AI Startup ARR Manipulation: How Rage-Bait Culture Normalized Lying About Revenue

AI startup ARR manipulation is no longer just a cautionary tale from the fraud playbooks of the past. It just played out in public, in real time, and the market barely flinched. When Cluely CEO Roy Lee admitted on March 5, 2026, that he had lied about reaching $7 million in annual recurring revenue to TechCrunch, the reaction was mostly a shrug — and that reaction tells us something far more troubling than the lie itself.

This isn’t a story about one dishonest founder. It’s a story about a culture that made the lie not only rational but almost predictable. And Cluely is not alone. Two other high-profile cases — one a 2025 a16z-backed scandal, one a federal criminal conviction — show exactly where this culture leads, and why SaaS founders need to understand the full spectrum.

The Cluely Confession: What the Numbers Actually Showed

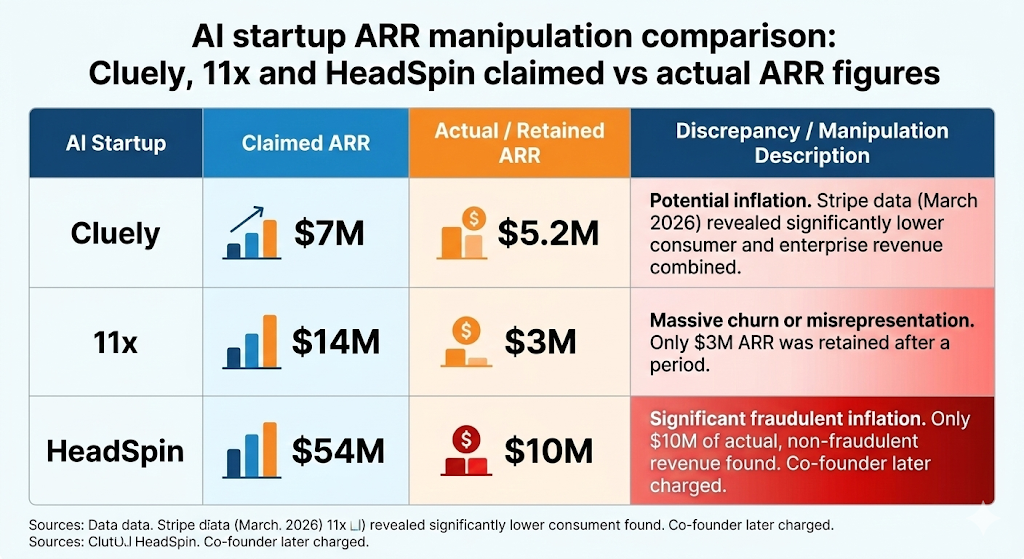

In the summer of 2025, TechCrunch reported that Cluely had reached $7M ARR — a figure Lee shared directly in an interview arranged by his own PR team. In the admission posted on X in early March 2026, Lee revealed the actual picture: consumer ARR of $2.7M (with a run rate of $3.8M) and enterprise ARR of $2.5M (run rate of $2.5M), totaling roughly $5.2M in actual ARR at the time.

That’s not a rounding error. It’s a $1.8M gap — approximately 35% inflation on a headline metric that investors, press, and potential customers use as a primary indicator of business health. And in the same post where Lee admitted the lie, he also misrepresented the circumstances under which he gave the interview, claiming it was a cold call rather than an interview his own PR representative had proactively arranged.

Two lies in one correction. The math on the honesty wasn’t great either.

To be clear: Cluely was not failing. The actual numbers — $5.2M in combined ARR — represent a legitimately fast-growing AI startup that had already raised a $15 million Series A from Andreessen Horowitz in June 2025, following a $5.3M seed round from Abstract Ventures and Susa Ventures. The company didn’t need the lie. It chose the lie. That distinction is the whole story.

Rage-Bait Marketing: When Virality Becomes Your Business Model

Cluely’s origin story is inseparable from its marketing strategy. Roy Lee was suspended from Columbia University after building a tool to help software engineers cheat on job interviews without being detected. Rather than treating this as a setback, he published it. The post went viral. The controversy became the product. The outrage became the acquisition funnel.

The company raised $5.3M on the strength of that attention. It launched a counter-industry — rivals emerged specifically to detect Cluely usage, which generated more press for Cluely. Lee spoke openly about this playbook at TechCrunch Disrupt 2025, describing how rage-bait marketing had driven early customer acquisition.

The strategic logic is not stupid. In a market flooded with AI tools, manufacturing moral controversy costs less than paid acquisition and converts faster than brand advertising. The problem is not the tactic in isolation. The problem is what the tactic does to a founder’s relationship with truth over time.

When your business model is the story, metrics become story elements. ARR stops being a financial measurement and starts being a narrative beat. The pressure to keep the story escalating — more users, more revenue, more controversy — creates systematic incentives to stretch every number just a little further than reality supports.

