Why Product Managers Need to be Able to Read 10-K Filings

One of the key themes I have reinforced over my 25-year career in product management is basic financial literacy. Product managers need to be able to locate, read, and interpret basic financial filings like Annual Reports (10-Ks), quarterly filings (10-Qs), and Proxy Statements (Def 14As). It should be a tool like others in their product management toolbox. There is a ton of information in public filings that customers and competitors must disclose. This information can make or break a sales deal, competitive steal away campaign, or even a product roadmap.

Pragmatic Example

Here’s a simple case in point. A company I worked for had a long-standing relationship with a customer where they provided a value-added outsourced solution that generated over $1.5 million/year in revenues. After a change in management, the customer decided to re-examine their investment in the outsourced solution. A new executive wanted to bring the solution in-house. To do so, this company would need to invest over $750,000 in equipment and software, plus set up a group of employees to do the processing/value-added services t we had been doing. If they brought the solution in-house they believed they could save $500K a year.

The salesperson on this deal was petrified that the customer was going to take the solution in-house. As a result, he thought of offering to cut the monthly fees by 50% so that the customer would not even consider taking the solution in-house. This company had a history of ‘writing down’ existing business in a bid to preserve revenue. The salesperson was commissioned on revenue, so some revenue was better than no revenue.

Fortunately, a product manager on the deal pricing committee did a little research. Even though it was a large company with more than $200 million in revenues, it had some serious financial challenges. At the time they were ‘considering’ in-sourcing the solution the company only had $5 million in cash on their balance sheet and a limited revolving credit facility. The product manager learned this fact by reviewing the customer’s 10-Qs and 10-Ks. The customer also had certain minimum EBITDA and cash flow targets they had to meet to be in compliance with the covenants of their loan agreements.

Once the sales team realized that the company would have to invest about 20% of their existing cash balance to make the project work, they came to the conclusion that they were not serious about in-sourcing. Instead, they were really looking to get a massive price reduction. Armed with this knowledge they were able to structure a win-win deal for all parties that did not result in a 50% revenue reduction. In this case, the product manager was able to save the company hundreds of thousands of dollars in lost revenue.

What is a 10-K?

A10-K is an annual report required by the U.S. Securities and Exchange Commission (SEC). It gives a comprehensive summary of a company’s financial performance. The 10-K includes information such as company history, organizational structure, executive compensation, equity, subsidiaries, and audited financial statements, among other information.

You can find 10-Ks at the SEC’s EDGAR website where it maintains copies of all filings. You can search by company name or ticker symbol. You can download most financial exhibits as Excel files for free.

What Are The Components of a 10-K?

A 10-K consists of a number of standard components. We will use excerpts from Zoom and Oracle’s recent 10-K filings to show some relevant parts that would be of interest to product managers:

Fiscal Year

On the cover of a filing, the fiscal year is listed. Most company’s fiscal years run from January through December. Companies sometimes use non-calendar fiscal years to differentiate themselves from other companies. A company I worked for fiscal year ran from October 1 to September 1 to mirror the U.S. Federal government’s fiscal year.

Understanding customer fiscal year ends is critical. Most large purchases (>$100,000) need to be budgeted. Annual budgets are usually developed in the third fiscal quarter, finalized in the fourth quarter, and ‘released’ in the first quarter. Trying to pitch an unplanned major purchase in the third or fourth quarter can be tough. You should be aware of any budgetary roadblocks that could slow down the purchase process.

When studying competitors, understanding their fiscal year is also important. Typically, most financial plans have revenue plans that are ‘backloaded’ – in other words, the fourth quarter tends to be the largest of all quarters. Salespeople will bust their backs to exceed quota and get into the accelerator portion of the compensation plans. They will tend to offer higher discounts or better pricing late in the fiscal year to maximize their compensation.

Business Overview

This section is basically the start of their corporate messaging platform. It is how they simply explain their business. For example, here is Zoom’s business overview from their most recent 10-K:

Our mission is to make video communications frictionless and secure.

We provide a video-first unified communications platform that delivers happiness and fundamentally changes how people interact. We connect people through frictionless and secure video, phone, chat, and content sharing and enable face-to-face video experiences for thousands of people in a single meeting across disparate devices and locations. Our cloud-native platform delivers reliable, high-quality video and voice that is easy to use, manage, and deploy; provides an attractive return on investment; is scalable and easily integrates with physical spaces and applications. We believe that rich and reliable communications lead to interactions that build greater empathy and trust. We strive to live up to the trust our customers place in us by delivering a communications solution that “just works.”

