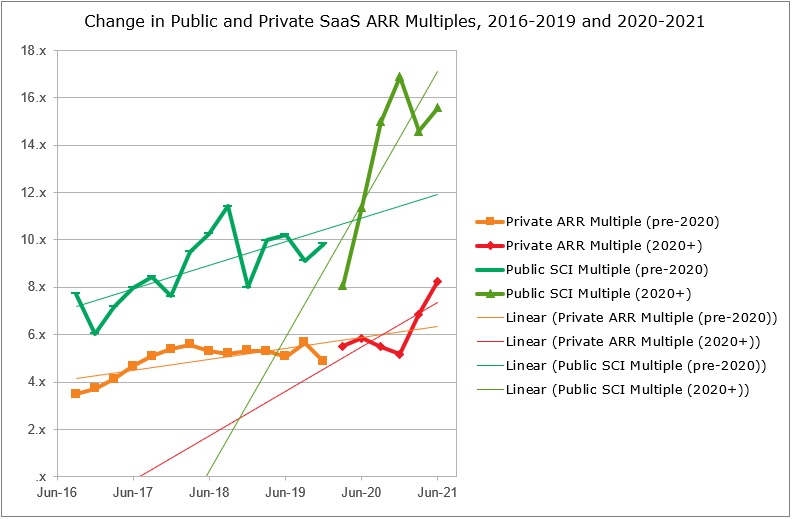

Public-Private SaaS Valuation Gap Now Over 50%

Private SaaS companies have always been valued less than their public company peers. SaaS Capital recently reported that the gap had grown to almost 50%. A public SaaS company may be valued at 16x Enterprise Value/Revenue, its private company peer would only be 8x. There are many reasons why in 2020 this gap has grown so much.

The Basics: Enterprise Value/Revenue Valuation Multiples

What is Enterprise Value?

There are many ways to measure the value of a SaaS company – market cap, enterprise value, discounted cash flow analysis. Enterprise value is perhaps the most common metric used to describe the value of a SaaS company. The formula for enterprise value is straightforward:

Enterprise Value Formula=

+ common equity at market value (this line item is also known as “market cap”)

+ debt at market value (here debt refers to interest-bearing liabilities, both long-term three-step and short-term)

– cash and cash equivalents

+ minority interest at market value, if any

+ preferred equity at market value (preferred shares/liquidation preferences)

+ unfunded pension liabilities and other debt-deemed provisions

– value of associate companies

Most major stock reporting services will calculate Enterprise Value automatically for public companies. Calculating the enterprise value of a private company is hard. There is no public source of the value of a private company’s equity. There are no publicly available audited financial statements or regulatory certifications. It is possible to estimate the enterprise value of a private SaaS company. For more details check out How to Calculate the Enterprise Value of a Private Company

