Why Should Product Managers Care About Balance Sheets?

Balance sheets are a somewhat esoteric topic for product managers. Balance sheets describe a company’s assets, liabilities, and stockholder equity on a specific date. Balance sheets contain many interesting facts. They help product managers do a better job of understanding customers, competitors, and even their own company. Product managers should care about balance sheets.

Three Examples of Why Product Managers Should Care ABout Balance Sheets

To help product managers understand why it is important to care about Balance Sheets. Let’s look at three examples.

Avoiding a Major Contract Renegotiation

A vendor-provided an outsourced service to a mortgage processing company. The service received mortgage applications, used OCR to extract data, and loaded them into an Oracle database. During the Great Recession of 2008, the company had large revenue losses, The contract cost $1.5 million a year. The customer wanted to reduce the cost to $500,000 or they would bring the application in-house. The salesperson wanted to agree since they were compensated on revenue. Some revenue was better than no revenue.

Fortunately, a product manager on the pricing committee did some research. Since the customer was a public company he could review their financial statements. He learned that they only had $5 million in cash as well as some harsh debt covenants. It would cost the company over $1 million to bring the solution in-house. The product manager realized it was unlikely the customer would invest 20% of their cash in a solution they were not experts in. With this information, the team was able to renegotiate the contract with only a minimal price reduction.

Deferred Revenue Crisis

Deferred Revenue refers to advance payments a company receives for products or services that are to be delivered or performed in the future. A prepaid annual subscription for a SaaS solution is an example. Deferred revenue is recorded as liabilities on the balance sheet.

A portion of the payments is intended to support the delivery of the service over time. A challenge some companies face is that they spend the cash received from advance payments on other things than service delivery. This is common for companies facing cash flow crises. The problem arises when there is no cash left to support the long-term delivery of the SaaS service. Customers become dissatisfied, don’t renew contracts, and the cash flow crisis grows.

Goodwill Impairments

Goodwill is an intangible asset on the balance sheet. It arises when a company pays more than the fair market value for an asset. Many tech acquisitions add significant goodwill to a balance sheet. When IBM acquired Red Hat, it added $25 billion in goodwill to its balance sheet.

In 2017 FASB changed the rules for goodwill accounting. Companies have to annually test whether goodwill had become impaired. Goodwill impairment results in an increased expense for the period in question and consequently a reduction in net income and earnings per share. The most notorious example of goodwill impairment was AOL/Time Warner. According to an article from Time Magazine:

“Sticking out of AOL Time Warner’s rather humdrum earnings report Wednesday was a very gaudy number: A one-time loss of $54 billion. It’s the largest spill of red ink, dollar for dollar, in U.S. corporate history and nearly two-thirds of the company’s current stock-market value. (It’s also, as a lot of news outlets have noted, more than the annual GDP of Ecuador, but that’s hardly relevant here.) All for something called “goodwill impairment.

Goodwill impairments reduce a company’s profitability. This often triggers headcount and other expense reductions.

What Are The Components of a Balance Sheet?