The cornerstone of our platform is Zoom Meetings, around which we provide a full suite of products and features designed to give users an easy, reliable, and innovative unified communications experience. Users are comprised of both hosts who organize video meetings and the individual attendees who participate in those video meetings. In 2019, we launched Zoom Phone, a cloud-based PBX system, creating a unique unified communications platform. Many customers also choose to implement Zoom Rooms, our software-based conference room system, which enables users to easily experience Zoom Meetings in their physical meeting spaces. Our partner ecosystem, which includes App Marketplace and in-product apps, and developer platform help enterprises create elevated experiences with third-party applications to create customized workflows.

Zoom FY2020 10-K

Products and Services

On page 7, Zoom provides a basic description of its nine products and services.

Departmental Overviews

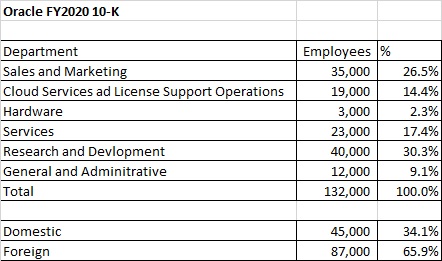

In Oracle’s FY2020 10-K they provide a breakdown of headcount by department:

Customers

Zoom disclosed they had approximately 467,100 customers with more than 10 employees.

Competition

Most companies describe who they view as their main competition. Here is how Oracle describes their competition:

We face intense competition in all aspects of our business. The nature of the IT industry creates a competitive landscape that is constantly evolving as firms emerge, expand or are acquired, as technology evolves and as customer demands and competitive pressures otherwise change.

Our customers are demanding less complexity and lower total cost in the implementation, sourcing, integration and ongoing maintenance of their IT environments. Our enterprise cloud, license and hardware offerings compete directly with certain offerings from some of the largest and most competitive companies in the world, including Amazon.com, Inc., Microsoft Corporation, International Business Machines Corporation (IBM), Intel Corporation, Cisco Systems, Inc., Adobe Systems Incorporated, Alphabet Inc. and SAP SE, as well as other companies like Hewlett-Packard Enterprise, salesforce.com, inc. and Workday, Inc. In addition, due to the low barriers to entry in many of our market segments, new technologies and new and growing competitors frequently emerge to challenge our offerings. Our competitors range from companies offering broad IT solutions across many of our lines of business to vendors providing point solutions, or offerings focused on a specific functionality, product area or industry. In addition, as we expand into new market segments, we face increased competition as we compete with existing competitors, as well as firms that may be partners in other areas of our business and other firms with whom we have not previously competed. Moreover, we or our competitors may take certain strategic actions—including acquisitions, partnerships and joint ventures, or repositioning of product lines—which invite even greater competition in one or more product offering categories.

Oracle 10-K FY 2020, page 16

Here’s how Zoom described their competition:

The markets in which we operate are highly competitive. We face competition from legacy web-based meeting services providers, including Cisco Webex and LogMeIn GoToMeeting, and bundled productivity solution providers with video functionality, including Google G Suite and Microsoft Teams, as well as UCaaS and legacy PBX providers, including 8×8. Avaya, and RingCentral.

Zoom FY2020 10-K, page 9

Item 1A. Risk Factors

All 10-Ks contain a section that details, from the company’s perspective, risks and uncertainties that could impact their financial performance and stock price. Many of these items are Pro-forma, you will see them in most 10-Ks. You should be alert to anything that is not cited by other companies in the industry.

Item 2. Properties

The properties and locations they use for their business.

Item 3. Litigation

Litigation is common for software companies. Oracle list five major matters:

- Hewlett-Packard Company Litigation

- Derivative Litigation Concerning Oracle’s NetSuite Acquisition

- Securities Class Action and Derivative Litigation Concerning Oracle’s Cloud Business

- Derivative Litigation Concerning Oracle’s Board Composition and Hiring Practices

If the company believes that they have a significant risk of losing a lawsuit, they will establish a reserve to cover any settlement. If the suit settles with no financial impact, the company will release the reserve and provide a temporary one-time bump in profits and earnings.

