Cash Flow Statements are probably the hardest type of financial statement for product managers. You should understand Income Statements and Balance Sheets before you try to understand a Cash Flow Statement. Cash Flow Statements can be the most useful financial statement for a product manager. They strip away the complexity of accrual-based accounting. They show how cash moves into and out of a business. Product Managers Should Care About Cash Flow Statements.

What Are The Components of a Cash Flow Statement?

A Cash Flow Statement summarizes the amount of cash and cash equivalents entering and leaving a business. It has three major components:

- Cash from operating activities

- Cash from investing activities

- Cash from financing activities

From a product manager’s perspective, the cash from operating activities section is the most valuable. The other sections are interesting, but not as relevant.

Cash From Operating Activities

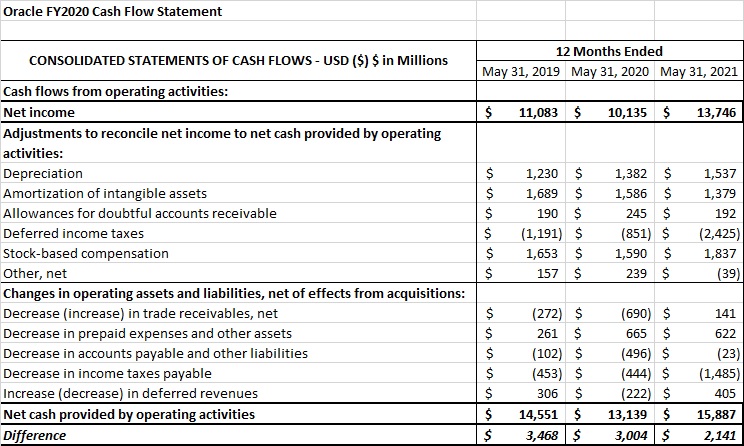

This section of a Cash Flow Statement is the most informative for product managers. What it does is strips out all of the non-cash items that were included in the Income Statement (aka P&L) Take a look at Oracle’s Cash Flow Statement:

The Net Income line comes from Oracle’s Income Statement. Net Income contains both cash and non-cash items. The non-cash items are a byproduct of accrual accounting. They mask how much cash the operations of the company generate. The two parts of this section. The first is ‘Adjustments to reconcile net income to net cash provided by operating activities’ The items like depreciation, amortization, and stock-based compensation are all non-cash items. The second part involves changes in ‘operating assets and liabilities, net of acquisitions.’ The decrease in accounts payable and other liabilities in an increase in cash flow. Operating expenses are typically paid on a monthly basis, which is why any reduction in prepaid expenses will immediately benefit cash flow for the current month.

A lot of the information in this section of the cash flow statement requires a solid understanding of accrual accounting. Product managers should focus on the net result. For example, in 2020 Oracle reported $13.746 billion in operating income. In total, they had $2.141 billion in non-cash adjustments. In other words, Oracle generated $15.887 billion in cash from their operations.

Cash from Investing Activities

This section of the Cash Flow Statement reports how much cash has been generated or spent from various investment-related activities. Investing activities include purchases of physical assets, investments in securities, or the sale of securities or assets.

Here is Zoom’s Cash from Investing Activities from 2020:

Generally, this section is not too interesting for product managers. It is more relevant for finance professions. Sometimes companies disclose the amount of capital expenditures in this section like Oracle does in its Cash Flow Statement. Since Zoom went public in 2021 they had a ton of cash from the IPO that they moved into marketable securities.

Some details about what certain things mean in this section:

Below are a few examples of cash flows from investing activities along with whether the items generate negative or positive cash flow.

- Purchase of fixed assets–cash flow negative

- Purchase of investments such as stocks or securities–cash flow negative

- Lending money–cash flow negative

- Sale of fixed assets–cash flow positive

- Sale of investment securities–cash flow positive

- Collection of loans and insurance proceeds–cash flow positive

Cash from Financing Activities

Cash Flow from Financing Activities is the net amount of funding a company generates in a given time period. Finance activities include the issuance and repayment of equity, payment of dividends, issuance and repayment of debt, and capital lease obligations.

Here is an example from Zoom:

The major cash inflow was the proceeds from Zoom’d IPO in 2021. Financing activities can include:

- Issuance of equity

- Payment of dividends

- Issuance of debt

- Repayment of debt

- Capital/finance lease payment

Net Change in Cash & Cash Equivalents

At the bottom of the Cash Flow Statement, the overall changes to a company’s cash position are summarized. Here are Oracle & Zoom’s summary:

Looking at the net change in cash is very helpful for product managers. If a business is building cash it is a sign of health. If a business has declining cash balances, a product manager can see whether it is operational or due to a combination of investments and financing.

How Can Product Managers Analyze a Cash Flow Statement?

Product managers can quickly analyze Cash Flow Statements. By focusing in on the changes in cahs flow from operations they can identify specific trends that should be investigated. Here is a look at Zomm’s changes over three years:

For Zoom the growth in net income was driven by the $2 billion increase in sales from $600 million in FY2019 to $2.6 billion in FY2020. The growth in stock-based compensation expense was a combination of rewarding employees and increased headcount. The growth in amortization of deferred contract acquisition costs is due to the incredible revenue growth. To learn more about contract acquisition costs check out this discussion of ASC 606..

How Can Product Managers Use This Information in Their Jobs?

Product managers can use information from Cash Flow Statements to better understand existing customers, prospective customers, and competitors. Cash Flow Statements enable product managers to see through the impact of non-cash accounting items. If a business has positive cash flow from operations you know they are being successful. If they have negative cash flow from operations you know they are having problems. Looking at investing and financing activities also provides important insights.

Also published on Medium.