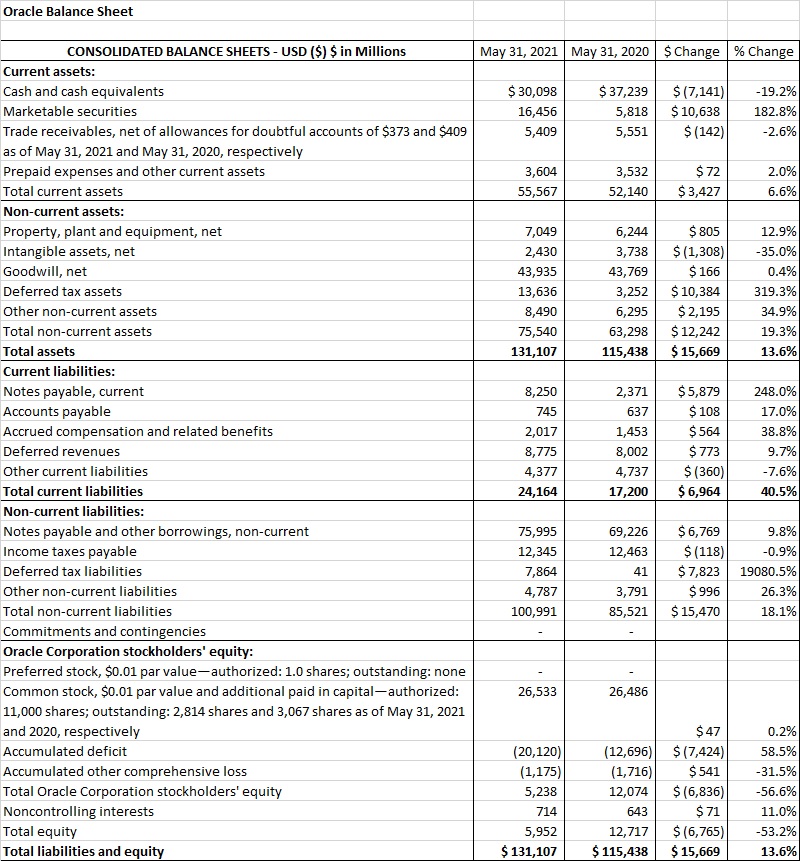

Balance sheets gave three components: Assets, Liabilities, and Stockholder Equity. Balance Sheets show the value of items as of a specific reporting date. The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity. Here is Oracle’s balance sheet from their most recent fiscal year:

For public companies, you can access quarterly and annual financial statements filed with the SEC. You can even download Excel versions of the filings.

Assets

There are two types of assets; short-term and long-term. Short-term assets (aka Current Assets).are assets that can be turned into cash within a year. Long-term assets (aka Non-Current Assets) can stay on the balance sheet for years.

Cash, marketable securities, and accounts receivable are all examples of current assets. Items like plant, property, & equipment, intangible assets, goodwill, and deferred tax assets are long-term assets. It is important to note items like goodwill and intangible assets are non-cash items. They cannot be readily converted to cash-like marketable securities. Product managers should see a red flag if these types of non-cash assets represent the majority of a company’s assets.

An important metric SaaS product managers should look at is Days Sales Outstanding (aka DSO). DSO is an indication of how quickly customers pay their bills. The DSO calculation is simple:

High DSOs (>60 days) indicate that the company’s customers are slow payers. It can also demonstrate that the company has overly generous credit terms. As noted by KPISense

DSO benchmarks will vary industry by industry – some have a median DSO of 30 days and others have 90 days.

Shopify, a B2C SaaS company, has a DSO of approximately 20 days. On the other hand, Microsoft, mainly a B2B SaaS company, has a DSO of approximately 77 days. Product, customers, and niche industries can impact what makes a DSO acceptable or not.

KPISense

Liabilities

There are two types of Liabilities: short-term and long-term. Here is Zoom’s Fy2020 Balance Sheet:

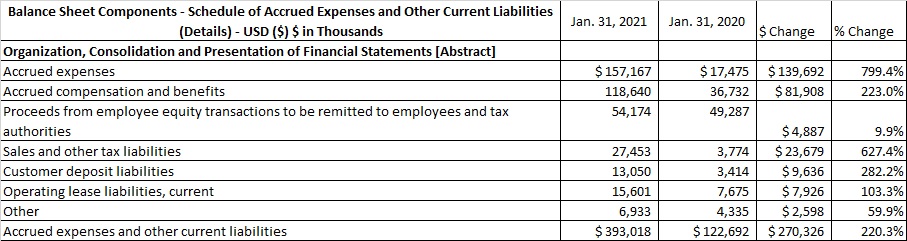

Most items are self-explanatory. Zoom grew its revenues by over $2 billion in 2021 (325%). Logically, items like accounts payable would grow significantly. Zoom provided more detail about the growth of accrued expenses and other current liabilities:

Zoom reports long-term deferred revenue. This is for advance payments that cover more than one year. Zoom reported $858 million of current deferred revenue (due in less than a year) and only $25 million in non-current deferred revenue (due in more than a year).

Debt

Balance sheets list the total value of a company’s debt. Debt that is due within one year is listed as a current liability. Debt that is due in more than one year is listed as a long-term liability. Oracle has more than $80 billion in short and long term debt (listed as notes payable):

Debt is a common source of funding, especially for companies owned by private equity firms. Private equity firms often use debt to finance acquisitions.

Debt often comes with covenants. Covenants set out certain activities that will or will not be carried out by the borrower. These restrictions help the lender ensure that the debt will be repaid. An example covenant is the EBITDA/Interest coverage ratio. Many lenders require that a borrower generate EBITDA that is 2 to 5 times larger than the annual interest payments. Another common covenant is what a company can do when they generate more cash than it had planned. An excess cash sweep is a covenant that requires a company to make additional debt principal payments when their actual business performance exceeds what they had negotiated with the lender. Debt, interest payments, and covenants can impose significant restrictions on a company’s operations.

