With SaaS Valuations Returning to 2018 Levels, Is Now the Time to Buy?

Surprisingly, The Answer May Be No

Baron Rothschild, an 18th-century British nobleman and member of the Rothschild banking family, is credited with saying that “the time to buy is when there’s blood in the streets.” In late 2022 it is clear that the SaaS market is in trouble. The Nasdaq is off over 34%. Median Enterprise Value/Revenue valuations are off 58% in comparison to their peak in 2021. Many companies might consider now to be a good time to jump into the M&A game. Experience has shown, however, that a well-reasoned M&A strategy is required for success

In this article we will talk about:

- 2022 SaaS Valuation Trends

- Can You Buy Your Way Out of a Problem?

- Acquisitions Can Be Transformative

- You Need an M&A Strategy

- Acquisition Types

- Acquisition Constraints

- Acquisition Currency

- Return Requirements

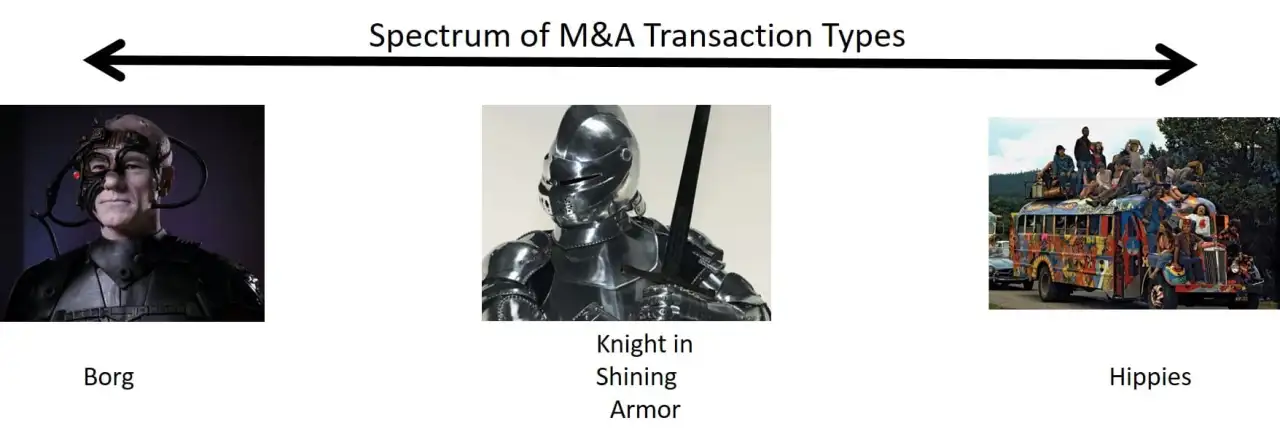

- Acquisition Styles

- The Borg

- The Hippies

- Knights in Shining Armor

2022 SaaS Valuation Trends

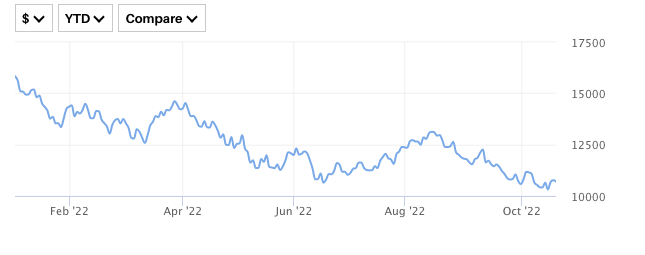

There is no doubt that 2022 has been tough on SaaS valuations. By October, the Nasdaq is off 34% since the start of the year:

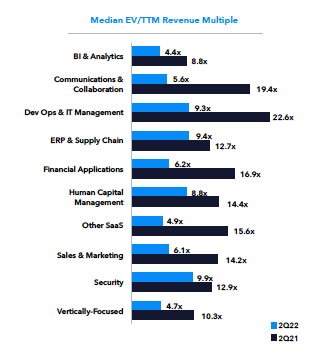

In August, the Software Equity Group published a great study Staying Power: A Dive into Software M&A Trends in 2022. It showed that the median Enterprise Value/Revenue valuation for SaaS firms in the SEG SaaS Index had declined 58% in comparison to their peak in 2021:

Staying Power: A Dive into Software M&A Trends in 2022

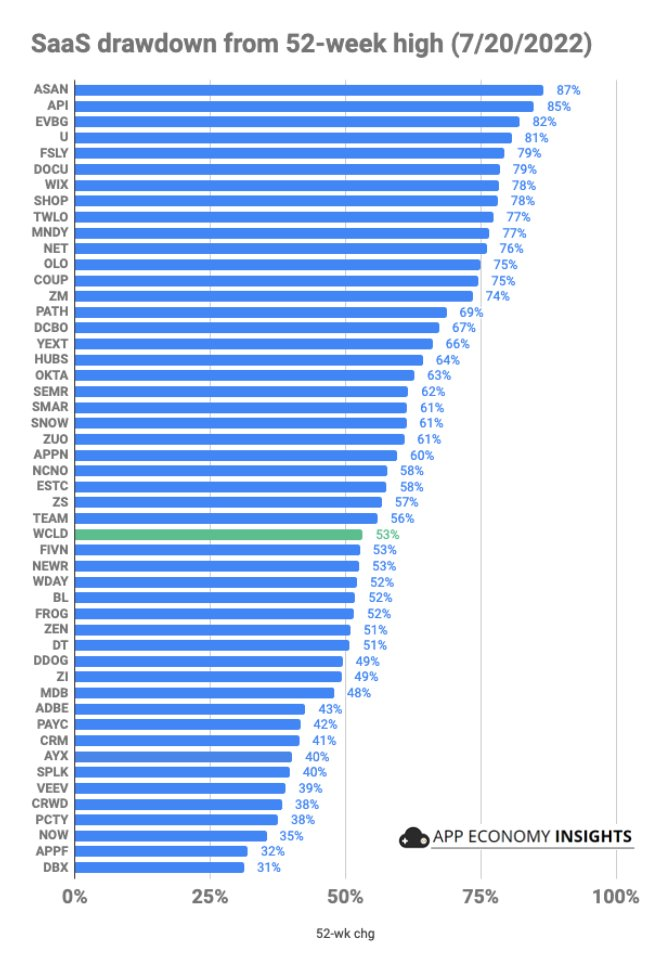

Some SaaS market segments have seen even greater declines in valuation:

Staying Power: A Dive into Software M&A Trends in 2022

Some previous high fliers like Twilio (↓73.6%), Cloudfare (↓53.4%) and Confluent (↓54.1%) are suddenly much more affordable than before.

Private equity investors have shifted what they consider to be important:

Staying Power: A Dive into Software M&A Trends in 2022

Revenue stability and persistence, along with profitability are much more important in 2022 than in 2021.

Can You Buy Your Way Out of a Problem?

As the third quarter earnings season approaches you can expect to see even more signs of financial stress in the SaaS market. Many companies will consider using M&A as a tactic to overcome weaknesses in their core business. Current valuation trends make this an attractive option.

Purchased revenue growth is a time-proven strategy. Oracle is a classic example of a serial acquirer. Oracle has acquired over 140 firms. Oracle’s acquisition of healthcare IT provider Cerner will increase total revenues by almost 14% ($5,8 billion) and propel Oracle to over $50 billion in revenue this year. Other Oracle acquisitions have not worked out as well – like Sun Microsystems in 2010.

