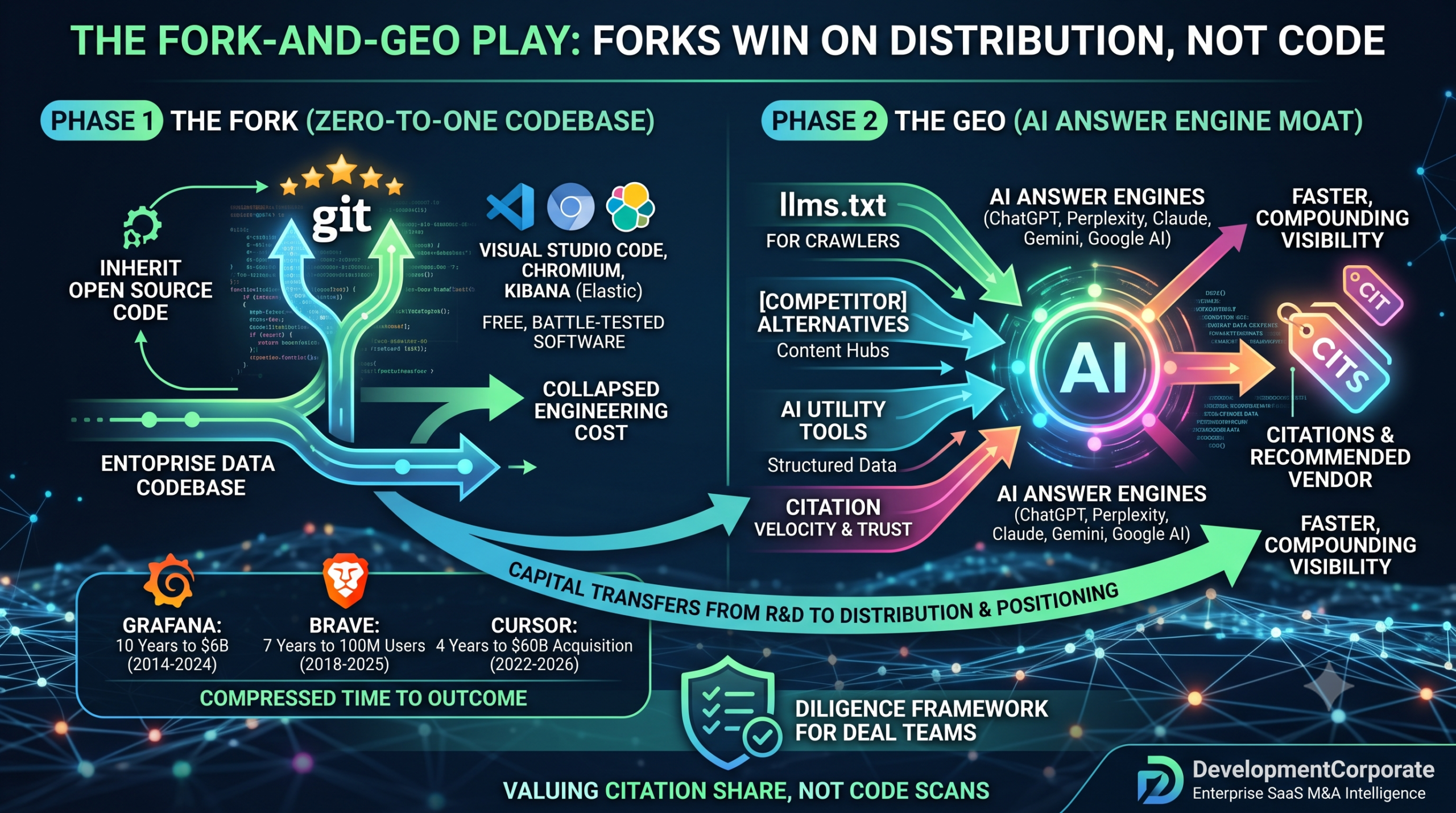

The Fork-and-GEO Play: How Commercial Forks Win on Distribution, Not Code

The fork-and-GEO play is quietly rewriting how software companies get built — and how they should be diligenced. In June 2026, SpaceX agreed to acquire Anysphere, maker of the Cursor AI code editor, for $60 billion in the largest acquisition of a venture-backed startup ever recorded. Cursor began life as a fork of Microsoft’s open-source VS Code. Brave, at 100 million monthly users, runs on Google’s Chromium. Grafana Labs, valued at $6 billion, started as a rejected pull request to Elastic’s Kibana. Three of the most valuable software franchises of the decade were built on code their founders did not write.

