In 2019 I wrote a post about an interesting startup called Gong.io. Gong is a revenue intelligence platform for B2B sales teams. It helps close more deals by shining the light on your team’s sales conversations. It records, transcribes, and analyzes sales calls so you can drive sales effectiveness across your entire team. In my post, AI Listened to 1,000,000 Sales Calls – What Do You Think It Learned?, I reviewed Gong’s core technology and value equations. I found it interesting but was concerned that sales reps would resent another inspection tool into the day-to-day work. Today a few random articles about Gong popped up in my feed. I did a little research into Gong’s recent performance. I asked myself “Why is a $120 million ARR SaaS Company Worth $7 Billion?”

What is Gong.io?

Gong is a SaaS application for sales teams. It records, transcribes, and analyzes sales telephone or video calls using artificial intelligence. Some of the things Gong can analyze include:

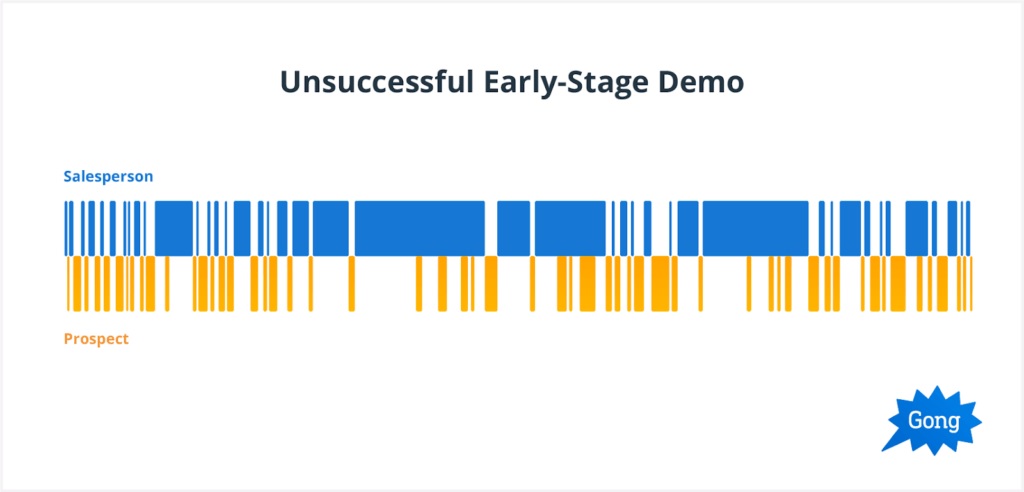

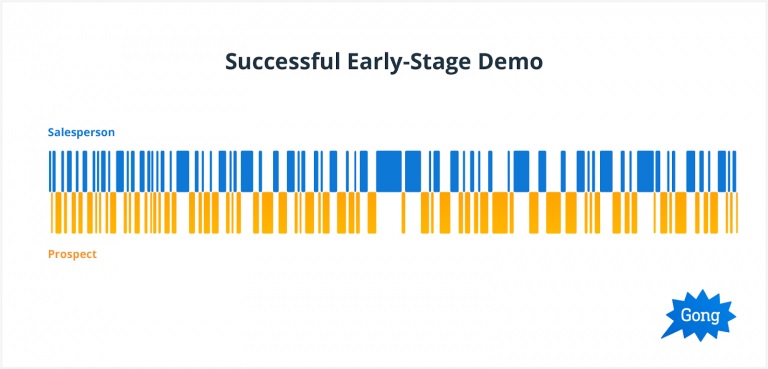

Talk/Listen Ratios

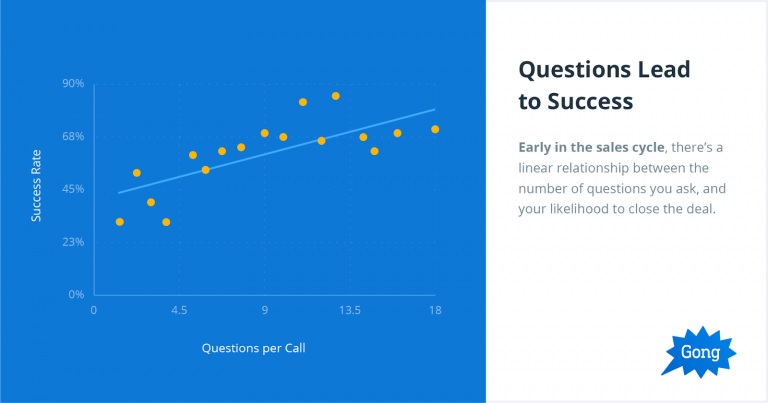

# of Questions Asked

Talk Patterns

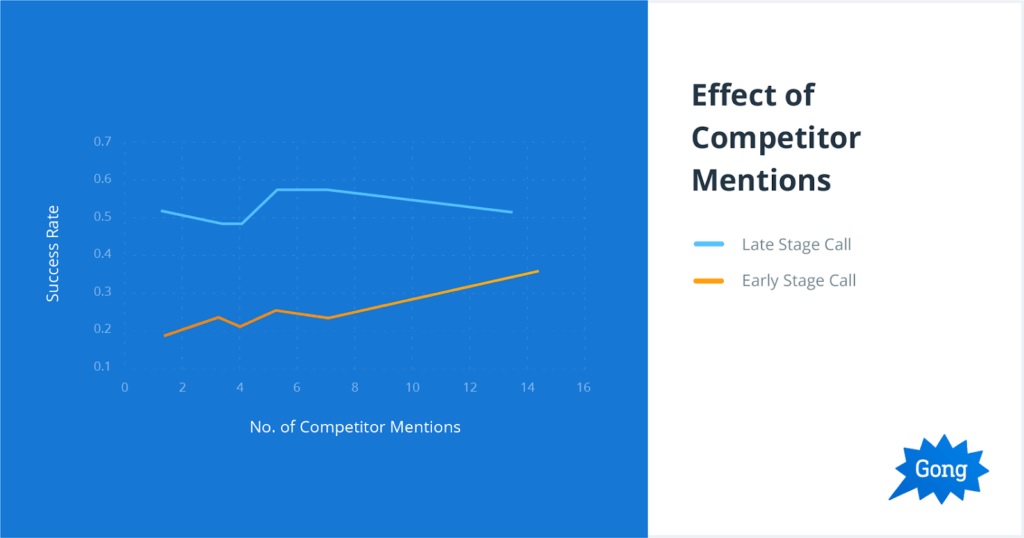

Competitor Mentions

Buyer Concerns

How Is It Used?

Sales coaching is the primary use case of Gong. Sales leaders can develop fact-based insights into sales rep interactions with prospects and customers. The habits of successful salespeople can be identified and shared. Bad habits can be highlighted and appropriate corrective actions implemented. The AI can help provide insight into pipeline quality and market intelligence.

Gong is tightly integrated with the tools sales use every day. There are calendar, CRM, telephony, and video conferencing integrations. This includes products like Outlook, GSuite, Salesforce, Zoom, Teams, WebEx, 34 telephony systems.

