AI SaaS Investment Trends Are Flashing Red: What VC Rejection Signals Mean for M&A Buyers

AI SaaS investment trends shifted decisively in early 2026 — and the consequences for M&A valuations have not yet been fully priced into the market. Venture capital firms are now openly rejecting the majority of AI SaaS pitches they receive, not because founders lack ambition, but because the products they’re building occupy what investors are calling “dead zones”: categories where an AI agent will soon do the same job better, faster, and for a fraction of the cost.

TechCrunch recently published candid commentary from partners at 645 Ventures, F Prime Capital, AltaIR Capital, and Emergence Capital spelling out exactly what they won’t fund anymore. For M&A practitioners, this intelligence is not abstract market gossip — it’s a precise due diligence signal. When a VC says “we won’t fund that,” a buyer should hear “that category carries structural valuation risk.”

This post translates those investor rejection signals into a practical M&A framework, with specific implications for SaaS founders considering an exit, PE and VC buyers conducting due diligence, and enterprise CTOs evaluating vendor relationships.

The New VC Verdict on AI SaaS Investment Trends

The funding environment has bifurcated. Investors are not abandoning AI SaaS — they are concentrating capital in a narrow set of categories while pulling back sharply from everything else.

What Investors Still Want

Aaron Holiday, Managing Partner at 645 Ventures, identified four categories that still command real VC attention:

- AI-native infrastructure companies

- Vertical SaaS with proprietary data moats

- Systems of action — platforms that complete tasks, not just coordinate them

- Tools deeply embedded in mission-critical workflows

The common thread across all four is depth. These are businesses where switching costs are high, where proprietary assets create defensibility, and where the product sits inside the workflow rather than around it.

The Dead Zones: What VC Capital Has Left Behind

The rejection list is blunter — and longer. According to multiple investors, the following categories are now essentially unfundable:

- Thin workflow layers (lightweight coordination tools sitting on top of other software)

- Generic horizontal tools without a specific domain advantage

- Light product management and task orchestration software

- Surface-level analytics with no proprietary data

- Generic productivity tools, basic CRM clones, and project management software

- Products whose only differentiation is a polished UI over existing APIs

Igor Ryabenky, Managing Partner at AltaIR Capital, was precise about the underlying logic: “If your differentiation lives mostly in UI and automation, that’s no longer enough. The barrier to entry has dropped, which makes building a real moat much harder.”

This statement deserves to be read very carefully by any M&A buyer evaluating an AI SaaS target. It is not a preference. It is a structural diagnosis.

Why VC Rejection Signals Are a Due Diligence Goldmine for M&A Buyers

Venture capital and M&A operate on different timelines but evaluate the same fundamentals: defensibility, growth durability, and competitive moat. When VCs articulate specific rejection criteria, they are, in effect, publishing a risk taxonomy for buyers.

Here is how each major VC red flag translates into an M&A valuation risk:

Red Flag #1: Thin Moat = Structural Valuation Compression

Abdul Abdirahman of F Prime noted that generic vertical software “without proprietary data moats” no longer attracts investor interest. For buyers, this means any target whose competitive position rests primarily on brand recognition, feature breadth, or first-mover timing — rather than genuinely proprietary data or workflow integration — carries a structural discount risk as AI-native competitors enter the market.

Due Diligence Question: Can the target articulate a specific data asset or workflow lock-in that an AI-native startup building from scratch in 2026 could not replicate within 18–24 months?

Red Flag #2: Workflow Execution vs. Workflow Ownership

Jake Saper, General Partner at Emergence Capital, identified what he calls the “canary in the coal mine”: the difference between Cursor and Claude Code. “One owns the developer’s workflow, the other just executes the task,” Saper explained. “Developers are increasingly choosing execution over process.”

For M&A buyers, this is not an abstract technology debate. It defines whether the product being acquired has durable revenue or transactional revenue. Workflow-owning products create high switching costs. Task-executing products compete on price and speed — precisely the dimensions where AI commoditization hits hardest.

Products that built their moat on “workflow stickiness” — keeping humans inside their interface continuously — face a structural challenge as AI agents take over the actual work. If the users are agents rather than humans, the concept of human-workflow lock-in loses its meaning.

Due Diligence Question: Does the target own the workflow (users live inside the product) or execute within a workflow (the product is called upon to complete a task)? And what percentage of daily active use involves judgment and oversight versus rote execution?

Red Flag #3: The MCP Threat to Integration Moats

This is perhaps the most underpriced risk in current AI SaaS valuations. Saper made the point explicitly: Anthropic’s Model Context Protocol (MCP) is systematically eliminating the moat that integration-layer products have relied on for years.

“Being the connector used to be a moat,” Saper said. “Soon, it’ll be a utility.” MCP enables AI models to connect to external data and systems without requiring companies to build or download individual integrations. A product whose primary value proposition is “we connect your stack” should carry an explicit MCP risk discount in any current DCF model.

We’ve covered the broader AI infrastructure investment dynamics in detail on our enterprise SaaS M&A trends analysis, but the MCP dynamic specifically creates a new category of stranded asset risk that buyers should model explicitly.

