loan. Of the eight software loans that Lincoln International placed in the first four months of 2026, not one was underwritten on annual recurring revenue. All eight were priced on EBITDA — the old-fashioned measure of what a company actually earns after paying its bills.

That is not a random data point. It is a structural shift — one that signals a wholesale reassessment of whether SaaS subscription revenue is as durable, predictable, and creditworthy as lenders spent five years assuming it was.

And here is the part that should alarm founders approaching a sale: the logic that killed ARR loans is the same logic that M&A buyers are now applying to acquisition multiples. Private credit lenders got there first. Equity buyers are arriving next.

This analysis unpacks what the ARR lending collapse means — for the private credit market, for SaaS M&A valuations, and for founders and PE sponsors trying to navigate what comes next. We also explore our previously published JPMorgan software loan markdown analysis, which identified this dynamic months before it became consensus.

Figure 1: Private credit software loan underwriting has shifted entirely from ARR to EBITDA in 2026. Source: Lincoln International / PitchBook.

How ARR Became the Gold Standard — and Why It Isn’t Anymore

The rise of ARR-based private credit lending was a product of a specific moment in economic history. Between 2020 and 2023, with interest rates near zero and venture-backed SaaS companies growing at 30% to 50% annually, private credit lenders made a calculated bet: subscription revenue from enterprise software was sticky, predictable, and therefore creditworthy — even if the borrower was burning cash.

At the height of the market, software borrowers secured ARR loans at 525 to 550 basis points over the benchmark rate, with loan-to-value ratios of 30% to 35% — a structure rarely seen in the syndicated loan market. Lenders were comfortable lending against revenue that hadn’t yet converted to profit, betting those revenue streams would hold through the loan maturity and eventually flip into EBITDA-based covenants.

The logic had three pillars. First, switching costs: enterprise SaaS customers don’t churn easily. The cost and disruption of replacing core software was seen as a natural protection for revenue streams. Second, subscription predictability: recurring monthly and annual payments were measurable and forecastable in ways that cyclical revenues were not. Third, growth trajectory: even cash-burning SaaS companies were adding ARR fast enough that time was on the lender’s side.

AI has systematically undermined all three pillars.

| “AI’s disruption to many SaaS products has made the ARR bet more complicated. Lenders are starting to question the durability of these revenue streams.” — PitchBook LCD, April 2026 |

The February 2026 SaaS-pocalypse — the wave of selloffs triggered by concerns about AI’s ability to automate or replace entire categories of software functionality — crystallized what had been building for 18 months. Lenders who spent 2020–2023 competing to underwrite ARR-based software loans are now doing the opposite: requiring EBITDA, demanding at least $100 million in cash operating profit for most deals, and widening spreads by 100 basis points or more versus commitments made just months earlier.

For a deeper look at how these credit dynamics map to M&A valuations, see our SaaS-Pocalypse Buying Signal analysis, which identifies which software categories remain creditworthy — and acquirable — despite the market dislocation.