In the late 1990s, I was a senior corporate development executive in Sterling Software’s Application Development tools group. In 1998 we were struggling, the move from client/server and mainframe applications to SaaS applications was cutting dramatically into our revenue growth. The CEO, Sterling Williams, directed us to acquire a struggling application tools vendor, Cayenne Software. The firm was doing almost $50 million in revenue, but because of their broken finances we were able to acquire them for only $11 million – a 0.25x Enterprise Value/Revenue valuation. We spent an additional $22 million to restructure Cayenne. We were able to add over $45 million in revenue and improve the acquired business to over 23% operating profit margin.

Acquisitions Can Be Transformative

A quintessential example is Google’s 2006 $1.65 billion acquisition of YouTube. YouTube had been founded a year and a half before and had raised $85 million in venture capital. They had 65 employees but controlled 46% of the video streaming market. Google had been struggling in that market with Google Video. The YouTube acquisition was a huge bet, but it enabled Google to dominate the video streaming market. In 2019 YouTube had grown into a $28 billion business in 2021.

A more recent example is Vista Equity Partners’acquisition and sale of Marketo. Marketo was founded in 2006 by a group of ex-Epiphany executives. It went public in 2013 and was struggling in 2016 when its revenue growth rate declined by 50%. Marketo was executing a growth at any cost strategy and had posted -$50 million in EBITDA. They were acquired by Vista Equity for $1.79B – a 62% premium over its prior closing price. Adobe acquired Marketo from Vista in August 2018 for $4.75B – a hefty return and Vista’s single largest exit to date.

Vista brought in a new CEO for Marketo – SAP executive Steve Lucas, who had significant experience in growing enterprise software businesses. When Vista buys a company, all employees and recruits are required to take a personality-and-aptitude test, like one first developed by IBM. The hour-long test assesses technical and social skills and attempts to gauge analytical and leadership potential. Vista also leveraged its Vista Standard Operating Procedures aka their secret sauce. It is basically a guidebook for growing software companies. Vista also leveraged its boot camp training programs. Boot camps train employees, not just for two weeks but for six to nine months. In the past three years, Vista has put 12,000 new hires through these boot camps. They start by giving employees the big picture: how the Vista company makes money and the way customers use its products. The focus later shifts to specific corporate roles.

The results were dramatic. Marketo went from ~$50M in 2016 to EBITDA positive in 2017 to a $4.75 billion exit in 2018. Instead of growth at any cost, it was growth with a purpose and focus.

You Need an M&A Strategy

Successful acquirers always have a strategy that underlies their M&A activity. The strategy encompasses why they undertake an acquisition, the constraints that govern potential acquisitions, their style for conducting the acquisition, and integrating the acquired company into their company.

Acquisition Types

There are three broad reasons why a company undertakes an acquisition:

- Consolidation. Acquire companies in the same core market to gain market share and dominance. Consolidation acquisitions bring increased revenue (aka purchased revenue) and profitability. In the 1990s I led the consolidation of the enterprise application tools market with Sterling Software’s acquisition of KnowledgeWare, Texas Instruments Sofware, Synon, and Cayenne.

- Acceleration. Acquire a business to accelerate your product roadmap. Instead of building a product organically, buy an existing product to get to market sooner at a lower risk. Google’s acquisition of YouTube is a classic example of this. Another company I worked with last year, Bigtincan Holdings (ASX:BTH) executed a strategy of several small technology acquisitions and one major acquisition to accelerate the completion of their long-term product roadmap by years.

- Diversification. Diversification acquisitions move a company into new markets, like Oracle’s acquisition of Cerner.

Acquisition Constraints

Constraints are factors that limit a company’s ability to do a specific acquisition. Two common constraints include acquisition currency and return on investment requirements.

Acquisition currency refers to how an acquirer will pay for an acquisition. This can include stock, cash, and new debt. The willingness of a target to accept stock is dependent on many things. Is the acquirer public? If private when will they be able to monetize the stock? Does the acquirer have shareholder approval to issue new stock? Cash is pretty obvious, does the acquirer have liquid funds available? Many acquirers also use new debt to fund an acquisition. This often puts additional constraints on the deal, such as minimum revenue, profitability, and cash flow targets.

