North American Startup Investment Q1 2024. A Mixed Bag of Performance, but Signs of Hope

Recently Crunchbase published an analysis of North American VC activity for Q1 2024 – North American Startup Investment Perked Up A Bit In Q1. Navigate Ventures also published a good piece that puts things into context – North American Startup Funding Weakens Further In Q1.

The Depressing News

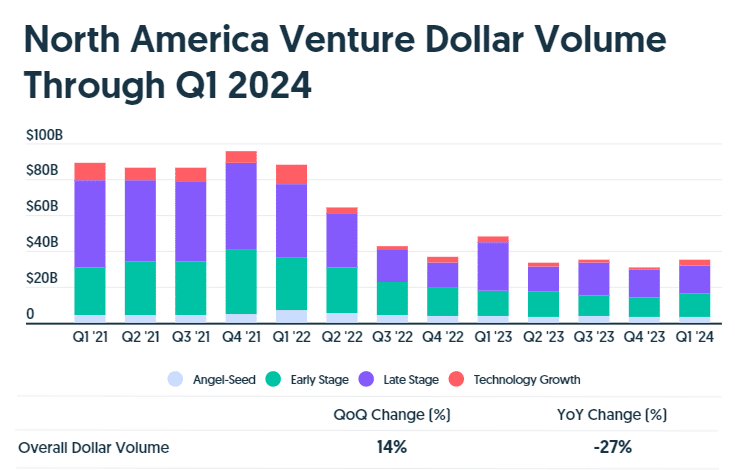

In the first quarter, VC investment in North American companies totaled $46.3 billion, marking a 46% decrease from the same period last year. This figure includes significant investments like Microsoft’s $10 billion in OpenAI and a $6.5 billion funding round for Stripe. Excluding these two major transactions, venture capital funding for the quarter would have fallen even more sharply, showing a decline of over 60% compared to the same quarter last year.

As Crunchbase reported, Q1 showed marginal QoQ growth, but continued YoY declines:

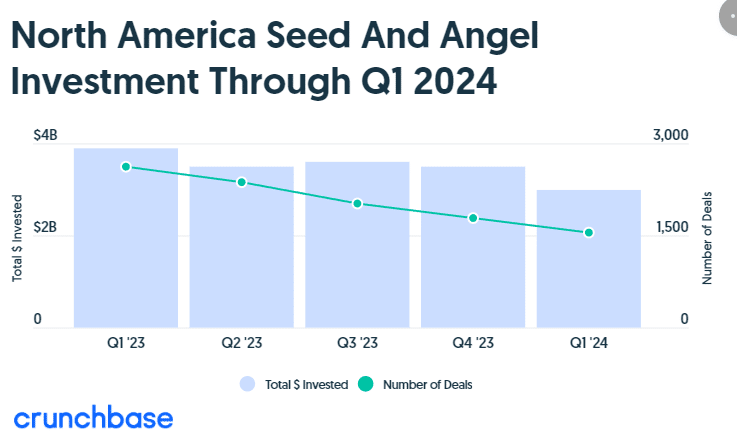

Angel & Seed Funding Decline Materially

When the VC market cooled in Q2 2022, Angel and Seed funding was somewhat immune. Early and late stage investments contracted sharply then. That contraction has now spread to Angel, PreSeed & Seed investing. Deal count and $ invested declined materially in Q1

Anecdotally, five of my clients have been trying to raise PreSeed or Seed funding in the past six months. Only one has successfully closed a round. Another is involved in a protracted round of VC due diligence.

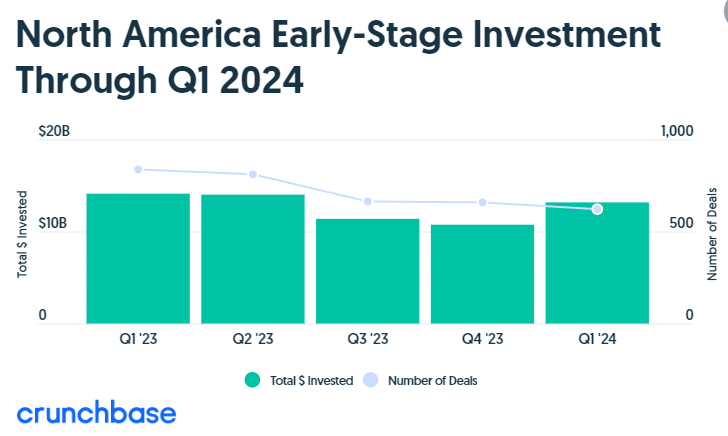

Early Stage (Series A & B) Show Signs of Recovery

Early Stage investing posted marginal sequential and year-over-year growth:

Series A & B were hit especially hard in 2023 – a 52% decline in comparison to 2022. The quarter-over-quarter and year-over-year sequential growth is a welcome sign. The majority of my clients are PreSeed or Seed stage firms. It has been hard to raise seed funding if the opportunity to raise follow on Series A rounds is constrained.