The consensus reading of these stories is that they are engineering triumphs. That reading is popular, intuitive, and wrong. The code was free. What these companies built — and what acquirers actually paid for — was distribution: brand, channel, trust, and workflow lock-in layered on top of a commoditized codebase. And in 2026, the cheapest, fastest-compounding distribution channel available to a fork is Generative Engine Optimization (GEO) — engineering a brand’s visibility inside AI answer engines like ChatGPT, Perplexity, Claude, and Google’s AI Overviews. We call the combined pattern the fork-and-GEO play, and it has direct consequences for how investors screen targets, how founders defend categories, and how deal teams run technical diligence.

“The engineering was inherited. The entire bet is distribution.”

What Is the Fork-and-GEO Play?

Fork-and-GEO is a go-to-market pattern with two moving parts. First, an operator takes a permissively or copyleft-licensed open-source codebase — often one with thousands of GitHub stars and years of accumulated bug fixes — and rebrands it as a commercial product. Second, rather than competing on engineering, the operator competes on distribution, with generative engine optimization as the spearhead channel.

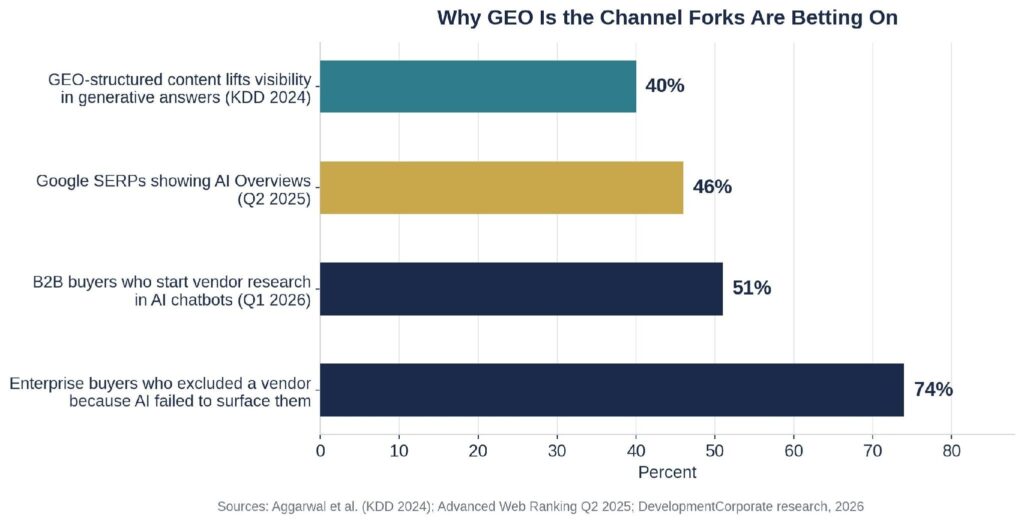

The underlying insight is old: open source commoditizes code, so the durable moat is distribution, trust, and workflow lock-in. What is new is the channel. AI assistants now mediate a growing share of software discovery, and as we documented in The Answer Economy, 51% of B2B buyers now start vendor research in AI chatbots rather than Google. The sites those engines cite win the category.

The mechanics of a modern fork-and-GEO launch are remarkably consistent: llms.txt files that explicitly invite AI crawlers; programmatic “[competitor] alternative” landing pages targeting high-intent brand queries; persona-segmented content hubs produced at AI speed; free utility tools for query capture; and affiliate programs engineered for third-party citation velocity. The academic grounding traces to the 2024 KDD paper “GEO: Generative Engine Optimization” by Aggarwal et al., which showed that content structured for AI citation can lift visibility in generative answers by 40% or more.

Figure 1: The distribution battleground has moved into AI answer engines. Sources: Aggarwal et al. (KDD 2024); Advanced Web Ranking; DevelopmentCorporate research.

Why the Fork-and-GEO Model Works — and Where It Breaks

Four structural forces make the model attractive, and one makes it dangerous.

- Zero-to-one engineering cost collapses. A proven, battle-tested codebase is free. Capital that would have gone to R&D goes to positioning and channel instead. In a market where AI-powered clean-room cloning has pushed the marginal cost of replicating open code toward zero, this asymmetry only widens.

- Forks can out-position the original. Open-source maintainers are usually engineers, not marketers. A fork that invests in brand, a legal entity, commercial support, and AI-search visibility can capture the commercial demand the upstream project created but never monetized.