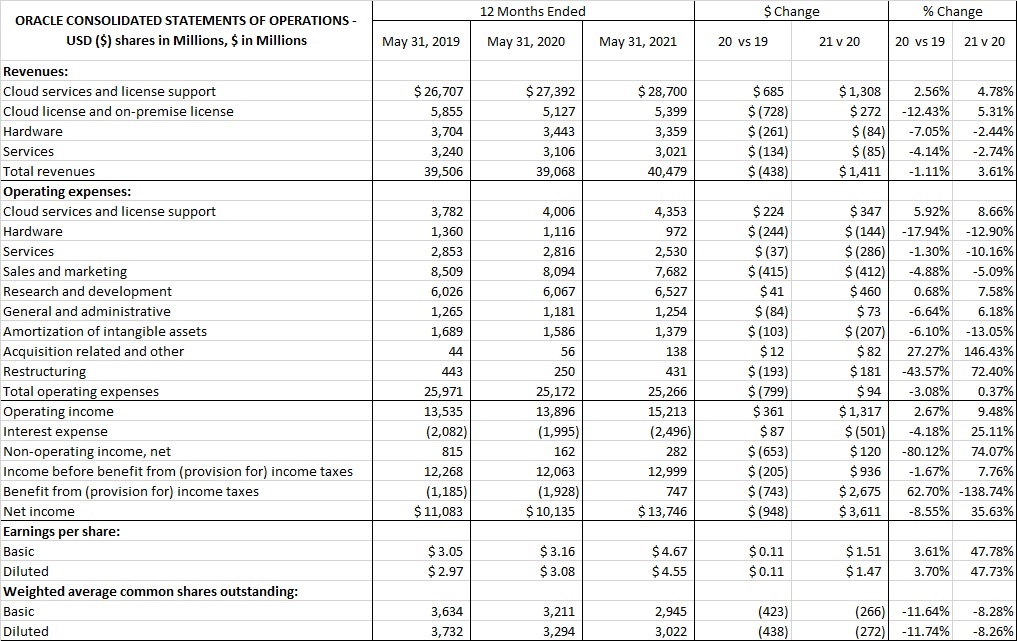

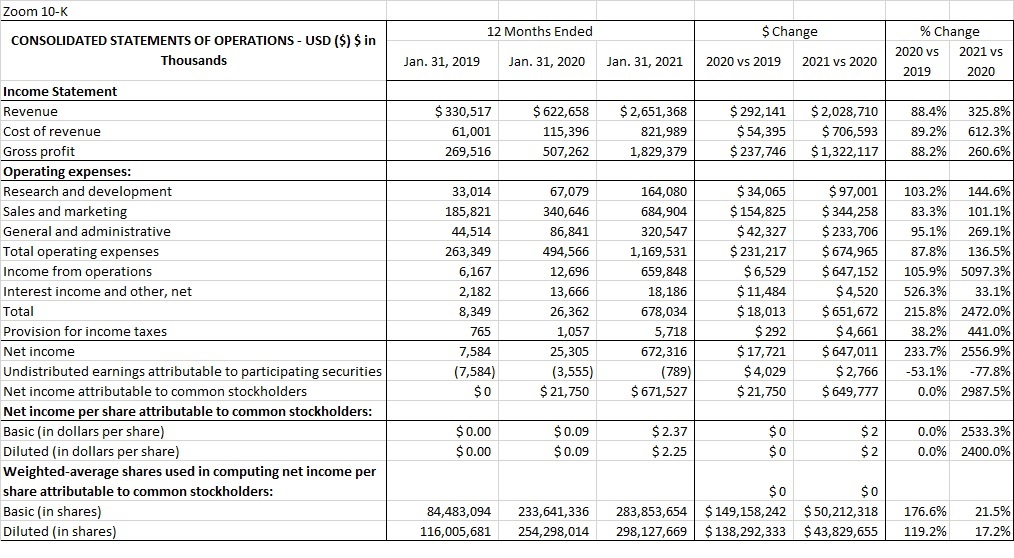

Results of Operations

Results of operations is one of the most significant sections in the 10-K. It describes overall revenue and expenses, and the commentary describes what has driven increases and decreases. To learn more about how product managers can leverage income statements check out Why Should Product Managers Care About Income Statements?

Consider Oracle and Zoom’s results:

Here is Oracle’s discussion about its hardware business:

Hardware Business

Our hardware business, which represented 8% and 9% of our total revenues in fiscal 2021 and 2020, respectively, provides a broad selection of enterprise hardware products and hardware-related software products including Oracle Engineered Systems, servers, storage, industry-specific hardware offerings, operating systems, virtualization, management and other hardware-related software, and related hardware support. Each hardware product and its related software, such as an operating system or firmware, are highly interdependent and interrelated and are accounted for as a combined performance obligation. The revenues for this combined performance obligation are generally recognized at the point in time that the hardware product and its related software are delivered to the customer and ownership is transferred to the customer. We expect to make investments in research and development to improve existing hardware products and services and to develop new hardware products and services. The majority of our hardware products are sold through indirect channels, including independent distributors and value-added resellers. Our hardware support offerings provide customers with unspecified software updates for software components that are essential to the functionality of our hardware products and associated software products such as Oracle Solaris. Our hardware support offerings can also include product repairs, maintenance services and technical support services. Hardware support contracts are entered into and renewed at the option of the customer, are generally priced as a percentage of the net hardware products fees and are generally recognized as revenues ratably as the hardware support services are delivered over the contractual terms.