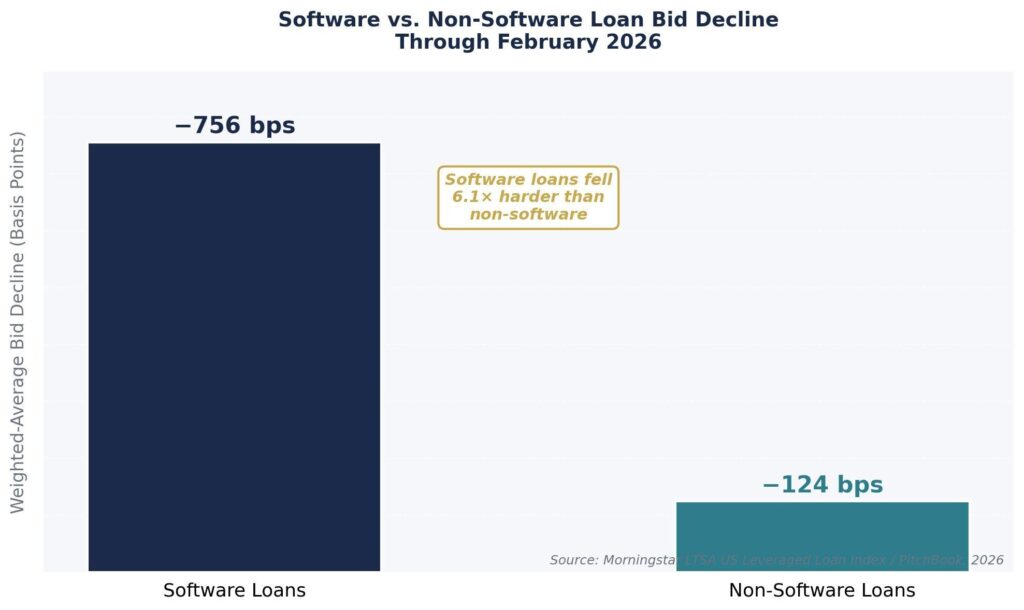

The Bid Decline That Makes This a Structural Problem, Not a Cyclical One

The scale of the software loan repricing is unlike anything in recent memory. Through the end of February 2026, the weighted-average bid for software loans tracked by the Morningstar LTSA US Leveraged Loan Index dropped by 756 basis points — the steepest decline since the onset of COVID-19.

The comparison to non-software loans is what makes this structural rather than cyclical: non-software loans dropped only 124 basis points over the same period. Software loans fell more than six times harder than the rest of the credit market. This is not a rate environment story. It is a sector-specific reassessment of credit quality.

Figure 2: Software loans declined 756 bps through Feb. 2026 — more than 6× the 124 bps decline in non-software loans. Source: Morningstar LTSA / PitchBook.

The Pro Forma Problem

Lenders are also turning aggressive on one of the most common practices in leveraged buyout financing: pro forma EBITDA adjustments. Historically, private credit deals have included EBITDA adjustments averaging 20% to 30% of total EBITDA — add-backs for one-time costs, run-rate savings from announced headcount reductions, and revenue ramps from newly signed contracts. That flexibility is now severely curtailed.

Lenders are increasingly skeptical of run-rate revenue that has not yet materialized — whether from price increases, newly signed contracts, or planned workforce reductions. For PE sponsors who built their acquisition models on generous EBITDA adjustments, this creates a compounding problem: the multiple they paid was based on adjusted EBITDA that lenders may no longer recognize.

Club Deals as a Confidence Signal

A behavioural change in how large software loans are structured offers a revealing window into lender confidence. For bigger transactions, lenders are increasingly opting to “club up” — sharing underwriting across multiple credit funds rather than underwriting solo. Seeing other lenders review the book and join in now serves as a sanity check, giving participants greater confidence to stay in a deal. When underwriting confidence was high, a single lender could carry a software deal alone. The move to club structures signals that confidence is no longer high enough to go it alone.

The M&A Parallel: What Happened in Credit Will Happen in Equity

Private credit lenders are typically ahead of the equity M&A market in repricing risk. They have financial covenants, loan monitoring, portfolio mark processes, and direct legal remedies that force a faster reckoning with credit quality than equity valuations, which are driven by narrative and comparables. When credit markets reprice, equity M&A follows — usually 6 to 18 months later.

The ARR lending collapse is therefore a leading indicator for SaaS M&A multiples. The underlying logic is identical:

- ARR durability is now in question. If a lender won’t underwrite against your recurring revenue, a buyer’s DCF model will assign a steeper discount rate to those same cash flows.

- Pro forma adjustments are being challenged. M&A buyers are applying the same skepticism to seller-provided EBITDA add-backs that credit funds are now rejecting.

- AI disruption premium is being priced in. Just as lenders now demand $100M+ EBITDA floors as a buffer against AI disruption, acquirers are demanding AI-defensibility evidence before paying premium multiples.

Our AI Valuation Gap analysis documents this dynamic in detail: 83% of M&A buyers now pay higher multiples for AI-native or AI-integrated targets, and 85% cite commoditization risk from AI as their biggest long-term concern about SaaS cash flow durability. The credit market is pricing the same concern — just via spread widening rather than multiple compression.