Another common constraint involves return expectations. What are the minimum improvements in valuation (enterprise value) and when must they be achieved? In the early 2000s I worked for a number of private equity-backed SaaS companies. One sponsor had a simple formula – they expected a 3x to 5x return on their investment within three years. When I worked for Sterling Software they expected that each acquisition would be accretive to earnings per share in year one.

Not all acquirers are bound by such draconian constraints. Many of the most successful acquisitions were dilutive to EPS initially. It is important to understand your company’s constraints before launching an M&A initiative.

Acquisition Style

There are many approaches acquirers use for M&A. Computer Associates had one approach that many considered to be harsh. Others had a friendlier, kinder approach like the style employed by Google and Apple. Acquisition styles can be grouped into three cases– what I call the Borg, Knight in Shining Armor, and the Hippie approach. In the spirit of full disclosure, I was an M&A exec for three enterprise software firms. I led three Borg-like acquisitions, one Hippie acquisition, and 11 Borg-like divestitures.

The Borg

The Borg approach was pioneered in the late 80’s and 90’s. Example acquirers included Computer Associates, Platinum Technologies, and Sterling Software. This approach was characterized by:

- Complete takeover of a company’s operations.

- Significant headcount reductions and office closures

- Significant reduction in new product development and often customer service

- Financial engineering (junk bond style debt to finance acquisition)

- Annihilation of acquired company’s brand an identity

- Replacement of acquired company’s management with exes and managers from acquirer

- Primary focus was on increasing profitability, EPS, and Enterprise Value.

In the 1980s and 1990s these firms sought out what they considered to be undervalued companies and acquired and subsequently restructured them. Often these firms had struggling stock prices, poor financial performance, and potentially liquidity problems. They could be acquired at a discount to their intrinsic value and restructured into profitable enterprises. Their approach was a precursor of the infamous Chainsaw Al Dunlap. Many of the companies acquired in this period had been successful at one time, but had fallen on hard times due to changing market conditions (client/server and Internet revolutions), investments in new products that ultimately failed, or botched acquisitions.

The primary driver of these acquisitions was the growth of shareholder value. Most of the senior executives of firms like CA, Platinum, & Sterling had a significant portion of their personal wealth tied up in company stock and stock options. Their business model succeeded as long as they could find undervalued companies that they could restructure to profitability, they could drive up the value of their stock and personal fortunes. The Dotcom bubble ended its business model with the stratospheric valuations of the late 1990s and the year 2000.

The Hippies

At the other end of the spectrum are the Hippie acquisitions. These deals, often done by West Coast software firms, were focused primarily on the products and not profits. Hippie deals were characterized by very high valuations and focused on products, not the financial characteristics of the business. Typical acquirers were the FAANG companies –Facebook, Apple, Amazon, Netflix, and Google. A quintessential example is Google’s 2006 $1.65 billion acquisition of YouTube. YouTube had been founded a year and a half before and had raised $85 million in venture capital. They had 65 employees, but controlled 46% of the video streaming market. Google had been struggling in that market with Google Video. The YouTube acquisition was a huge bet, but it enabled Google to dominate the video streaming market. In 2019 YouTube had grown into a $15 billion business.

The Hippie approach is characterized by:

- Extremely high valuations, often paid for with stock (versus cash/debt for Borg acquisitions)

- Primarily focused on products versus revenues/profits

- Acquired companies left intact, often as a strategic business unit of acquirer

- Little to no headcount reductions

- Focus on integrating/leveraging technology and human capital

- Significant resources invested to accelerate growth

- Significant growth opportunities for employees of acquired companies to move into new positions in the acquirer’s company

