Why Should Product Managers Care About Income Statements?

Financial literacy is not one of the top skills most product managers have. They may have learned about financial statements in university, but it is not something they use daily. Understanding how Income Statements, Balance Sheets, and Cash Flow Statements work is critical for several reasons. These skills can help product managers build better product value equations, business cases, and competitive analyses. The learning process starts with Income Statements (aka P&Ls).

Three Examples of Why Product Managers Should Care About Income Statements

To help product managers understand why it is important to care about income statements let’s examine three examples.

Customer Income Statements

Customer Income Statements give product managers insight into their business. You can determine the health or challenges a customer faces. Are their revenues growing or shrinking? Are they profitable or not? Understanding their income statements helps you to better position your products. You can speak a language that their executives are familiar with. If the company is public, they will file quarterly and annual financial statements with the SEC. You can read these filings for free and even download Excel versions of their income statements.

Competitor Income Statements

Competitor Income Statements provide another perspective of their business. If your competitors are public companies, you can learn a tremendous amount about them. You can see if they are growing or shrinking. You can see how much they are spending on activities like sales, marketing, and product development.

If your competitor is not public, you can look at other companies in their market that are public. Companies that offer similar products tend to have similar financial metrics. You can estimate a private company’s revenues in several ways. Check out Finding Revenues of Private Tech Companies. This information can help you understand the benchmarks for performance in your market.

Your Company’s Income Statements

Product managers rarely have access to their company’s Income Statements unless they are public companies. Sometimes you have access to summary or partial information. Income Statement data can help you understand how much revenue your product contributes to your company’s overall success. You can learn about profitability targets like gross margin and operating profit margins. You can see the trends in how much the company is investing in sales, marketing, and development. Armed with this type of information, you can make better cases for investment in your product. You can also discover key targets that your product must meet or face its possible elimination.

What Are The Components of an Income Statement?