Enterprise Value Valuation Multiples

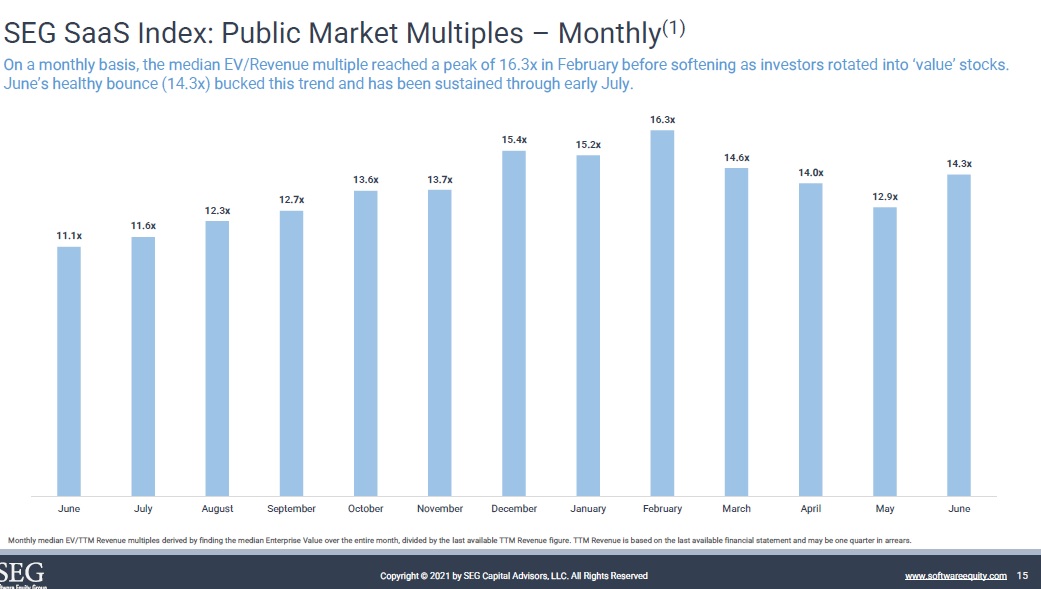

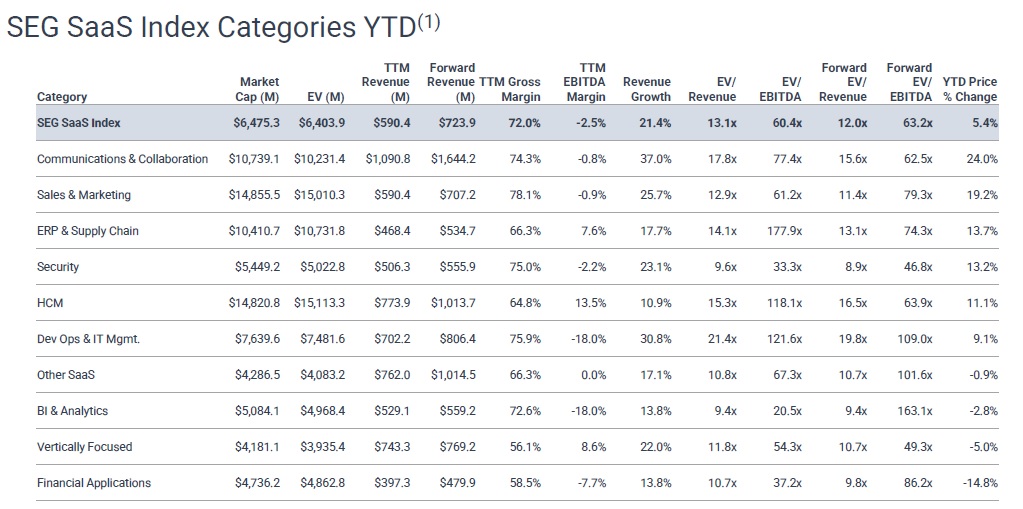

SaaS companies’ valuations are often expressed as multiples of Enterprise Value. Enterprise Value/Revenue and Enterprise Value/EBITDA are two of the most popular. The Software Equity Group regularly publishes valuation data about public SaaS firms. Here are some excerpts from their most recent research:

Public company SaaS valuations are near an all-time high. Certain market segments are considered to be more valuable than others — DevOps at 22.6x is the leading category while BI & Analytics is the lowest at 9.0x

The Gap Between Private SaaS Company and Public SaaS Company Valuations

Private SaaS companies have always been valued at a discount to their public peers. SaaS Capital finances Software-as-a-Service companies. They lend between $2 million and $12 million to scaling B2B SaaS companies. SaaS Capital publishes great free research focused on private SaaS companies, which is pretty hard to come by. They recently published some updated research on the gap between private SaaS companies and public SaaS valuations – Public-Private Valuation Gap Widens for SaaS Company Multiples

They found that the gap between private and public company valuations has grown from 30% to 50%:

SaaS Capital did not report on any definitive reasons why the gap had grown from 30% to over 50%. They have promised more details in upcoming research.

Why Are Private SaaS Companies Valued Less Than Public SaaS Companies?

There are a lot of reasons why private companies are valued less than public companies. In general, there are three major factors and six minor factors:

Major Private SaaS Company Discount Factors

- Liquid equity

- Audited Financials

- SOX 404 certifications

Minor Private Company Discount Factors

- Revenue Scale & Growth Rate

- Market Size

- Revenue Retention Rate

- Gross Margin & Revenue Mix

- Customer Acquisition Efficiency

- Profitability

Major Discount Factors

There are three major factors that collectively account for the majority of valuation discounts private SaaS companies face in comparison to their public peers. These factors include:

Liquid Equity

The single largest factor is that public SaaS company’s stock/equity is traded and priced every business day. The market takes into consideration everything it knows about a company and sets a price. People can buy or sell every day. Privately held SaaS companies’ equity is not publicly traded. It is only priced when a new round of funding is raised or a private placement is made. Investors impose a steep discount for private versus public companies.