- AI search resets the ranking game. Answer engines reward structured, citable, comparison-rich content — which a new entrant can manufacture faster than an incumbent can defend, especially for “alternative to X” queries. As our AI Dark Funnel research found, 74% of enterprise buyers have excluded a vendor simply because AI failed to surface them. Incumbency in Google does not transfer automatically.

- Citation authority compounds from a standing start. Our LLM training data analysis showed that ungated content can achieve confirmed citation status in search-first engines like Perplexity within days of publication — a timeline with no analog in traditional SEO.

The break point is equally structural. Copyleft licenses — GPL and AGPL — impose source-disclosure obligations on distributed binaries. Upstream communities can generate reputational backlash. And a distribution moat must eventually convert into product differentiation, or the next fork simply runs the same play against you. Code that was free to take is free to take again.

Anatomy of a Fork-and-GEO Launch: The Unspoken Teardown

The clearest way to see the pattern is at the micro end, where the machinery is fully visible. Unspoken is a commercial Mac dictation app derived from VoiceInk, a GPL v3 open-source project with roughly 5,300 GitHub stars. The Unspoken domain was registered in January 2026. By launch, it had shipped a complete GEO apparatus: an llms.txt file inviting AI crawlers, competitor-alternative landing pages in two languages, ten persona-segmented content hubs, and free utility tools for query capture — all before the product had any organic reputation whatsoever.

Read that sequence carefully, because it inverts twenty years of go-to-market orthodoxy. The traditional playbook builds product, earns users, and accretes search authority over years. The fork-and-GEO playbook inherits the product on day zero and manufactures the citation surface before the first customer arrives. The content infrastructure is not marketing for the product. The content infrastructure is the product bet.

This is also where diligence risk concentrates. A GPL v3 derivative distributed as a commercial binary carries source-disclosure obligations. A fork with no public repository and no written source offer is carrying legal exposure that can surface mid-transaction — precisely the failure mode we documented in the Delve whistleblower files, where an open-source fork marketed as proprietary IP escalated from a compliance question into investor-fraud allegations.

Three Companies That Proved the Distribution Thesis at Scale

GEO as a named discipline is barely two years old, but the underlying play — fork the code, win on distribution — has already produced companies worth billions. The three cases below span three eras of the channel: developer word-of-mouth, privacy positioning against search incumbents, and community-led content. Each one monetized a codebase it did not originate.

Cursor (Anysphere): Fork of VS Code → $60B Acquisition Agreement

Four MIT students forked Microsoft’s MIT-licensed VS Code in 2022 to build an AI-native editor. The fork bought architectural control — inline diffs, shadow workspaces, terminal interception — that plugin-based rivals like GitHub Copilot could not match. Distribution was pure bottoms-up: developer word-of-mouth and $20/month individual subscriptions converting into enterprise contracts without a traditional sales motion.