Stockholders’ Equity

Stockholders Equity is the third component of a balance sheet. Stockholders’ equity is the remaining amount of assets available to shareholders after all liabilities have been paid. It is calculated either as a firm’s total assets less its total liabilities or as the sum of share capital and retained earnings less treasury shares.

From a product manager’s perspective, stockholders’ equity is a sign of the relative health or distress of a company. Positive stockholders’ equity indicates that the company has created value for its shareholders. Negative stockholders’ equity indicates significant problems. The company’s liabilities exceed its assets.

Tricky Things About Balance Sheets

Balance Sheets can be hard for product managers to understand. There are a few items that are important to understand.

Cash vs Non-Cash Items

One item that is often confusing for product managers is the difference between cash and non-cash items on the balance sheet.

Many items are straightforward. Assets like cash, marketable securities, accounts receivables, prepaid expenses, interest payments, etc. are cash items. Other items like goodwill and deferred tax liabilities are not cash, but an accounting construct. Product managers should focus more on cash-related items.

Deferred Revenue

Deferred revenue refers to advance payments a company receives for products or services that are to be delivered or performed in the future. A SaaS prepaid annual subscription is an example.

Deferred revenue is a by-product of the revenue recognition process. Many SaaS contracts operate on a month-to-month basis. The customer is billed for a month of service and they can cancel at any time. That revenue is recognized each month.

Revenue recognition is when a company can include specific sales transactions in its Income Statements. Consider a SaaS company whose fiscal year ends on December 31st. They sell an annual SaaS subscription to a customer in June for $120,000. The customer prepays the entire amount in July. Since the contract is only for one year, the $120,000 is recorded as a current liability. Each month the liability balance would be reduced as revenue is recognized.

Companies that are having cash flow challenges sometimes divert the cash they receive from prepayments to other uses. The cash is supposed to support the delivery of the service over time. If the company diverts the cash to short-term needs like payroll or sales commissions, they may have a problem down the road.

Deferred revenues are governed by an accounting standard known as ASC 606 Revenue from Contracts with Customers from the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB). ASC 606 is a complex topic that is beyond what most product managers know. Check out Why Product Managers Should Become Best Friends with Finance Team to learn how you can partner with your finance team to conquer any knowledge deficits.

Goodwill

Goodwill is an intangible asset that is recorded on the Balance Sheet.

“Goodwill is an intangible asset associated with the purchase of one company by another. Specifically, goodwill is recorded in a situation in which the purchase price is higher than the sum of the fair value of all identifiable tangible and intangible assets purchased in the acquisition and the liabilities assumed in the process. The value of a company’s brand name, solid customer base, good customer relations, good employee relations, and any patents or proprietary technology represent some examples of goodwill.”

Investopedia

For example, IBM added $25 billion of goodwill to IBM’s balance sheet as a result of the acquisition of Red Hat. In 2017 FASB changed the rules for goodwill accounting. Companies have to annually test whether goodwill had become impaired. When goodwill is impaired, companies must record it as an expense on the Income Statement. This can be significant.

Goodwill impairment results in an increased expense for the period in question and a reduction in net income. The most notorious example of goodwill impairment was AOL/Time Warner. According to an article from Time Magazine:

“Sticking out of AOL Time Warner’s rather humdrum earnings report Wednesday was a very gaudy number: A one-time loss of $54 billion. It’s the largest spill of red ink, dollar for dollar, in U.S. corporate history and nearly two-thirds of the company’s current stock-market value. (It’s also, as a lot of news outlets have noted, more than the annual GDP of Ecuador, but that’s hardly relevant here.) All for something called “goodwill impairment.

Why so many? Call it a bunch of drunken sailors nursing a hangover. When AOL and Time Warner first decided to merge, the dot-com love affair was raging and the stock of the combined companies was worth $290 billion, mostly thanks to the price of AOL. By the time the stock-swap deal closed a year later, the bubble had burst, AOL was back on earth, and even though AOL had technically been the acquirer (thanks to that high stock price), the new AOL Time Warner suddenly had a relative lemon on its hands.”

Product managers should be on the lookout for goodwill impairments. A significant impairment might encourage an executive team to decrease or eliminate funding for a product manager’s product.