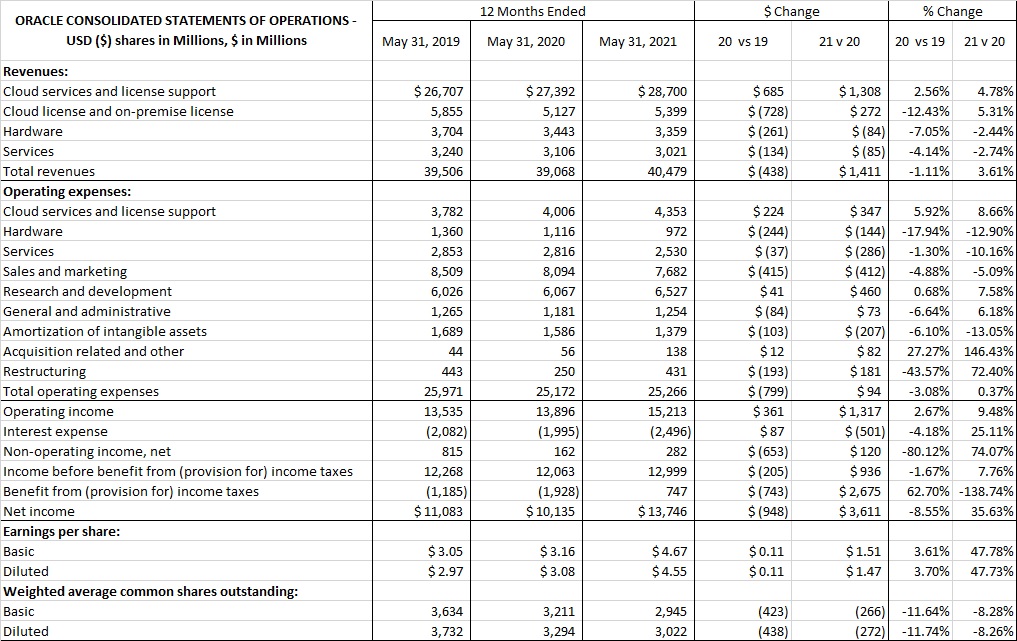

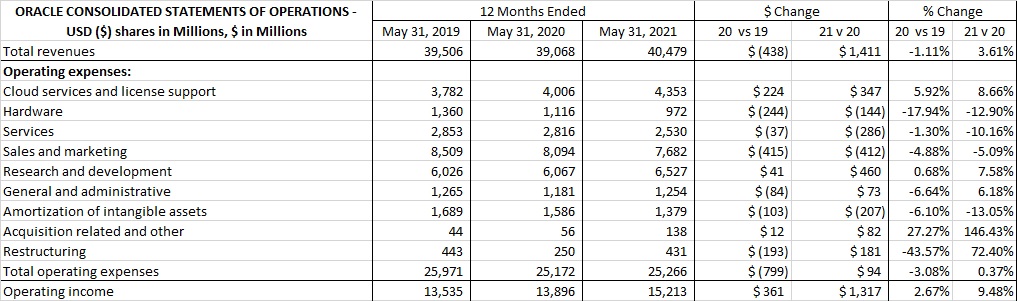

There are five major components for most tech companies’ income Statements. Here is Oracle Corporation’s Income Statement from the last fiscal year as an example.

Revenues

Revenues are the first component. Revenues are the sales that are recognized in a specific period. Oracle reports four types of revenue: cloud services and license support, cloud license and on-premise license, hardware, and services. Cloud services and license support are subscription revenues that are paid monthly or annually. Cloud license and on-premise license are perpetual licenses that are paid upfront. This was the normal business practice pre-SaaS. Hardware is the Sun Microsystems product line. Services are the professional services and training that Oracle offers its customers.

Product managers should understand the concept of revenue recognition and how it impacts their products. Revenue recognition is when a company can include specific sales transactions in its Income Statements. Consider a SaaS company whose fiscal year ends on December 31st. They sell an annual SaaS subscription to a customer in June for $120,000. The customer prepays the entire amount in July. The company is only allowed to ‘recognize $60,000 in the current fiscal year ($10,000/month). The remaining $60,000 will be recognized in the next fiscal year. As a result, the product manager’s product line will only get credit for the revenue recognized in the current fiscal year. This could impact their bonus among other things.

Revenue recognition is governed by the standards set by the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB). The specific policy is known as ASC 606 Contracts with Customers. ASC 606 not only deals with revenue recognition but expense recognition. This impacts a company’s profitability. AC 606 was initially launched in 2016 and all companies had to comply by 2020.

In the Oracle Income Statement, the cloud services and license support revenue line is an example of subscription revenues impacted by ASC 606. License support is what used to be called software maintenance revenue. These are services like customer support and software upgrades for on-premise licensed software like Oracle DBMS. Cloud license and on-premise license revenue cover perpetual licenses sold to customers. This was the industry standard pre-SaaS. These revenues are usually recognized all at once. Hardware revenues are similar. Services revenues are recognized as they are delivered.