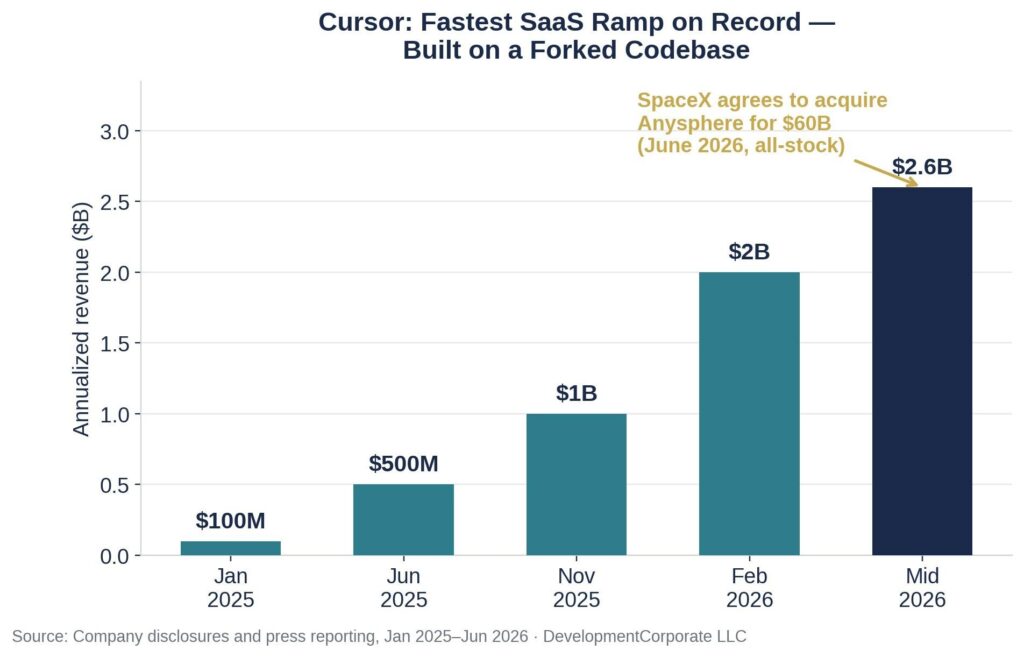

The result is the fastest SaaS ramp on record: $100M ARR by January 2025, $1B by November 2025, $2B by February 2026, and roughly $2.6B annualized by mid-year, with Cursor reportedly running on developer machines at about half the Fortune 500. After a $29.3B Series D in late 2025, SpaceX agreed in June 2026 to acquire Anysphere for $60 billion in an all-stock deal expected to close in Q3 2026, pending regulatory approval. The strategic kernel is pure fork-and-distribution: the ongoing “tax” of merging upstream changes bought architectural freedom, while the code Cursor inherited was free.

Figure 2: Cursor’s revenue ramp, January 2025 to mid-2026. The codebase was inherited; the distribution was built. Sources: company disclosures and press reporting.

Brave: Fork of Chromium → 100M Monthly Active Users

Founded by Mozilla co-founder Brendan Eich, Brave moved onto Google’s open-source Chromium codebase in 2018, inheriting the world’s dominant browser engine and full Chrome extension compatibility at zero cost. The entire company is the distribution layer: a privacy-first brand positioned directly against its own upstream, a built-in ad blocker as the wedge, its own search engine and ad network for monetization, and relentless comparison content targeting “Chrome alternative” intent.

In October 2025, Brave announced it had passed 101 million monthly active users and 42 million daily actives — built on a codebase it did not write, differentiated almost entirely by positioning, defaults, and trust. Note the GEO-native detail: Brave’s public transparency dashboard is itself a distribution asset — a citable, crawlable proof point that AI answer engines routinely surface when users ask about private browsers.

Grafana Labs: Fork of Kibana → $6B Valuation, $400M ARR

In 2013, Swedish developer Torkel Ödegaard submitted a pull request adding Graphite support to Elastic’s Kibana. When it was rejected, he forked Kibana 3’s UI and released Grafana in January 2014. The fork went viral in the DevOps community, and Grafana Labs scaled through the canonical open-source distribution playbook: community-led adoption past 25 million users, content and documentation as the marketing engine, and monetization of roughly 1% of users through cloud and enterprise tiers.

By 2024 it reached a $6 billion valuation on a $270M Series D extension led by Lightspeed with Alphabet’s CapitalG, and by late 2025 reported $400M in annualized revenue with customers including Nvidia, Anthropic, and Uber. Grafana is the cleanest proof that a rejected pull request plus superior distribution can out-scale the original: as an independent brand, it now dwarfs Kibana.

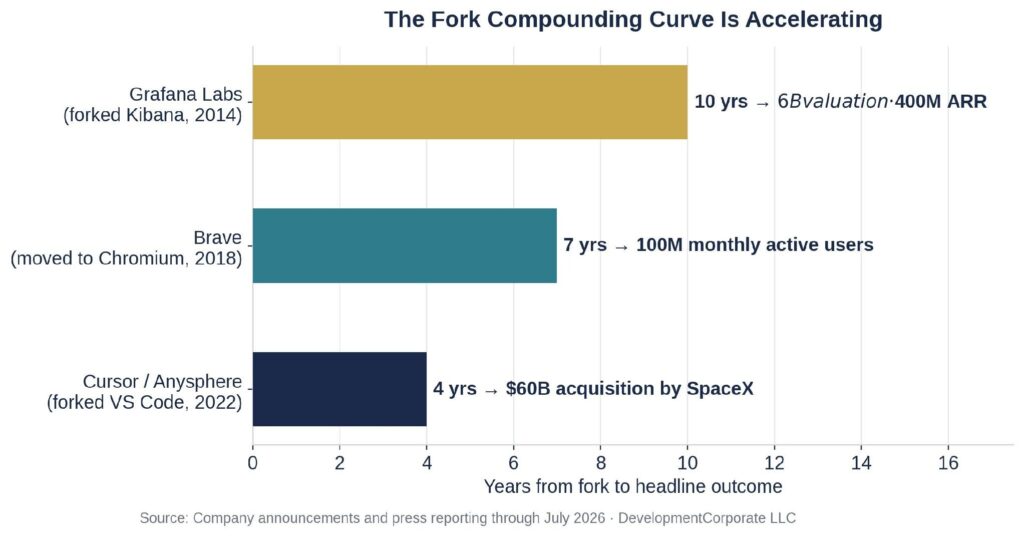

Figure 3: Time from fork to headline outcome is compressing — from ten years (Grafana) to four (Cursor). GEO compresses it further.