Audited Financials

Public companies are required to have their financial statements audited, and an opinion rendered by the auditor. Audited financials provide investors with clarity and consistency.

Any privately held SaaS companies do not have their financial statements audited. This can cause problems with investors and potential acquirers. These organizations must conduct their own diligence. Many privately held firms ‘bury’ owner’s expenses in their P&L. Examples include non-business travel expenses, personal legal services, rent/lease payments on non-business-related real estate and equipment. I once found that a prospective acquisition candidate had inflated their revenues so that a credit card processor wouldn’t fine them for excessive chargebacks. They used relatives’ credit cards to pay for monthly services that were subsequently refunded to them.

SOX 404 Certifications

The Enron disaster spurred the passage of the Sarbanes Oxley Act in 2002.

The SOX Act, passed in 2002, affects all companies, regardless of industry. It addresses corporate governance and financial practices with a particular focus on records. SOX includes 11 titles with the primary audit-related sections being 302, 401, 404, 409, and 802. 302 – Requires periodic statutory financial reports. The reports must present an honest accounting of a firm’s financial stability, any fraud incidents, ineffective control methods, and changes/improvements to internal controls.

- 401 – Addresses full financial disclosures, including liabilities, transactions, and accounting practices.

- 404 – Analyzes internal controls and financial reporting procedures.

- 409 – Requires companies to inform the public of changes in financial operations or significant changes in the company’s financial position.

- 802 – Addresses fraudulent documentation (e.g., falsifying records) and consequent penalties

Every time a company makes a public filing containing financial statements the Chief Executive Officer and the Chief Accounting Officer have to personally certify the adequacy of financial controls and the accuracy of financial statements. These certifications are powerful motivation.

Private SaaS companies do not have to make these disclosures and certifications

Minor Discount Factors

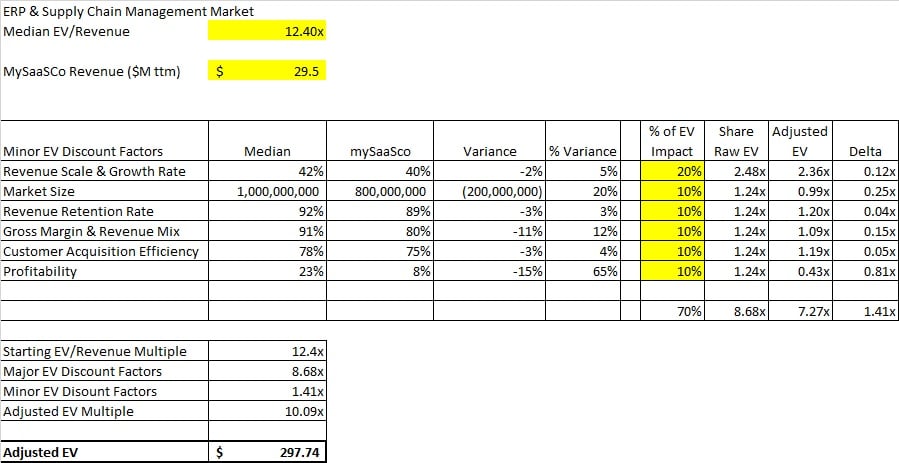

There are six common minor factors that are applied to private SaaS companies. Usually they are presented in context of the median performance in their market segment. Consider the following:

This is a typical model that investors and acquirers use to assess a potential investment. A multi-factor model like this looks at a company from multiple perspectives. The more fact-based perspectives, the better the results will be. You can download this model here. Cells that are highlighted in yellow can be changed.

Revenue Size & Growth Rate

Investors place a premium on revenue growth rates and scale of total revenue. Investors like to see startups execute a “Triple-Triple-Double-Double-Double”. One a firm reaches product-market fit and $2 million in ARR they should focus on tripling the revenue to $6M and tripling again to $18M, the execute three years of doubling revenue ($36M, $72M, & $144M). This is the performance of a unicorn. Not every company can be a unicorn – look at the median revenue growth rate in your market and assess how your growth rate stacks up.