Cost of Revenue/Cost of Goods Sold

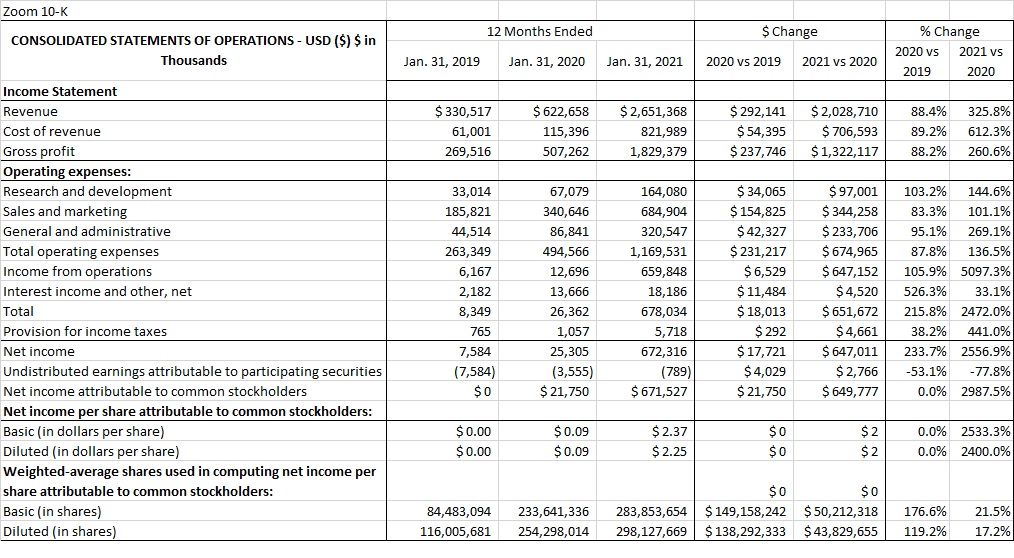

Cost of Revenue/Cost of Goods sold are the direct costs associate with providing a good or service to a customer. As noted in Zoom’s most recent 10-K:

Cost of revenue primarily consists of costs related to hosting our unified communications platform and providing general operating support services to our customers. These costs are related to our co-located data centers, third-party cloud hosting, integrated third-party PSTN services, personnel-related expenses, amortization of capitalized software development and acquired intangible assets, royalty payments, and allocated overhead.

Zoom 2021 10-K

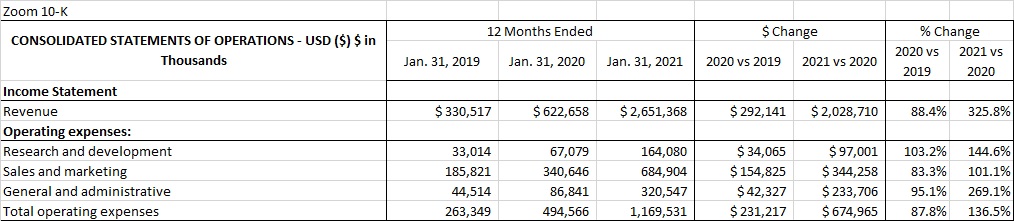

Here is Zoom’s Income Statement:

Gross Margin (aka Gross Profit) is a key metric for SaaS companies. Gross Margin is equal to Revenue – Cost of Revenue. Typical SaaS companies have Gross Margins of 80% to 90%.

Operating Expenses

Operating Expenses are the costs related to ongoing operations. They usually include three main sub-categories:

- Research & Development (product development)

- Sales & Marketing

- General & Administrative (e.g., HR, IT, Finance, real estate, and other administrative costs not otherwise attributed to R&D/S&M)

Most operating expenses are headcount-related. Product managers should learn about the operating expense ratios that are common in their industry. Young companies, like Zoom, will spend more on a percentage basis for things like sales and marketing. More mature companies, like Oracle, tend to spend less on a percentage basis. Companies that focus on the early stages of the technology adoption life cycle (Visionary/Early Adopters) will spend significantly more on a percentage basis on expenses like sales/marketing. Later stage companies that are focusing on Late Majority/Laggards spend less.

Other Expenses

Most companies report non-operational expenses in the ‘other expenses’ section of their Income Statement. They are usually below the net income line. This includes items like interest payments, taxes, depreciation/amortization, and other items. These expenses can have a big impact on the net income line. Occasionally it can increase the net income line.

Profit

There are two types of profit included in an Income Statement. Operating Profit is equal to Gross Margin minus Operating Expenses. Some companies, like Oracle, do not report Gross Margin. For them, Operating Income is equal to Revenue minus Operating Expenses.

The second type of profit is called Net Profit or Net Income. That is equal to Operating Profit minus Other Expenses. This number is used to calculate earnings per share (EPS).