Due Diligence Question: What percentage of the target’s stated competitive moat is attributable to integration breadth? And has the target’s leadership team modeled the valuation impact of MCP adoption at scale?

Red Flag #4: Per-Seat Pricing Under Structural Pressure

Ryabenky made a pointed observation about pricing models that carries direct implications for revenue quality analysis: “Rigid per-seat models will be harder to defend, while consumption-based models make more sense in this environment.”

Per-seat pricing is built on the assumption that human headcount drives software usage. As AI agents replace human operators of SaaS tools, that assumption deteriorates. A target still running a pure per-seat model in 2026 is carrying a revenue model risk that should factor into ARR quality assessments, retention modeling, and terminal value calculations.

This connects directly to the broader SaaS valuation compression dynamics we analyzed in our SaaS valuation benchmarks report.

Due Diligence Question: What percentage of ARR is tied to per-seat pricing? Has the target modeled what happens to that revenue if 30% of seats are replaced by AI agents over the next 24 months?

Moat Strength Reference: AI SaaS Investment Trends by Category

The table below synthesizes current VC signals into a reference framework for M&A buyers and investors evaluating AI SaaS targets:

| Moat Type | VC Appetite (2026) | M&A Valuation Risk | Defensibility |

| Workflow Ownership | High | Low | Strong |

| Proprietary Data | High | Low–Medium | Strong |

| Domain Expertise + AI | Medium–High | Medium | Moderate |

| Integration Layer | Declining | High — MCP risk | Weakening |

| UI + Automation Only | Very Low | Very High | Negligible |

| Per-Seat Pricing Model | Low | High | Weakening |

Source: TechCrunch VC investor survey, March 2026; DevelopmentCorporate M&A analysis

Three Due Diligence Frameworks for AI SaaS Buyers in 2026

The VC rejection signals above are not merely academic observations. They map directly onto practical due diligence questions that buyers should be asking at each stage of an M&A process.