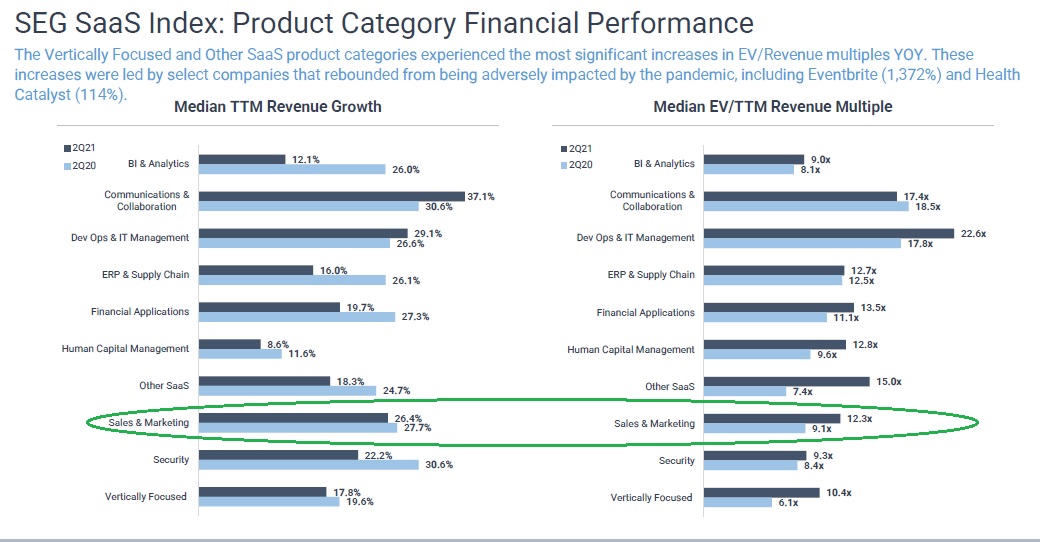

What Are Comparable SaaS Companies Worth in 2021?

The best way to measure the value of SaaS companies is Enterprise Value. Enterprise value represents the total costs to acquire a company. It is more comprehensive than market cap. Simply put, Enterprise Value = value of common stock minus cash plus debt. There are other factors like pension liabilities and minority interests that usually do not come into play for SaaS companies.

Enterprise value is often described as a ratio, such as Enterprise Value / Revenue (trailing twelve months) or Enterprise Value / EBITDA (ttm). In the second quarter of 2021, the median EV/Revenue ratio for public SaaS companies was 14.3x.

Some SaaS markets have higher valuations than others:

The median EV/Revenue for sales and marketing SaaS in Q2 2021 was 12.3x.

Gong Valuation Q2 2021

To put Gong’s valuation in context here is some background:

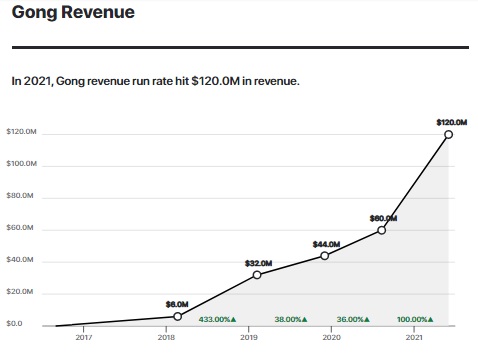

Gong Revenues

Gong posted $120 million annual revenue run rate in 2021:

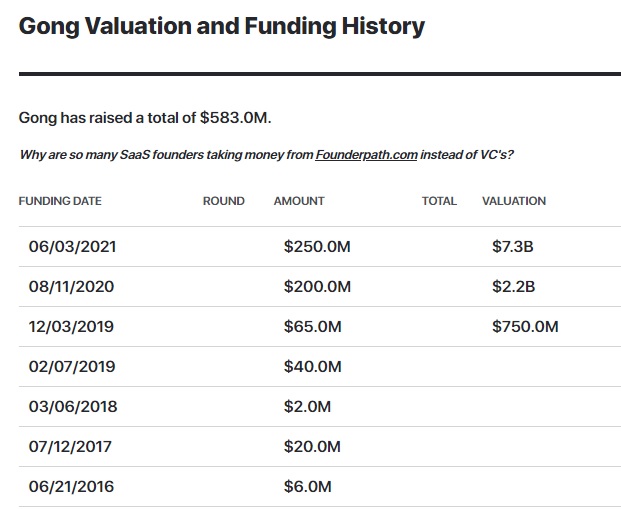

Gong Funding History

Gong Valuation

Gong’s investors valued Gong at $7.25 billion in June 2021 when they raised $250 million in their Series E funding round.

Estimating the valuation of private companies is hard. Private companies are usually valued at a discount in comparison to their public company peers. There are three major factors that impact private SaaS company valuations and there are six minor factors:

Major Private SaaS Company Discount Factors

- Liquid equity

- Audited Financials

- SOX 404 certifications

Minor Private Company Discount Factors

- Revenue Scale & Growth Rate

- Market Size

- Revenue Retention Rate

- Gross Margin & Revenue Mix

- Customer Acquisition Efficiency

- Profitability

When comparing private company valuations to their public peers, investors consider whether a company is performing better than the median performance of the public peers. Generally, private SaaS companies are valued at a 10% o 50% discount to their public peers. For more information check out Why are Private SaaS Companies Valued Less Than Public Peers?