Operating Profit and Net Income margins are important metrics for determining the health of a business. Many early-stage companies intentionally run large losses early in their existence. Uber, for example, had a multi-billion dollar net income for years.

What Are Some of the Tricky Things About Income Statements?

Most product managers do not have extensive accounting training. There are several aspects of Income Statements that are difficult to understand. Here are four examples:

ASC 606

ASC 606 Revenue from Contracts with Customers is an accounting standard from the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB). The primary goal was to have a single model for recognizing revenue for all industries. It replaces prior standards that were industry-specific and subject to abuse.

ASC 606 deals with two major topics: revenue recognition and expense recognition. This had a major impact on SaaS companies.

SaaS revenue recognition is unchanged. Many SaaS contracts operate on a month-to-month basis. The customer is billed for a month of service and they can cancel at any time. The revenue is recognized each month.

Many companies require annual contracts, often with a prepayment of the entire subscription upfront. In these cases, the prepayment is recorded as deferred revenue on the balance sheet. Revenue is recognized on a month-by-month basis and the deferred revenue balance is decreased accordingly. Maintenance fees for on-premise software are handled the same way.

On the expense side of things, many expenses like sales commissions are recognized over the term of the customer contract instead of all at once when they are paid. This generally results in higher profits.

ASC 606 is a complex topic that is beyond what most product managers know. Check out Why Product Managers Should Become Best Friends with Finance Team to learn how you can partner with your finance team to conquer knowledge deficits.

Deferred Revenue

Deferred revenue refers to advance payments a company receives for products or services that are to be delivered or performed in the future. A SaaS prepaid annual subscription is an example. While deferred revenue is more of a Balance Sheet topic, it has an impact on the Income Statement as well.

Product managers cannot tell how much revenue is coming from new sales versus deferred revenue in any Income Statement. Companies do not report it as a separate revenue line item. This makes it difficult to assess the health of a company’s revenue stream. How much revenue is coming from new sales versus how much is coming from prior sales?

Companies that are having cash flow challenges sometimes divert the cash they receive from prepayments to other uses. The cash is supposed to support the delivery of the service over time. If the company diverts the cash to short-term needs like payroll or sales commissions, they may have a problem down the road.

Stock-based Compensation Expense

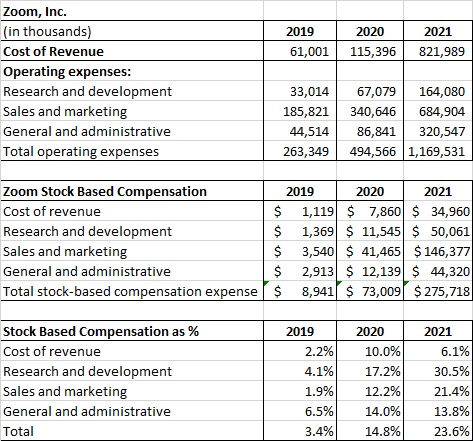

Companies use stock awards and stock options to compensate employees. They need to report the value of these awards as expenses in their Income Statement. This is known as stock-based compensation expense.

stock-based compensation expense.is a non-cash expense. Companies do not have to spend any cash for these awards. They do need to record the value of the awards. This is not a separate line item in the Income Statement. Instead, it is just included in the appropriate category. You have to dig into a public company’s SEC filings to find the details. Here is Zoom’s stock-based compensation expense:

As you can see, Stock-Based Compensation grew from 3.4% to 23.6% of Zom’s operating expenses.

Goodwill Impairment

Goodwill is an intangible asset that is recorded on the Balance Sheet.

“Goodwill is an intangible asset associated with the purchase of one company by another. Specifically, goodwill is recorded in a situation in which the purchase price is higher than the sum of the fair value of all identifiable tangible and intangible assets purchased in the acquisition and the liabilities assumed in the process. The value of a company’s brand name, solid customer base, good customer relations, good employee relations, and any patents or proprietary technology represent some examples of goodwill.”

