I advise many early stage SaaS companies on many things, especially in competitive analysis. Many of them are attempting to raise either preseed or seed stage VC funding. The early stage VC funding market has experienced a significant decline since the market peak in February 2021. While most of my clients have viable products and market opportunities, fundraising has become a significant challenge. This post will present some key statistics that describe the current state of the early stage fundraising market.

Put the Market into Context

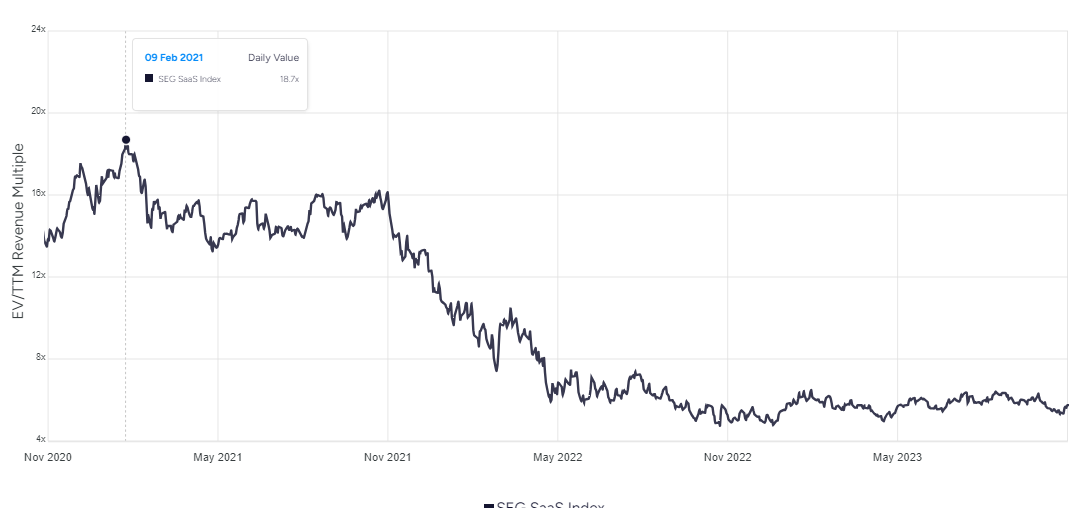

It is important to put the SaaS market into context. According to the Software Equity Group’s SaaS Index, median SaaS Enterprise Value/Revenue (ttm)valuations reached a peak of 16.x in February 2021 – almost the peak of the Covid-19 crisis. In November 2023 the median SaaS valuation had declined to 5.7x – almost two thirds of what it had been in 2021.

Software Equity Group’s SaaS Index,

Early Stage is Still Active, but Activity has Slowed

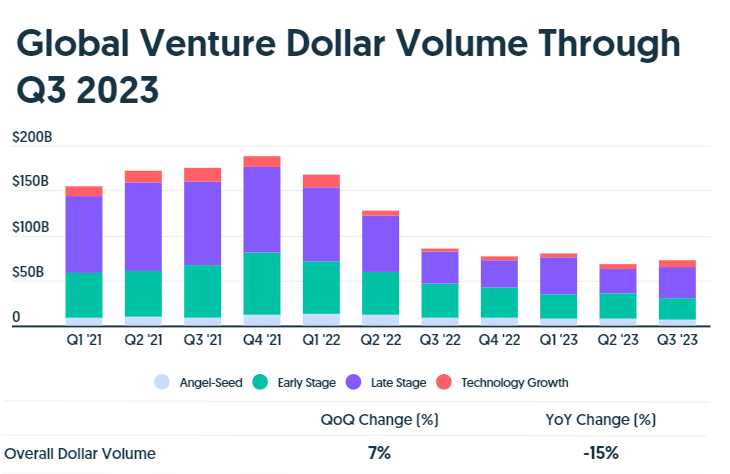

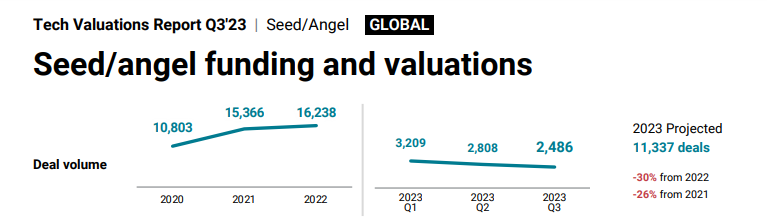

Early stage (preseed and seed) still accounts for a major portion of VC activity. According to the CB Insights Q3 2023 Tech Valuations Report:

CB Insights Q3 2023 Tech Valuations Report:

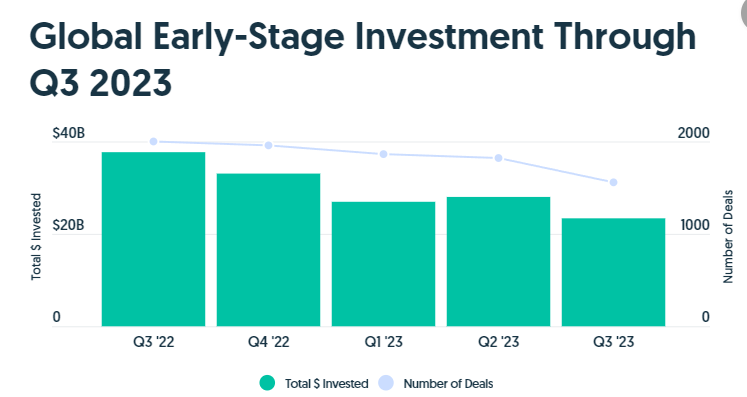

The number and value of early stage deals have declined since 2023:

CB Insights Q3 2023 Tech Valuations Report

Q3 2023 Has Shown a Slight Uptick

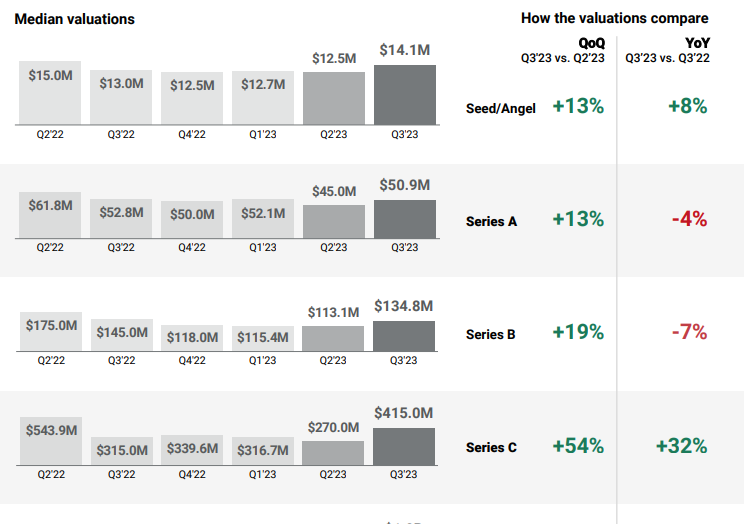

Q3 2023 has shown a slight improvement for early stage deals. Series A & B deals are still struggling, while Series C deals are recovering very nicely:

CB Insights Q3 2023 Tech Valuations Report

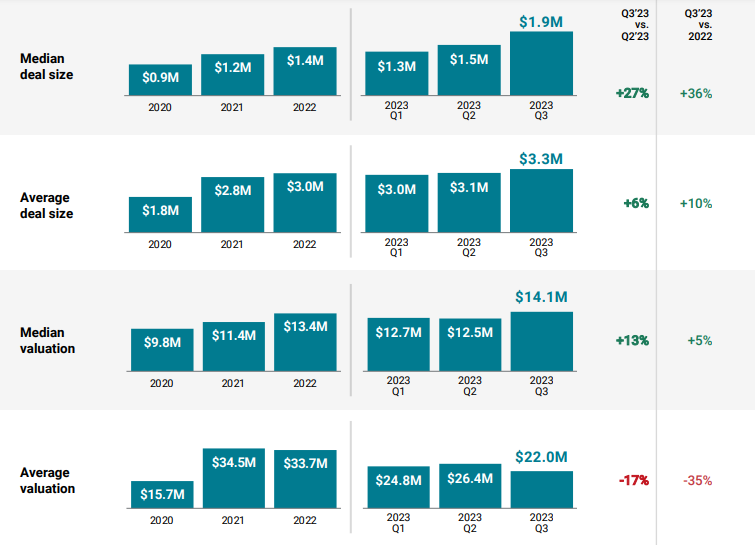

Some more insights into early stage deals:

CB Insights Q3 2023 Tech Valuations Report

Liquidation Preferences Continue to be Investor vs Founder Friendly

During the market peak of 2021, investment terms were very founder friendly. Since then the market has shifted to being investor vs founder friendly:

CB Insights Q3 2023 Tech Valuations Report

Summary

Early stage deals are still happening at a decent pace. Valuations have moderated and terms have turned more investor friendly.

Also published on Medium.