Recent Transactions

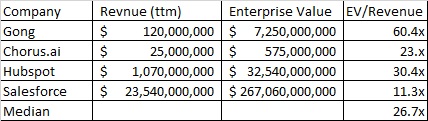

In June 2021 ZoomInfo (NASDAQ ZI) acquired Chorus.ai, Gong’s #2 competitor for $575 million. Chorus.ai had estimated revenues of $25 million Which translates to an EV/Revenue multiple of 23.0x.. At its recent valuation, Gong had an EV/Revenue ratio of 60.4x. The following table puts these numbers into context:

Why is Gong Worth $7 Billion?

There are a few reasons why a $125 million ARR company is worth $7 billion.

It Solves a Valuable Problem

Scaling sales performance is a hard problem. Companies that solve it are richly rewarded. Those that fail are punished.

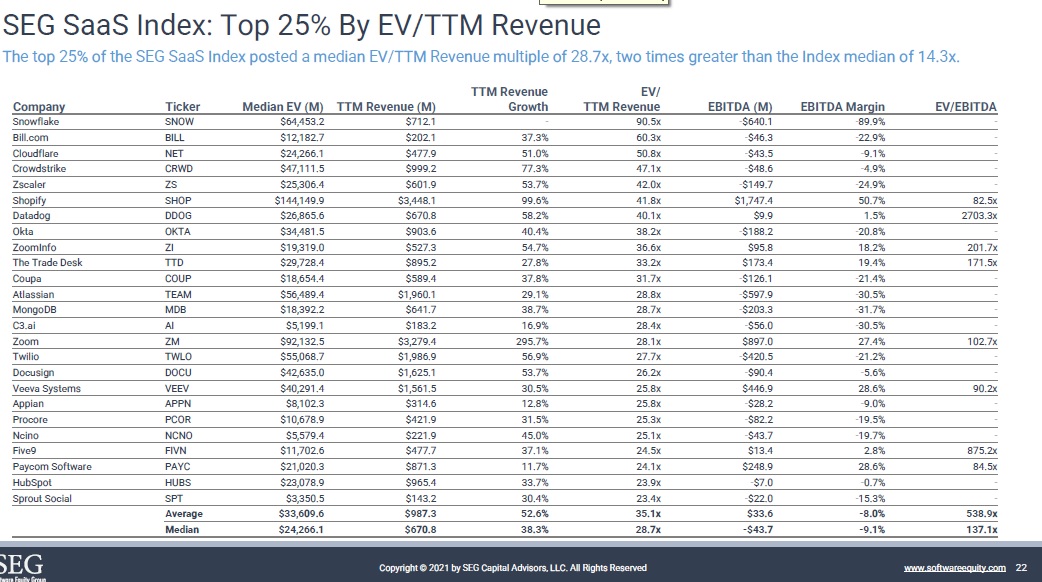

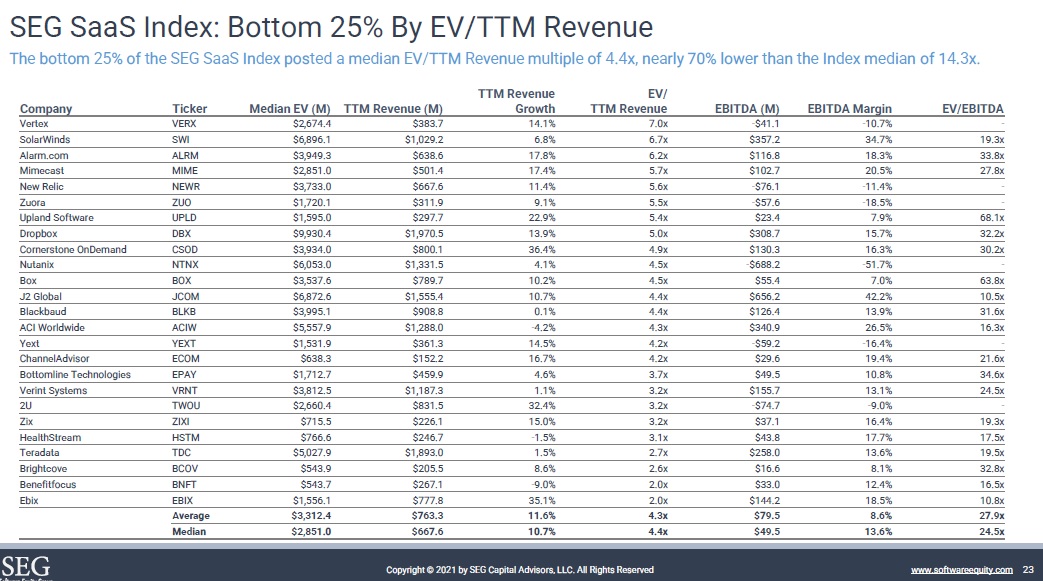

The scale of revenues and revenue growth rates are key factors. SaaS companies with larger revenues and revenue growth rates have higher valuations. Consider this list of the top and bottom 25 SaaS companies in the Software Equity Group SaaS SaaS Index:

Gong Has a Clear Return on Investment

Gong commissioned Forrester Consulting to conduct a Total Economic Impact™ (TEI) study and examine the potential return on investment (ROI) enterprises may realize by deploying Gong’s Revenue Intelligence Platform. Forrester found:

- Quantifiable Benefits

- Increase in incremental profit, leading to an additional $5.66M in deals won.

- Reduced time spent on low-value tasks, saving $4.2M over three years

- Reduced time for onboarding by 50%

- Increased sales manager productivity, saving 400 hours each year

- Unquantified benefits

- Reduced talent attrition and increased talent retention

- Increased visibility into sales performance insights and voice of the customer (VoC) data.

- Increased transparency around performance goals.