AI Startup ARR Manipulation Is a Culture Problem, Not a Character Problem

Cluely is not a unique case. It is a visible case. AI startup ARR manipulation exists on a spectrum that ranges from aggressive interpretation of revenue recognition rules all the way to outright fabrication. Most of the cases that matter to founders sit somewhere in the middle — in the grey zone where numbers are technically defensible but strategically misleading.

Consider the most common patterns:

- Run rate inflation: Taking a single strong week or month and annualizing it as ARR. Lee’s own Stripe data showed this — consumer ARR of $2.7M versus a run rate of $3.8M, a gap that suggests he may have reported the aspirational run rate figure rather than actual contracted recurring revenue.

- Trial-period counting: Including short-term pilot contracts in full-year ARR calculations, even when those contracts include opt-out clauses after 90 days — before any long-term commitment has been made.

- Phantom customer logos: Listing trial participants or lapsed accounts as active customers on marketing materials, inflating apparent scale and credibility.

- Gross vs. net confusion: Reporting gross revenue on marketplace or reseller models without disclosing the take rate, creating the impression of a larger business.

- ARR from non-recurring sources: Including one-time implementation fees, consulting revenue, or variable usage billing in ARR figures that imply predictable subscription economics.

None of these require a deliberate decision to deceive. They emerge from the same culture that produces rage-bait marketing: the belief that the story must always accelerate, that hesitation looks like weakness, and that the market will forgive you if the product eventually catches up to the pitch.

It often does forgive — which is exactly why the behavior persists. But two other cases show where this logic leads when left unchecked: one ended in investor lawsuits, the other in an 18-month federal prison sentence.

Case Study #1: 11x.ai — When Trial Periods Became “ARR”

In March 2025, TechCrunch reported that 11x, an AI-powered sales automation startup founded in 2022 by Hasan Sukkar, had been systematically inflating its ARR through a structurally misleading contract design. In just two years, 11x claimed to approach $10 million in ARR — enough to attract a $24 million Series A from Benchmark followed by a $50 million Series B led by Andreessen Horowitz, valuing the company at $350 million post-money.

The mechanism was buried in contract structure. 11x sold one-year contracts that included a “break clause” — a 90-day opt-out that functioned as a trial period. When calculating ARR, the company counted the full annual contract value for every customer, including those who had already exercised the break clause and stopped paying. According to former employees cited by TechCrunch, only approximately $3 million in contracts had survived past the trial threshold out of a reported $14 million in ARR — a gap of roughly 78%.

“They absolutely massaged the numbers internally when it came to growth and churn,” one former employee told TechCrunch. The company also listed logos of companies including ZoomInfo and Airtable as customers on its website — despite ZoomInfo publicly stating it had never been a customer and was pursuing legal action for unauthorized use of its trademark.

11x defended its approach as using “contracted ARR (CARR),” claiming investors were aware of the metric definition. That defense only underscores the definitional grey zone at the heart of AI startup ARR manipulation. As one VC told Fortune, “The problem is that so much of this is essentially vibe revenue. It’s not Google signing a data center contract. That’s real shit. Some startup that’s using your product temporarily? That’s really not revenue.”

The 11x case shows the mechanism that sits one step beyond Cluely’s public lie: not a headline number delivered to press, but a systematic contract structure that converted trial interest into the appearance of committed recurring revenue — and then raised institutional capital at approximately 35x that inflated figure.

Case Study #2: HeadSpin — Where ARR Manipulation Ends in Federal Court

If 11x represents the grey zone and Cluely represents the public confession, HeadSpin represents the far end of the spectrum — the point where AI startup ARR manipulation transitions from aggressive accounting to criminal fraud.

HeadSpin was a mobile application testing platform founded in 2015 by Manish Lachwani, a former Google executive. By 2020, HeadSpin had raised more than $100 million across multiple funding rounds and achieved a valuation of $1.1 billion — unicorn status — based largely on ARR figures Lachwani had personally constructed. In 2019, he told investors HeadSpin had ARR of $54 million. The board later determined the actual figure was roughly $10 million.

According to his guilty plea filed with the U.S. Department of Justice, Lachwani’s methods included counting revenue from potential customers who had never agreed to pay, inflating amounts beyond what real customers had contracted, and continuing to count revenue from customers who had already churned. He maintained a private ARR spreadsheet — controlled solely by him — containing fabricated figures he shared with investors. He also altered invoices before sending them to HeadSpin’s accountant to manufacture the appearance of contracted revenue.

In April 2023, Lachwani pleaded guilty to two counts of wire fraud and one count of securities fraud. In April 2024, he was sentenced to 18 months in federal prison and ordered to pay a $1 million fine. At sentencing, U.S. Attorney Ismail Ramsey stated: “Today’s sentencing should send a message to other entrepreneurs who may be tempted to cross the line into fraud and to ‘fake it until they make it.'”