Investopedia

For example, IBM added $25 billion of goodwill to IBM’s balance sheet as a result of the acquisition of Red Hat. In 2017 FASB changed the rules for goodwill accounting. Companies have to annually test whether goodwill had become impaired. When goodwill is impaired, companies must record it as an expense on the Income Statement. This can be significant.

Goodwill impairment results in an increased expense for the period in question and a reduction in net income. The most notorious example of goodwill impairment was AOL/Time Warner. According to an article from Time Magazine:

“Sticking out of AOL Time Warner’s rather humdrum earnings report Wednesday was a very gaudy number: A one-time loss of $54 billion. It’s the largest spill of red ink, dollar for dollar, in U.S. corporate history and nearly two-thirds of the company’s current stock-market value. (It’s also, as a lot of news outlets have noted, more than the annual GDP of Ecuador, but that’s hardly relevant here.) All for something called “goodwill impairment.

Why so many? Call it a bunch of drunken sailors nursing a hangover. When AOL and Time Warner first decided to merge, the dot-com love affair was raging and the stock of the combined companies was worth $290 billion, mostly thanks to the price of AOL. By the time the stock-swap deal closed a year later, the bubble had burst, AOL was back on earth, and even though AOL had technically been the acquirer (thanks to that high stock price), the new AOL Time Warner suddenly had a relative lemon on its hands.”

Software Capitalization

Companies are allowed to capitalize a portion of their software development costs. This creates an asset on the Balance Sheet. The asset is amortized over a period (3 years). This results in the expense being recognized over a long time instead of when it was incurred. This improves profitability in the short term. Software cap is not called out as a separate line in most Income Statements. Here is a description of Zoom’s software cap:

We capitalize certain development costs related to our unified communications platform during the application development stage as long as it is probable the project will be completed, and the software will be used to perform the function intended. Capitalized software development costs are recorded as part of property and equipment, net. Costs related to preliminary project activities and post-implementation activities are expensed as incurred. Capitalized software development costs are amortized on a straight-line basis over the software’s estimated useful life, which is generally three years, and are recorded in cost of revenue in the consolidated statements of operations. We evaluate the useful lives of these assets on an annual basis and test for impairment whenever events or changes in circumstances occur that could impact the recoverability of these assets. We have capitalized $19.4 million, $3.1 million, and $2.5 million of software development costs during the fiscal years ended January 31, 2021, 2020, and 2019, respectively.

https://www.sec.gov/ix?doc=/Archives/edgar/data/0001585521/000158552121000048/zm-20210131.htm#

Some companies have been known to use software capitalization as a tool to improve short-term profitability.

How Can Product Managers Analyze an Income Statement?

Product managers should learn how to analyze Income Statements. There are two main techniques.

Changes Over Time

The first thing product managers should do is calculate how line items in the Income Statement change over time. They should calculate the absolute dollar change, as well as the percentage of change.

The changes show the dynamics that are driving the business. The most important question product managers can ask is ‘why are the changes occurring?’ Zoom was able to grow its revenues by 325% between 2020 and 2021. That was over a $2 billion increase. As Zoom noted in their 10-K:

While we have experienced a significant increase in paid hosts and revenue due to the pandemic, the aforementioned factors have also driven increased usage of our services and have required us to expand our network, data storage, and processing capacity, both in our own co-located data centers as well as through third-party cloud hosting, which has resulted and is continuing to result, in an increase in our operating costs. Furthermore, a significant portion of the increase in usage of our platform is attributable to free Basic accounts and our removal of the time limit for school domains, which do not generate any revenue but still require us to incur these additional operating costs to expand our capacity. Therefore, the recent increase in usage of our platform has adversely impacted and may continue to adversely impact, our gross margin.

Zoom 2021 10-K

Understanding why changes are occurring is critical. Product managers should consider if the changes in their own or competitor’s Income Statements indicate that they are missing a key market trend.