Market Size

The larger the market, the better. Investors are long past the “if we can get 2% of a billion market we’d be great” market sizing. You need to be able to intelligently discuss Total Available Market (TAM), Serviceable Addressable Market (SAM), & Service Obtainable Market (SOM).

Revenue Retention Rate

Revenue retention is a critical indicator of the health and longevity of a business.

Net dollar retention is a common metric. It measures what percent of revenue you retained from the prior year after accounting for upgrades, downgrades, and churn. Formulaically it’s beginning of period revenue + upgrades — downgrades — churn all divided by beginning of period revenue. If that formula yields a number greater than 100%, then growth from your existing customer base more than offset any losses from that customer base.

Similarly, net retention below 100% means churn and downgrades were greater than any growth you enjoyed from the expansion of existing customers. If that’s the case, you need to take action with Customer Success and Customer Support to try and reverse the trend.

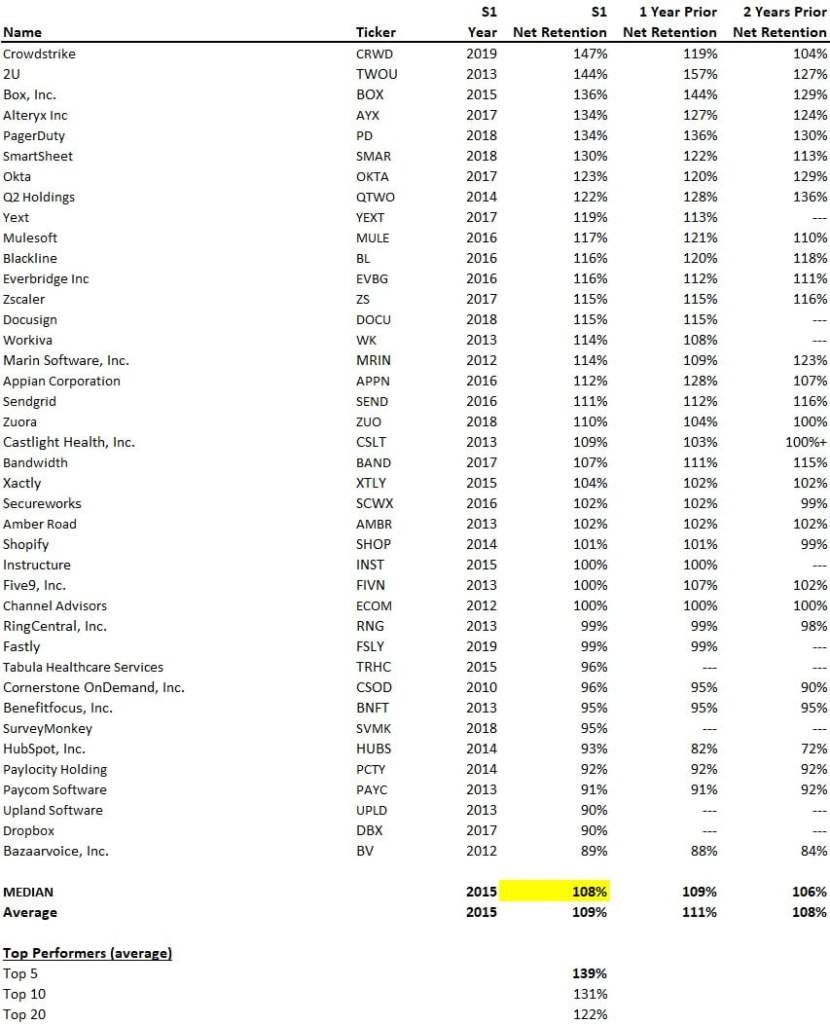

Here is a list of public companies and what their retention rates are like:

The valuation of your firm will depend on how your retention rate compares to the median of your industry.