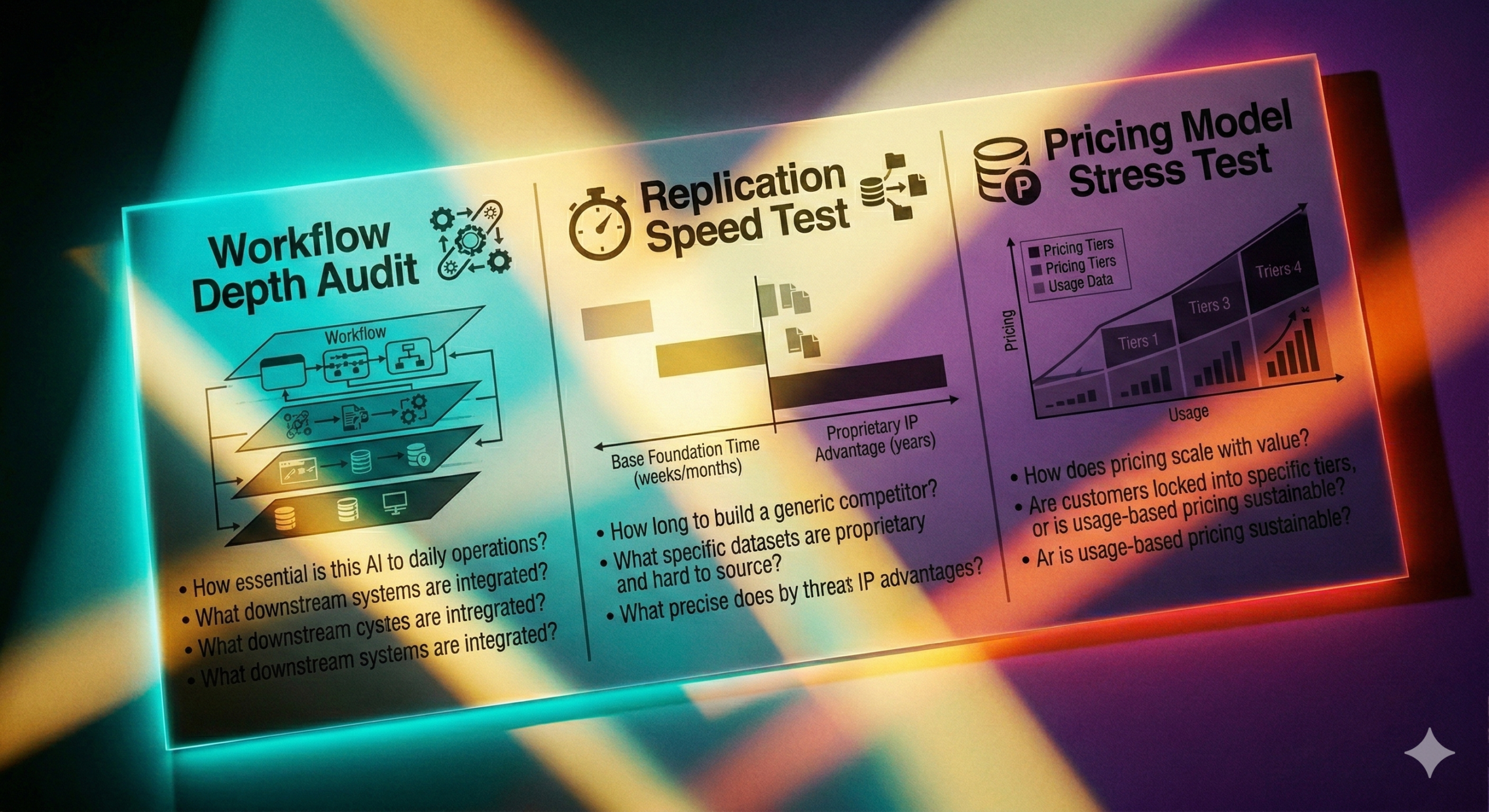

Framework 1: The Workflow Depth Audit

The central question is whether the target owns a workflow or merely participates in one. Run a structured workflow depth audit by examining:

- Daily active usage patterns — are users spending substantive time inside the product, or triggering it episodically?

- Integration topology — does the product sit at the center of the customer’s operational workflow, or at the edge?

- Data gravity — does customer data accumulate inside the product in ways that make migration costly?

- Replacement cost — how long and expensive would it be for a typical enterprise customer to replace this product?

Our SaaS due diligence checklist covers workflow depth assessment in greater detail for buyers operating at the enterprise tier.

Framework 2: The Replication Speed Test

Ryabenky at AltaIR Capital was explicit: “Strong AI-native teams can rebuild [thin products] quickly.” Buyers should ask the same question that VCs are asking: how fast could a well-funded AI-native startup replicate the core functionality of this product?

A useful forcing function is to assume a $5M seed-funded team building on the current AI infrastructure stack. If the honest answer is “they could ship a competitive MVP in 6–9 months,” the product does not have a durable moat — and the acquisition price should reflect that reality.

Framework 3: The Pricing Model Stress Test

Model a scenario in which 30% of the target’s human users are replaced by AI agents over 24 months. Specifically:

- How does ARR behave under a per-seat model in that scenario?

- Does the product have consumption-based or outcome-based pricing that could capture agent usage?

- What is management’s current roadmap for pricing model evolution?

A target with no credible answer to these questions is carrying unmodeled revenue risk. A target with a clear transition path to consumption-based pricing is demonstrating the kind of strategic adaptability that protects acquirer returns.

Strategic Implications by Audience

For SaaS Founders Evaluating an Exit

If your product sits in any of the dead zones identified by investors — thin workflow layer, UI-led differentiation, integration connector, generic horizontal tool — the window to achieve a premium exit multiple is narrowing. Buyers are applying exactly the same scrutiny as VCs, and the M&A market typically lags the VC market by 12–18 months in repricing.

The most defensible move is to use any remaining runway to deepen workflow integration and build proprietary data assets. Ryabenky’s prescription applies equally to exits as to fundraising: “Real workflow ownership and a clear understanding of the problem from day one.”

Our analysis of AI productivity paradox dynamics is relevant context for founders navigating this positioning challenge.

For PE/VC Investors Conducting Due Diligence

The VC rejection criteria above represent a rapidly evolving consensus that is not yet fully reflected in M&A pricing. This creates opportunity — not to avoid the dead zones, but to apply appropriate discounts and negotiate accordingly.

The categories that command premium valuations in 2026 are becoming narrower and more clearly defined: workflow-owning platforms with proprietary data, deep vertical expertise embedded in AI-native architecture, and consumption-based revenue models designed for an agent-driven usage pattern. Everything else requires a structural haircut.

For Enterprise CTOs and CPOs Evaluating Vendors

The same framework applies to vendor selection. An enterprise CTO evaluating an AI SaaS vendor should ask whether the vendor occupies a VC dead zone category — not because it disqualifies the vendor today, but because a vendor whose product can be replicated within 18 months by a well-funded AI-native startup is a vendor with an uncertain product roadmap.

The practical implication: procurement and contract terms for AI SaaS vendors in dead zone categories should include shorter lock-in periods, clear data portability requirements, and explicit clauses covering the pricing model transition risk.

The Bottom Line: Investor Signals Are Due Diligence Intelligence

The current AI SaaS investment trends are sending an unusually clear signal. When senior partners at leading venture firms independently converge on the same rejection criteria — thin moats, UI differentiation, integration layers, workflow coordination — they are not expressing a preference. They are identifying categories where competitive advantage is structurally eroding faster than product development cycles can respond.

For M&A buyers, these signals are a gift. The market is not yet fully pricing the structural risks in dead zone AI SaaS products. The window to apply rigorous due diligence — and negotiate valuations that reflect actual defensibility rather than AI narrative premiums — is open now.

The acquirers who discipline themselves to apply the Workflow Depth Audit, the Replication Speed Test, and the Pricing Model Stress Test to every AI SaaS target in 2026 will make better acquisitions at better prices. Those who don’t will find they’ve paid platform multiples for commodity software. Review our enterprise SaaS M&A trends analysis and our per-seat pricing model collapse analysis for further context on the valuation dynamics shaping this environment.