Compare Against Benchmarks

Product managers should compare their performance against other companies in their industry. For example, operating expenses tend to move in proportion to changes in revenue. A sign of how efficient a company is when their operating expenses increase at a lower rate than what their revenues grow at. Here’s an analysis of Zoom and Oracle’s operating expenses metrics:

Here is a look at Zoom’s operating expenses:

Here is a look at Oracle’s operating expenses:

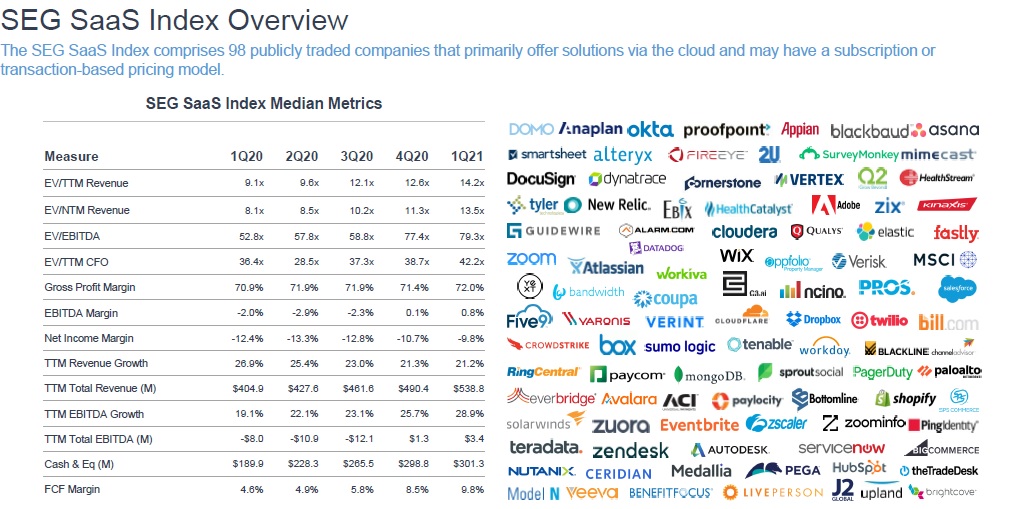

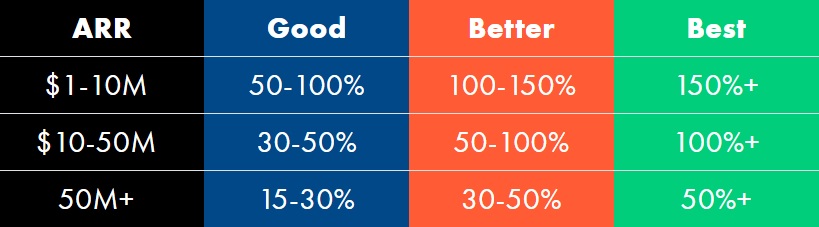

You can also compare your performance against industry averages. The Software Equity Group publishes great free SaaS industry research For example:

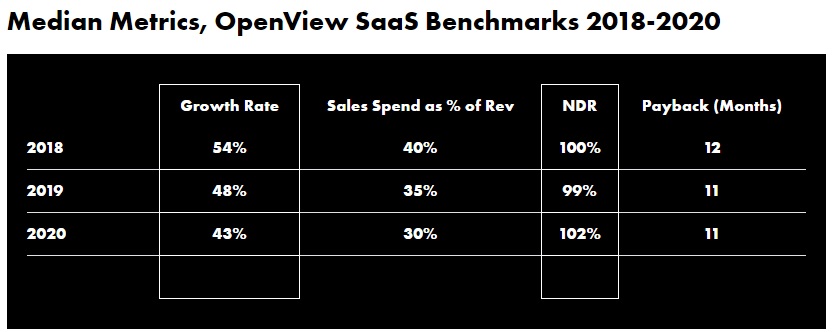

Openview Partners also publishes SaaS metrics. Here are some examples from their recent 2020 Saas Expansion Benchmarks report.