Oracle 10-K FY 2020

These types of discussions provide significant insight into how a company views its business.

Report of Independent Registered Accounting Firm

10-K filings always include a report from the company’s independent auditors.Public companies are required to have an independent audit each year. This ensures that the financial statements and other management commentary are complete and accurate. They also certify that internal controls are sufficient to meet the requirements of Sarbanes Oxley.

Two things to look for in the auditor’s report. First, if the auditor issues a ‘qualified’ opinion — in other words, the auditor has issues with how the company has presented or accounted for certain financial information. Another red flag is if they find deficiencies in the company’s internal controls.

Financial Statements

10-Ks include full financial statements for the fiscal year. We have already discussed Results from Operations (aka Income Statement or Profit & Loss statement), let’s move on to two other statements – the Balance Sheet and Cash Flow Statement.

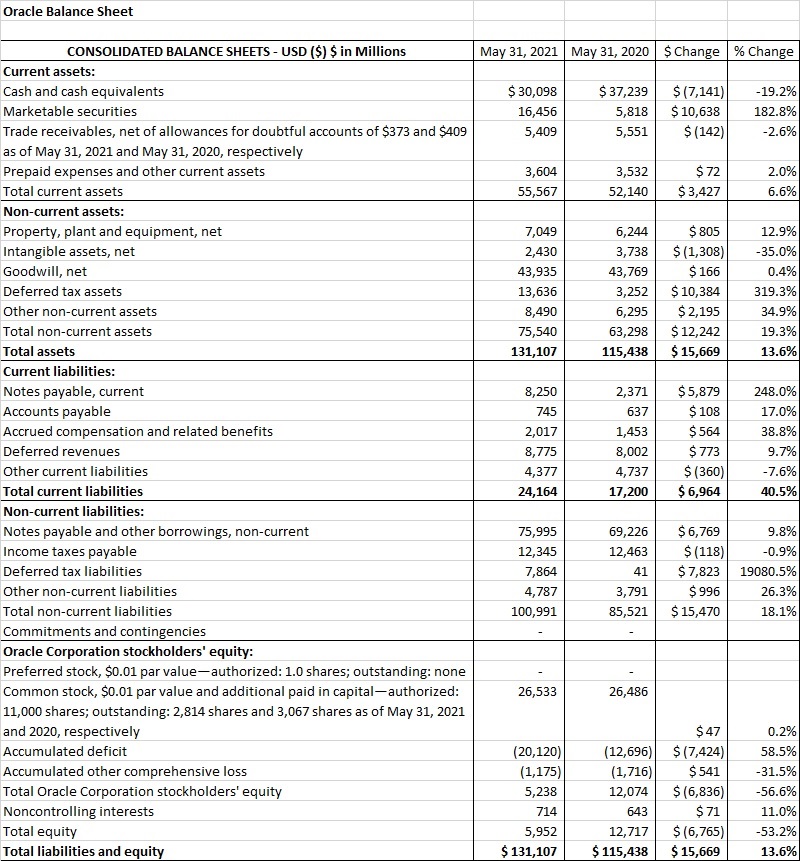

Balance Sheet

Balance sheets describe a company’s assets, liabilities, and stockholder equity on a specific date. Balance sheets contain many interesting facts. They help product managers do a better job of understanding customers, competitors, and even their own company. To learn more about Balance Sheets check out Why Should Product Managers Care About Balance Sheets?

Here is Zoom’s most recent balance sheet:

Here is Oracle’s:

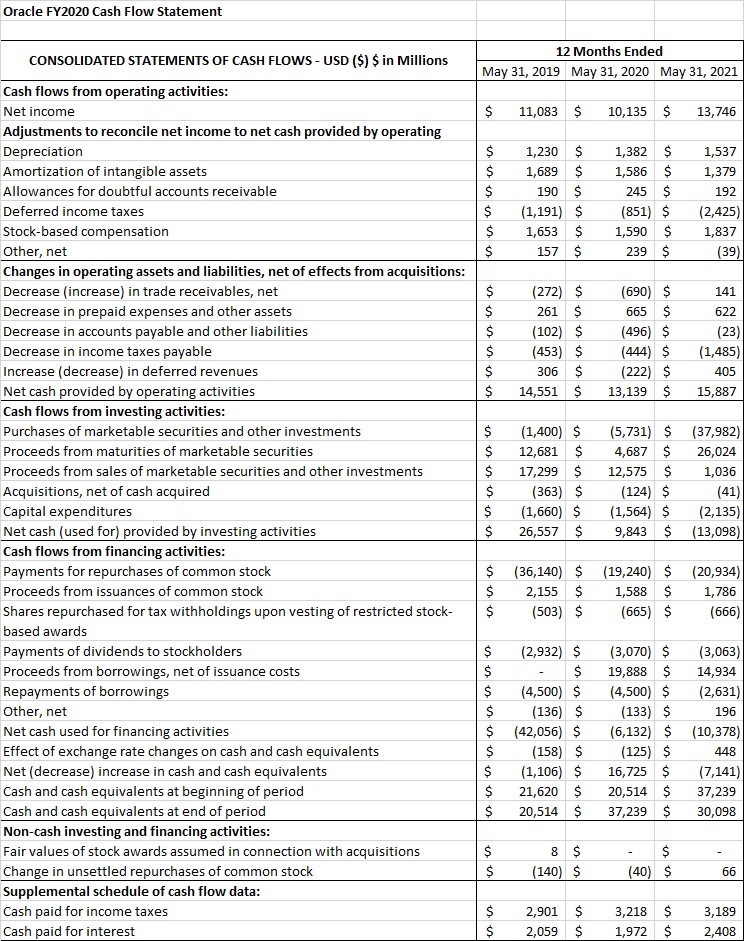

Cash Flow Statement

Cash Flow Statements can be the most useful financial statement for a product manager. They strip away the complexity of accrual-based accounting. They show how cash moves into and out of a business. A Cash Flow Statement summarizes the amount of cash and cash equivalents entering and leaving a business. It has three major components:

- Cash from operating activities

- Cash from investing activities

- Cash from financing activities

For more information check out Why Product Managers Should Care About Cash Flow Statements.

Here is Oracle’s most Recent Cash Flow Statement:

Business Combinations

High-level details about any mergers/acquisitions are included in 10-K filings. Here is an extract from Zoom’s 10-K:

5. Business Combinations

On May 7, 2020, we acquired 100% of the issued and outstanding share capital of Keybase, Inc. (“Keybase”), a secure messaging and file-sharing company, for purchase consideration of $42.9 million in cash. The acquisition helps us strengthen the security of our video communications platform by providing end-to-end encryption expertise. The acquisition has been accounted for as a business combination.

In allocating the purchase consideration, $24.3 million was attributed to goodwill, $3.3 million to intangible assets, and $15.3 million to other net assets acquired primarily consisting of cash and cash equivalents of $16.4 million. The goodwill amount represents synergies related to our existing products expected to be realized from the acquisition and assembled workforce. The associated goodwill is not deductible for tax purposes. Acquired intangible assets consisted of developed technology with an estimated useful life of five years. The developed technology had a remaining useful life of 4.3 years as of January 31, 2021, and is amortized using the straight-line method over its estimated useful life.

Not included in the purchase consideration, we also entered into holdback agreements with certain employees for $20.0 million in cash payments, which are subject to such employees’ continued service with us. The holdback amount of $20.0 million will be treated as compensation for research and development over the required service period ranging from one to three years.

Transaction costs incurred in connection with the acquisition were immaterial. The results of operations of Keybase have been included in our consolidated financial statements from the date of the acquisition. Pro forma and historical results of operations of Keybase have not been presented, as the results do not have a material effect on any of the periods presented in our consolidated statements of operations.

Zoom FY2020 10-K

Why Should Product Managers Care About 10-Ks?

As we have discussed there is a ton of information in 10-Ks that product managers can use. They provide great insights into customer businesses. You can leverage this information to make better cases for investment decisions. 10-Ks provide specific insights into competitors that can be used to make better fact-based prioritization decisions.

There are other public filings that are interesting as well. 10-Qs are shorter versions of 10-Ks that are filed every quarter.

Annual Proxy Statements (aka Definitive Schedule 14-A) provide other information like the structure of executive compensation plans. Check out this link and see starting on page 32 how Oracle incentivizes its executives.

S-1’s are statements filed associated with IPOs. Check out Zoom’s S-1 here. S-1s are great sources of industry and market data.

All of this information is freely available. Product managers would be remiss in their duties if they did not leverage it for their company’s benefit.

One Comment

Comments are closed.