Software Capitalization

Companies can capitalize a portion of their software development costs. This creates an asset on the Balance Sheet. The asset is amortized over a period (3 years). This results in the expense being recognized over a long time instead of when it was incurred. This improves profitability in the short term. Software cap is not called out as a separate line in most Income Statements. Here is a description of Zoom’s software cap:

We capitalize certain development costs related to our unified communications platform during the application development stage as long as it is probable the project will be completed, and the software will be used to perform the function intended. Capitalized software development costs are recorded as part of property and equipment, net. Costs related to preliminary project activities and post-implementation activities are expensed as incurred. Capitalized software development costs are amortized on a straight-line basis over the software’s estimated useful life, which is generally three years, and are recorded in cost of revenue in the consolidated statements of operations. We evaluate the useful lives of these assets on an annual basis and test for impairment whenever events or changes in circumstances occur that could impact the recoverability of these assets. We have capitalized $19.4 million, $3.1 million, and $2.5 million of software development costs during the fiscal years ended January 31, 2021, 2020, and 2019, respectively.

Zoom 10-K

Some companies have been known to use software capitalization as a tool to improve short-term profitability.

How Can Product Managers Analyze Balance Sheets?

Product managers should learn how to analyze Balance Sheets. There are three main techniques.

Changes Over Time

The first thing product managers should do is calculate how line items in the Balance Sheet change over time. They should calculate the absolute dollar change, as well as the percentage of change. Consider Zoom’s most recent balance sheet:

The changes show the dynamics that are driving the business. The most important question product managers can ask is ‘why are the changes occurring?’ In the case of Zoom, the growth in cash was driven by their IPO in 2021:

On January 15, 2021, we completed our follow-on public offering, in which we issued and sold 5,882,353 shares of our Class A common stock, including 735,294 shares pursuant to the full exercise of the underwriter’s option to purchase additional shares, at $340.00 per share. We received aggregate proceeds of $1,980.0 million, net of underwriters’ discounts and commissions. The other related offering costs were immaterial.

Balance Sheet Ratios

Several standard financial analysis ratios can be helpful to product managers.

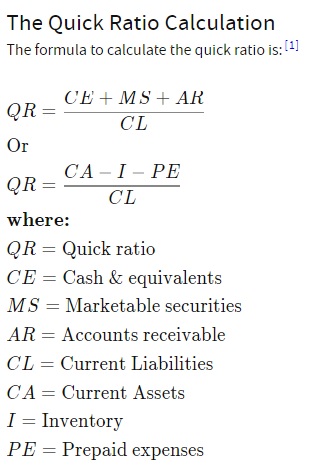

Quick Ratio

The quick ratio measures a company’s ability to meet its short-term obligations with its most liquid assets. The formula is:

Here is Zom’s Quick Ratio from January 2021:

Anything below 1.0x is a sign of financial distress.

Debt to Asset Ratio

The debt to asset ratio calculates how much of your business’s assets were purchased through debt rather than equity. The formula is total liabilities / total assets. Here is Zoom’s:

Is 0.27x a good debt to asset ratio? Here are some general benchmarks:

| Debt to asset ratio | Business risk level |

| Over 1 High | High-you have more debt than assets |

| 0.6 and higher | High-you may have trouble borrowing money |

| 0.4 and lower | Low |

How Can Product Managers Use This Information in Their Jobs?

Customer Analysis

Product managers can use their understanding of a customer’s balance sheet to more effectively position their offerings. As noted in the example cited earlier, a product manager was able to avoid an unnecessary price reduction for an outsourced offering when they realized the customer did not have the cash to pay for a project to bring the solution in-house. A product manager’s understanding of debt covenants could help them better position their offerings. They could show how their offering could improve profitability and cash flow.

Competitive Analysis

Product managers can use knowledge about competitor Balance Sheets to offer fact-based interpretations of their performance. Understanding the trends in assets and liabilities would give product managers insight into the health of their competitors. Understanding debt agreements and covenants would help them understand constraints that impact the competitor’s ability to invest..

Balance Sheet knowledge can also help counteract the’ disproportionate impact effect’. Salespeople will frequently cite aggressive competitive pricing as a reason why they lost a deal. This type of anecdotal gossip can spread throughout an entire salesforce. A product manager can dispel this gossip by pointing out that the competitor’s need for revenue growth to fund interest payments could drive them to discount to get revenue at any cost.

Summary

Balance sheets are an esoteric topic for product managers. They contain a lot of interesting facts that can help product managers understand the financial condition of costomers, competitors, and even their own company. Product managers do not need a degree in accounting to be effective in their jobs. They need to understand a few basic things about assets, liabilities, and stockholders’ equity.. Sometimes these details can make a big difference in commercial discussions. They can also help understand competitors’ weaknesses and constraints that impact their ability to compete. Product managers should care about Balance Sheets.

{kind=link}