- Provided accurate transcriptions of recorded sales calls

- Costs

- Gong annual subscription and user seat costs of less than $1.4M.

- Additional reinforcement training for new features at a cost of $261,117 over three years.

- Internal labor costs to implement and maintain Gong of $428,982 over three years.

The customer interviews and financial analysis found that a composite organization experiences benefits of $12.1M over three years versus costs of $2M, resulting in a net present value (NPV) of $10M and an ROI of 481%.

Valuation is in the Eye of the Beholder

At the end of the day, valuation is what a willing buyer will pay a willing seller. Gong’s investors in the most recent round led by Franklin Templeton, and existing Gong investors Coatue, Salesforce Ventures, Sequoia, Thrive Capital, and Tiger Global are a who’s who of sophisticated venture capitalists.

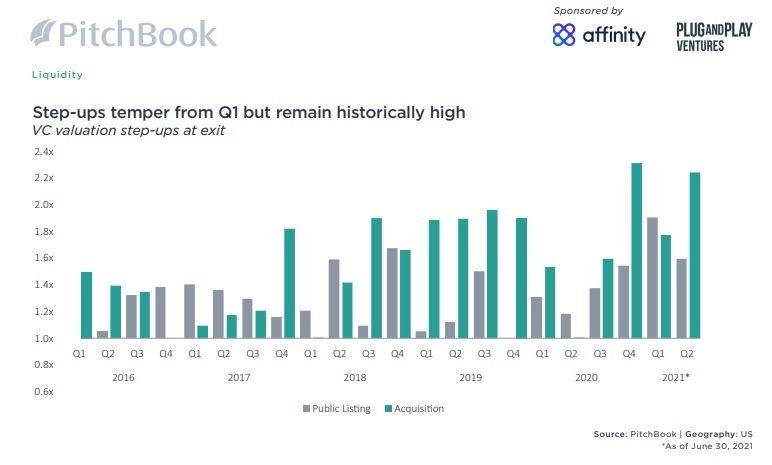

They are betting that Gong when it goes public, will deliver a huge ‘step up’ in valuation. Pitchbook recently reported that:

Summary

SaaS valuations are at an almost all-time high. The Software Equity Group reported that the median EV/Revenue multiple for public SaaS companies in Q2 2021 was 14.3x. The top 25 SaaS companies in the SEG SaaS Index had EV/Revenue valuations that ranged from 25.3x (Sprout Social) to 90.4x (Snowflake). While Gong’s most recent valuation is high – 60.4x – it is not unreasonable. Gong has shown consistent high revenue growth coupled with a strong ROI for its customers.

Full Disclosure: I have no relationship with Gong. I have not consulted with them in the past – I just find their technology and journey interesting.

Also published on Medium.