Gross Margin & Revenue Mix

Gross Margin is a key metric for SaaS companies:

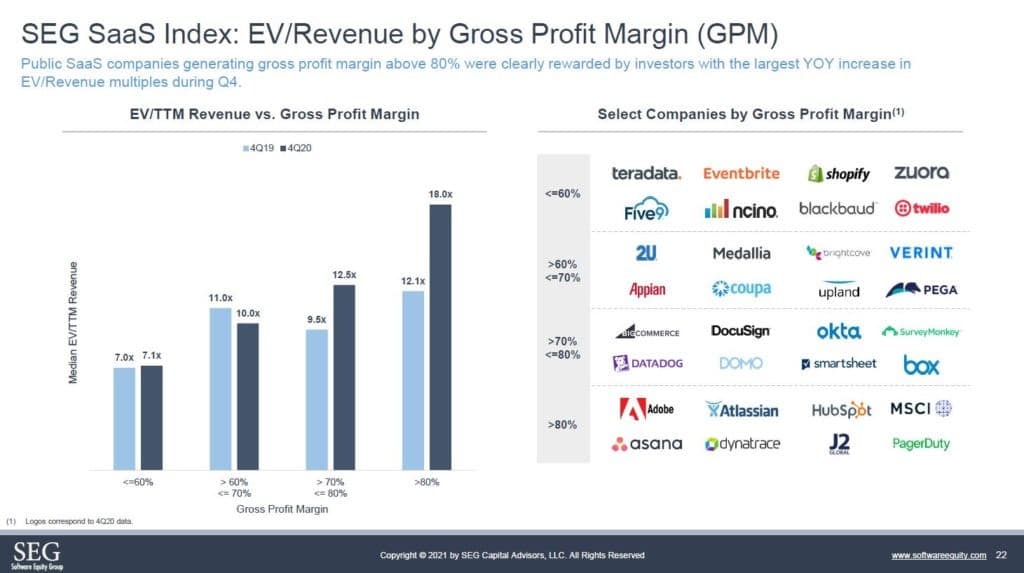

Gross margin is a very important metric Software Equity Group looks at when evaluating a business. Based on our experience, a good benchmark is over 75%. Typically, most privately held SaaS businesses we work with have gross margins in the range of 70% to 85%. Anything below 70% begins to raise a red flag, requiring additional analysis. It is important to note we occasionally see SaaS businesses incorporating on-going services into their business models. While this causes us to look deeper into the company’s scalability, we often see a favorable tradeoff resulting in exceptionally strong gross retention and net retention.

Higher than median gross margins are correlated with higher Enterprise Values:

Customer Acquisition Efficiency

As noted in a white paper by SaaS Capital

Profitability

Both investors and strategic buyers are typically looking to continue growing a SaaS business by deploying more capital for sales and marketing. How efficiently the business converts that spending into new customers is highly relevant to both projected future cash flows at maturity, and the amount of capital required to get there. Companies with high customer acquisition costs (CAC) need more capital to grow, and thereby, diminish overall returns whether the buyer is a VC, a corporation, or a public stockholder.

There are many ways to measure the CAC ratio, and for this analysis, we will keep it simple:

CAC Ratio = New ARR from new customers ÷ sales and marketing spend to acquire those customers

In English, how much in annual revenue is generated for each dollar invested in sales and marketing?

Our 2019 survey of SaaS companies yielded a median CAC ratio of .78. This means that each dollar of sales and marketing spend generated 78 cents of annual recurring revenue. This can also be thought of as a monthly payback period of 15.4 months (12 months ÷ .78).

SaaS Capital

It is important for a business to be self-sustaining. Private SaaS firms that are not profitable will take a major valuation discount as investors/acquirers assess how much capital is needed to sustain operations. The median profitability in your industry is a function of how advanced your market is. In early-stage markets, profitability is not rewarded – the profits could be reinvested to drive more growth/revenue. In mid-to-late stage markets (Moore’s Early Majority to Laggards) profitability becomes more important.

Summary

Private SaaS companies have always been valued less than their public company peers. SaaS Capital recently reported that the gap had grown to almost 50%. While SaaS valuations have moderated a bit in 2021, they still stand at near all-time highs. As the Software Equity Group has reported, median public company SaaS EV/Revenue valuations were almost 15x at the end of Q2 2021. Some segments were dramatically higher, like DevOps & I.T. Management at 22x. Leading companies like Zoom and Shopify are valued at over 50x EV/Revenue. There are many factors that account for private companies being valued less than public companies: illiquid equity, no public/audited financials, no SarBox certifications.