How Can Product Managers Use This Information in Their Jobs?

There are three main ways product managers can leverage Income Statement knowledge in their jobs.

Build Better Value Equations & Proof Points

Value equations are the customer perceived benefits minus the price/cost of the solution. Proof points are irrefutable evidence value. Proof points need to be accurate, convincing, and believable. Income Statement knowledge helps product managers craft better value equations and proof points.

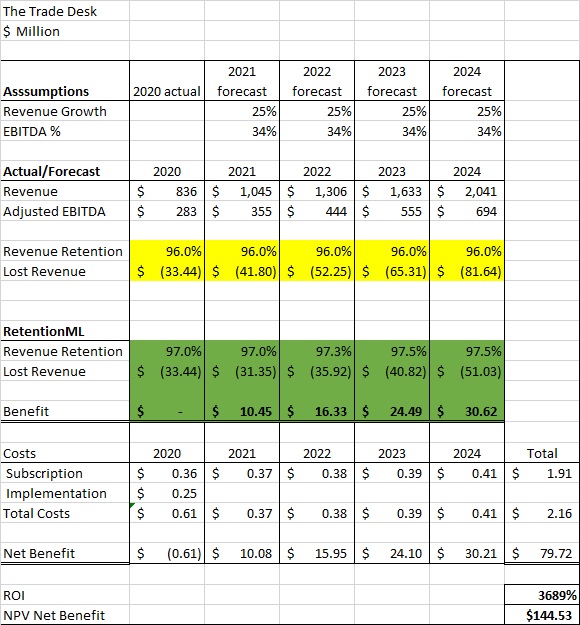

Assume you were a product manager of a SaaS solution called RetentionML. The solution helps SaaS companies increase revenue retention. Your solution can reduce revenue churn by 25% by combining machine learning and deep integration with CRM systems. You have three major SaaS customers that will attest to your solution’s benefits.

You have an opportunity to pitch an enterprise SaaS provider, like The Trade Desk, They are a publicly traded provider of SaaS digital advertising solutions. You could state that RetentionML could reduce The Trade Desk’s revenue retention by 25% and cite the testimonials from your reference customers.

Or you could leverage your knowledge of The Trade Desk’s Income Statement to present the benefits in dollars and cents. Upon reviewing their 2020 Income Statement and 10-K report you learned that they had 2020 revenues of $836 million and adjusted EBITDA of $283 million. They cited that they had 96% revenue retention. You could create a model that shows the impact your solution could have.

Competitive Analysis

Product managers can use knowledge about competitor Income Statements to offer fact-based interpretations of their performance. Understanding the revenue, expense, and profitability trends can help a product manager identify opportunities that they may have missed.

Income Statement knowledge can also help counteract the disproportionate impact effect. Salespeople will frequently cite aggressive competitive pricing as a reason why they lost a deal. This type of anecdotal gossip can spread throughout an entire salesforce. A product manager can dispel this gossip by pointing out that the competitor’s revenues have declined in the last three years and their revenue retention is only 75%. Excessive discounting is their futile strategy to grow revenues at any cost

Business Cases

Income Statement knowledge helps product managers to build credible business cases. Knowledge of how a proposed product or initiative financially contributes to the overall business is critical. Leveraging understanding of ‘tricky’ Income Statement items like ASC606 revenue recognition and deferred revenue helps convince executives.

Perhaps the most important thing is the ability to express how a business case will increase the company’s enterprise value Executive compensation is often based on increases in enterprise value.

Summary

Product managers can benefit from learning the details of how income statements work. Building effective value equations, competitive analyses, and business cases are core parts of a product manager’s job. Understanding the details of Income Statements (aka P&Ls) is a necessary skill. Product managers should care about Income Statements.