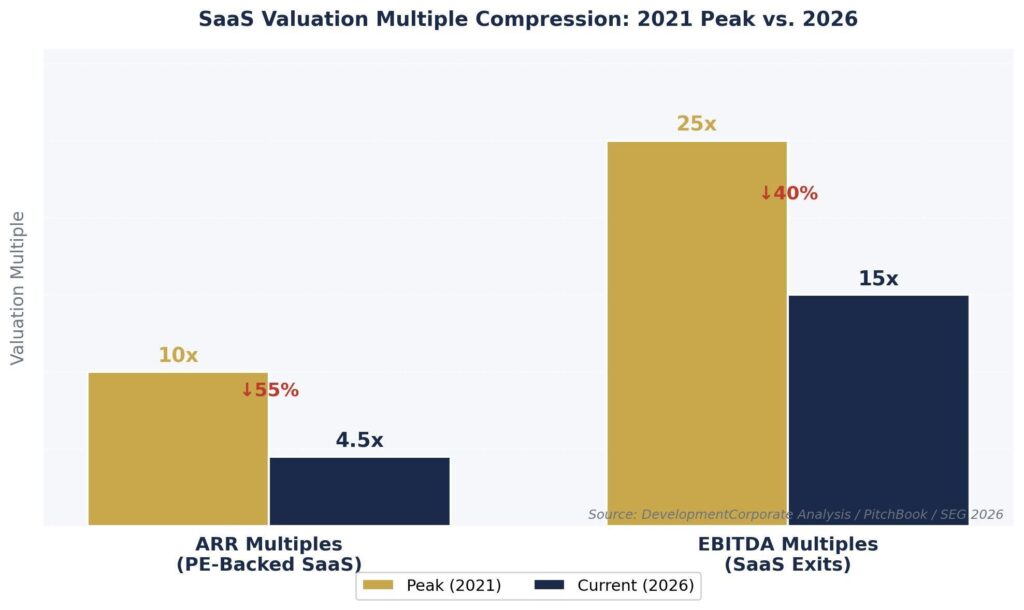

Figure 3: SaaS valuation multiples have compressed 55% (ARR) and 40% (EBITDA) from their 2021 peaks. Source: DevelopmentCorporate / PitchBook / SEG 2026.

Not All Software Is Equally Vulnerable

Both credit markets and equity buyers are making one critical distinction that most SaaS founders miss: not all software is equally at risk from AI disruption. As Thoma Bravo’s Orlando Bravo noted at Davos, AI will disrupt a percentage of software companies — “less than half” by his estimate — particularly those whose core competency is technical rather than domain-specific.

The credit market is already pricing this distinction. Software companies with deep workflow integration, proprietary data moats, and high switching costs are still findable for financing and M&A. Software companies with generic functionality that AI can replicate cheaply are not. As we’ve described in our analysis of when AI broke PE’s crystal ball, the bifurcation between AI-defensible and AI-exposed SaaS is the defining analytical challenge of the current M&A cycle.

What This Means for Founders, PE Sponsors, and Acquirers

| 🏦 FOR PE/VC INVESTORS |

| The ARR lending collapse invalidates acquisition models built on 2021-era assumptions. Specifically: |

| ▶ Rebase EBITDA projections on lender-grade metrics. If your portfolio company cannot pass a private credit underwriting test — generating $100M+ in cash operating profit — your exit multiple will reflect that weakness. Sponsored transactions now face 100+ bps higher spread than commitments made 6–12 months ago. |

| ▶ Audit pro forma EBITDA add-backs. Lenders are rejecting adjustments averaging 20–30% of stated EBITDA. Buyers will follow. Any CIM that relies heavily on run-rate adjustments from price increases, planned headcount cuts, or signed-but-not-yet-ramped contracts is a negotiating liability. |

| ▶ Treat back-leverage exposure as a valuation risk, not just a financing mechanic. PE firms that levered software portfolios at 7x+ against ARR covenants now face a double compression: loan collateral erosion plus equity multiple decline. Motivated exit timelines will create M&A opportunities — but also valuation pressure for sponsors on the sell side. |

| 🚀 FOR SAAS FOUNDERS APPROACHING AN EXIT |

| The standard exit playbook — hit $20M ARR, receive PE offers — no longer works. Three adjustments matter now: |

| ▶ Shift your exit narrative from ARR to EBITDA. Buyers and their lenders need to see real profitability. Exits are happening at 15x EBITDA versus 25x at the peak — but that math only works if you have EBITDA to sell against. Our SaaS Exit Crisis guide walks through the operational levers available. |