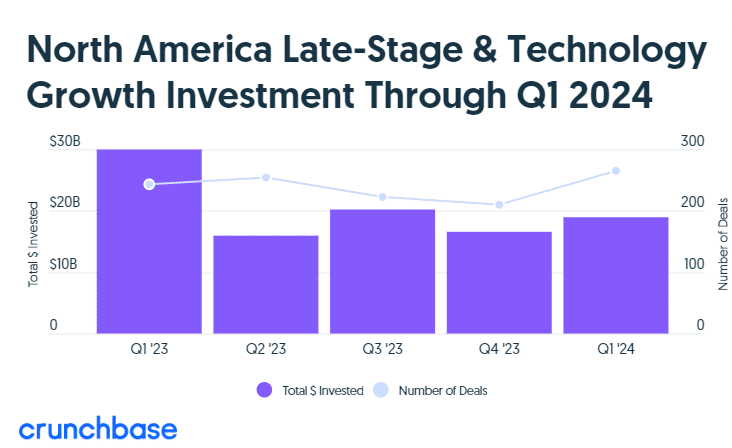

Late Stage Investing Showing Some Limited Improvement

Late-stage consists of Series C, Series D, Series E and later-lettered venture rounds. Late stage investing has typically accounted for the majority of VC dollar investments. Deal counts are somewhat lower, but dollars invested are showing sequential growth.

VC Funding Winter Maybe Ending

The doldrums of VC funding may be ending for this cycle. The slowdown that impacted Series A & B investing has caught up with Angel and Seed investing. The improvement that early and late stage investing augurs well for the 2024 recovery of Seed stage investing.

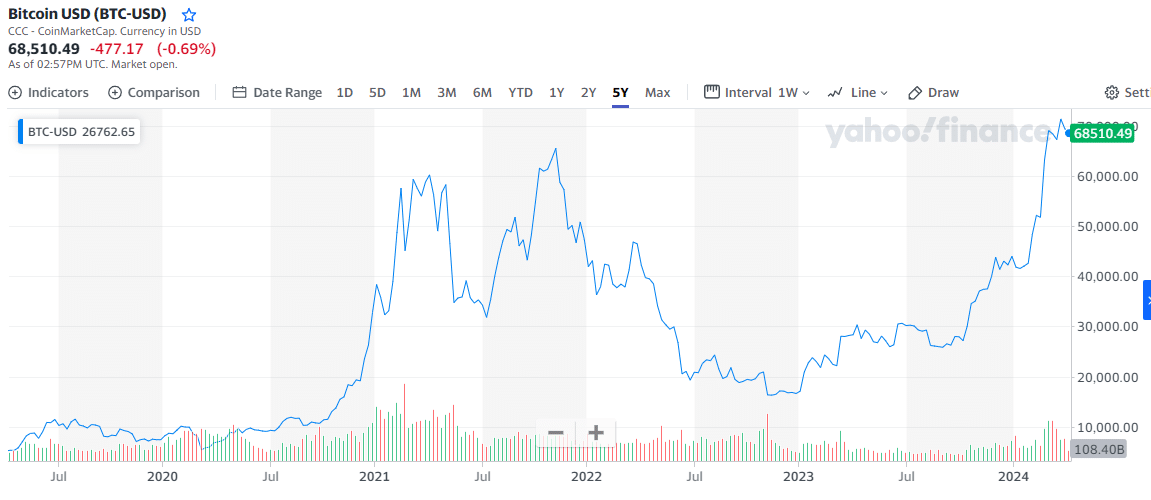

A potential canary in the coal mine is the dramatic recovery of the crypto market. While the collapse of FTX signaled the onset of the crypto winter, Bitcoin’s recent rise to an all time high may indicate that better days are ahead.

One Comment

Comments are closed.