HeadSpin’s case illustrates the end state of a logic that begins, as Cluely’s did, with the belief that the story can run ahead of the numbers. The founder who inflates ARR for a TechCrunch interview and the founder who fabricates invoices for a Series C data room are not different in kind. They are different in degree, on the same continuum.

The Structural Risk SaaS Founders Are Underestimating

Ironically, Lee himself identified the core problem before his own admission caught up with him. At Disrupt in October 2025, he told the audience: “What I’ve learned is you should never share revenue numbers.” He was right. But the lesson he drew was the wrong one.

The lesson isn’t to stop sharing revenue numbers. The lesson is to stop treating revenue numbers as marketing assets in the first place. When you weaponize metrics for attention, you create a trap with no clean exit. You either keep inflating to maintain narrative momentum, or you admit the gap and absorb the credibility cost. There is no scenario where this ends well.

For SaaS founders, the structural risks compound across three dimensions:

Due Diligence Exposure

If you have raised capital on the basis of misrepresented metrics, you carry potential liability regardless of whether investors have pursued it. M&A due diligence routinely surfaces discrepancies between publicly stated ARR and actual billing system data. The delta between story and reality is always discovered — the only question is when and by whom. As HeadSpin demonstrates, “by whom” can include the FBI.

Valuation Anchoring

Artificially inflated ARR creates valuation expectations that your real financials cannot support. At standard SaaS multiples, a $1.8M ARR gap translates to a $9–18M valuation discrepancy depending on growth rate and sector. An 11x-sized gap — $11M of phantom ARR — can mean more than $100M in evaporated enterprise value in a future round or exit process.

Team and Culture Distortion

Your team reads your public statements. When leadership demonstrates that metrics are negotiable, it establishes a cultural permission structure where the same logic migrates into sales forecasting, customer success reporting, and pipeline management. The founder who inflates ARR to journalists is building a company where salespeople inflate close probability to managers.

What SaaS Founders Should Do Instead

The choice is not between inflated metrics and boring anonymity. There is a third path — one that uses real operational transparency as a differentiated competitive signal, particularly in an environment where sophisticated audiences are increasingly capable of detecting AI startup ARR manipulation.

Define Your Metrics Publicly and Precisely

Don’t just report ARR — define what you mean by it. Stating that ARR reflects only contracted, recurring annual commitments with no run-rate extrapolation is itself a credibility signal. It tells sophisticated readers that you understand the difference and have nothing to hide. Companies that do this consistently tend to build deeper trust with both customers and investors than those optimizing for headline numbers. Read our analysis of AI productivity claims for a framework on where the line sits between evidence and marketing.

Separate Marketing Velocity from Financial Reporting

You can build a viral brand without using financial metrics as the instrument of virality. Product demonstrations, user stories, roadmap transparency, and technical architecture posts generate attention without creating a liability when the numbers need to be verified.

Treat Every Public Metric as a Future Due Diligence Item

Every ARR number you state publicly will be cross-referenced against your actual billing data in any serious M&A process or institutional fundraise. The question to ask before sharing any metric is not ‘will this generate attention?’ but ‘will I be able to defend this number in a data room three years from now?’ If the answer is no, the number should not be shared.

Build Credibility as a Moat

In a market saturated with AI startups making extraordinary claims, verifiable honesty is a genuine competitive differentiator. The founders who build reputations for precision — who are known for understating rather than overstating — command higher trust from enterprise buyers, better terms from investors, and premium valuations in exit processes. The short-term attention cost of not inflating your numbers is real. The long-term credibility premium is larger.

The Real Lesson from Cluely, 11x, and HeadSpin

These three cases represent three points on the same line: a startup founder who lied to a journalist, a startup that built its ARR narrative into its contract structure, and a founder who went to federal prison. The distance between them is not a difference in values — it is a difference in scale, time, and the point at which institutional scrutiny arrived.

AI startup ARR manipulation isn’t primarily a legal or ethical problem — though it becomes both at scale. It is first and foremost a strategic error that emerges when founders lose the distinction between the story they are telling and the business they are building.

Rage-bait marketing is a powerful tool for generating early attention in a crowded market. But attention is not a business. Revenue is a business. And revenue only becomes the foundation of a durable enterprise when it is measured honestly, reported precisely, and grown systematically — separate from the story, not subordinate to it.

The founders who understand this distinction early are the ones who reach exit with their credibility — and their valuation — intact. Are you preparing for a fundraise or M&A process? DevelopmentCorporate helps enterprise SaaS founders align their financial narrative with verified data before entering any capital markets process. Schedule a confidential consultation.

One Comment

Comments are closed.