| ▶ Build an AI-defensibility story before you hire an investment banker. The question every buyer’s diligence team will ask is: “Where does this company sit relative to AI disruption risk?” If you cannot answer that with specifics — proprietary data, switching cost evidence, NRR data — you are negotiating from a weak position. |

| ▶ Do not wait for 2021 conditions to return. The credit market just told you they are not coming back. The structural repricing of ARR as collateral is a multi-year reset, not a cyclical dip. Founders who delay exit decisions waiting for multiple expansion face the risk of financing conditions tightening further during the hold period. |

| ⚙️ FOR ENTERPRISE CTOs AND CPOs |

| The credit market’s reassessment of SaaS ARR durability translates directly into procurement and vendor risk management: |

| ▶ PE-backed SaaS vendors facing loan covenant pressure are more likely to pursue motivated exits — meaning your critical enterprise software vendors may change ownership. Build succession scenarios for key tools with high PE sponsor ownership. |

| ▶ Use the credit market’s diligence framework as a vendor evaluation proxy. If a private credit lender would refuse to underwrite against a vendor’s ARR — because its functionality is generic, AI-replicable, or technically undifferentiated — ask whether that vendor deserves a long-term enterprise contract. |

| ▶ Treat EBITDA discipline as a vendor health signal. A SaaS vendor that cannot demonstrate path to real profitability is also a vendor that may struggle to fund the R&D needed to stay competitive against AI-native alternatives. Vendor financial health belongs in your software portfolio review. |

The New Diligence Standard: What Lenders Are Teaching Buyers

The most underappreciated aspect of the ARR lending collapse is what it reveals about the quality of diligence that the private credit market is now demanding — and that the M&A market will need to match. Our M&A Due Diligence Checklist covers the baseline, but the credit market’s current behavior points to three additional dimensions that are becoming non-negotiable.

1. Revenue Durability Stress Testing

Lenders are no longer accepting ARR at face value. They want evidence that the revenue will survive an AI disruption scenario — that customers are not in the early stages of evaluating AI-native alternatives, that churn rates have not started to move, and that NRR is not being supported by price increases on a shrinking base. Buyers should apply the same stress test.

2. EBITDA Adjustment Scrutiny

The days of 25–30% EBITDA add-backs sailing through underwriting unchallenged are over. Every planned cost reduction, revenue ramp, and synergy assumption is now being pressure-tested against execution evidence. Deal teams that cannot substantiate their adjustments with signed contracts, HR documentation, or operational milestones will face significant negotiating haircuts.

3. AI Moat Assessment

The credit market’s floor of $100M cash operating profit is a proxy for a business with sufficient scale and differentiation to survive AI disruption. For companies below that threshold, the question that matters most — in both credit and M&A — is whether the product has a durable moat against AI replication.

This includes assessing AI training data provenance, GEO visibility and LLM citation footprint, and the target’s position on the differentiation ladder — from commoditized workflow tools at the top (highest AI disruption risk) to deeply integrated, proprietary-data-advantaged platforms at the bottom (defensible).

Conclusion: The Credit Market Has Already Answered the Valuation Question

Private credit lenders have spent 18 months asking a question that the SaaS industry has been reluctant to answer honestly: is ARR still a reliable indicator of durable cash flow? Their answer, delivered through zero ARR loans at Lincoln International and 756 basis points of bid decline on software loans, is unambiguous. It is not.

The M&A market is working through the same question. The transition from ARR-based to EBITDA-based underwriting in credit is a preview of the transition from ARR multiples to EBITDA multiples in equity. Founders who have not yet updated their exit models, sponsors who have not stress-tested their portfolio EBITDA against lender-grade scrutiny, and acquirers who have not built AI-disruption risk into their valuation frameworks are all operating on outdated assumptions.

The private credit market’s message is clear: revenue is not enough. Earnings matter. Durability matters. And AI risk is now priced into every software deal — whether the seller is ready for that conversation or not.Contact DevelopmentCorporate to discuss how the private credit market’s evolving underwriting standards should inform your SaaS exit strategy, acquisition diligence framework, or portfolio positioning in 2026.