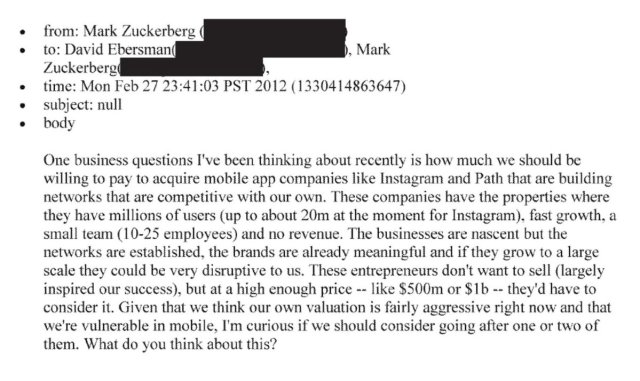

The following is an email exchange between Mark Zuckerberg and David Ebersman Facebook’s CFO around the time of the Instagram acquisition. It is a classic example of how Hippie-style acquirers think and what they value the most:

Knights in Shining Armor

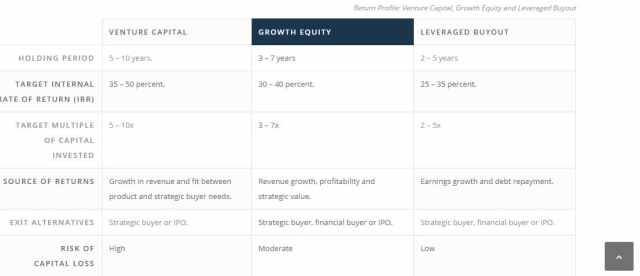

The Knights in Shining Armor approach is a hybrid of the Borg and Hippie approaches to Tech M&A. It is often associated with Growth Equity. Growth equity investors (private equity firms) focus on creating value through profitable revenue growth within their portfolio companies. Vista Equity Partners’ acquisition and subsequent sale of Marketo is often cited as a prime example of this strategy. The following table illustrates the differences between Venture Capital, Growth Equity, and LBOs:

The Knight in Shining Armor approach is characterized by:

- Established companies that have fallen on hard times, often public companies that have taken a stumble

- Premiums above current market valuation often paid

- Deals most often involve equity and little debt

- Restructuring to achieve profitability

- Replacement of senior executives and key managers is common

- Introduction of best practices from investors other portfolio companies

- Primary focus is on changing strategies and execution to focus on sustainable revenue growth

- Goal is to significantly grow enterprise value

- Exit in 3 to 5 years, often to strategic acquirer

Vista Equity’s acquisition of Market for $1.8 billion and its subsequent sale to Adobe three years later for $4.75 billion is often cited as a classic example of successful growth equity investing.

Marketo was a provider of marketing automation solutions. It targeted the entire spectrum of enterprises – SMB’s, mid-market companies, and large scale enterprises. Marketo went public in 2013 and by early 2016 their revenue growth had slowed considerably and their stock price had significantly declined. Marketo was trying to fight a battle on too many fronts – from SMBs to large scale enterprises. Their competitors, like Hubspot (SMBs) and Salesforce (enterprises). They were consistently unprofitable. In the Spring of 2016 management and the board began a process to sell the company to a strategic acquirer. Vista offered a 67% premium to the then current stock price and beat out six other bidders.

Vista implemented a number of Borg-like actions to reduce Marketo’s expense base and return the company to profitability. They deployed an updated version Vista playbook which focuses on leveraging best practices of their portfolio companies. On the growth side of the equation, Vista replaced the founding CEO of Marketo, Phil Fernandez, who had been running the company for a decade. His replacement, SAP executive Steve Lucas, had more experience with reinvigorating the growth of a software business. The company revamped its product development and decided to go after large deals in the enterprise space, where retention rates are higher and upselling is easier. In 2017, Marketo’s revenue grew to about $321 million from $209 million in 2015, and by the start of 2018 the company was generating positive EBITDA; it was posting -$50 million of EBITDA in the 12 months before the Vista acquisition. In August 2018 Vista announced the sale of the revamped Marketo to Adobe for $4.75 billion. They netted almost $3 billion in a little over two years.