“Grafana took ten years to turn a fork into $6 billion. Cursor took four to turn one into $60 billion. The compression is the story.”

The Fork-and-GEO Diligence Framework: Five Questions for Deal Teams

Standard technical diligence — code scans, architecture review, security posture — evaluates a fork-based target as if its value lived in the code. As we argued in our analysis of the a16z SaaS Moat Scorecard, code was never the moat. For fork-and-GEO targets, deal teams should add five questions to the standard M&A due diligence checklist:

- 1. Is the license chain clean? Identify the upstream project and license. GPL/AGPL derivatives distributed as binaries require a source offer; verify one exists in writing. A fork with no public repo, no attribution, and active denial of its origins is a representation risk, not a technical footnote.

- 2. What is the upstream merge tax? Quantify the engineering cost of tracking upstream releases. Cursor paid it willingly for architectural freedom; a thinly staffed fork that has silently stopped merging is accumulating security debt against every upstream CVE.

- 3. What is the citation share? Run the target’s category queries through ChatGPT, Perplexity, Gemini, and Claude and measure how often the target — versus the upstream project or rival forks — appears in the answer. This is the fork’s actual moat, and as we detailed in The AI Search Visibility Audit Your Deal Room Is Missing, no standard deal room process measures it today.

- 4. Where does the citation authority live? Distinguish owned citation surface (the target’s ungated content, tools, documentation) from rented surface (affiliates, listicles, press). Owned surface transfers cleanly in a transaction; rented surface decays. Remember that the channels executives assume matter most — Gartner, gated content — are invisible to every major LLM.

- 5. Is there evidence of graduation? The model converts only if distribution buys time to differentiate. Cursor built its own inference model. Brave built a search engine and ad network. Grafana built the LGTM observability stack. A fork that never graduates beyond the upstream codebase remains one fork away from being commoditized itself.

| FOR PE / VC INVESTORSScreen fork-based targets on channel machinery, not feature lists. Price the license chain and the upstream merge tax as liabilities; price owned AI citation share as a transferable asset. A target with dominant citation share in its category queries is carrying an unpriced CAC advantage — and one with none is carrying an unpriced CAC headwind. |

| FOR SAAS FOUNDERS APPROACHING EXITIf your product is a fork, document the license compliance story before a buyer’s counsel finds the gaps. If your product is the upstream, your commercial demand is being harvested by forks with better GEO — audit your own citation share quarterly. Either way, enter the process with a graduation narrative: what you built that the codebase did not give you. |

| FOR ENTERPRISE CTOs / CPOsWhen evaluating a vendor built on an open-source fork, ask for the source offer and the upstream merge cadence in the security questionnaire. A fork that lags upstream by two major versions is a patch-latency risk. And recognize that the vendor an AI assistant recommended to your team may simply be the one with the best llms.txt — not the best engineering. |

Takeaways: The Fork-and-GEO Play for Founders and Investors

- In categories where the code is open, the moat is distribution and trust. Evaluate fork-based competitors on their channel machinery, not their feature list.

- GEO is the cheapest distribution channel a fork has ever had. A six-month-old domain can now contest AI-answer citations for a category’s highest-intent queries. Track citation share in ChatGPT and Perplexity answers the way you once tracked page-one rankings.

- Diligence the license. GPL/AGPL forks carry source-disclosure obligations; a fork with no public repo and no source offer is carrying legal risk that can surface mid-transaction.

- The model converts only if distribution buys time to differentiate. Forks that never graduate beyond the upstream codebase remain one fork away from being commoditized themselves.

The Bottom Line

The fork-and-GEO play is not a fringe tactic. It is the logical endpoint of two converging forces: open source driving the marginal cost of proven code toward zero, and AI answer engines resetting distribution to a game a well-executed newcomer can win. Cursor, Brave, and Grafana proved the fork half of the thesis at billion-dollar scale. Operators like Unspoken are now running the GEO half from day zero. The market is pricing these companies on their code. The smart money will price them on their channel.

DevelopmentCorporate advises enterprise SaaS companies and investors on exit strategy, acquisition diligence, and valuation positioning — including AI search visibility assessment for both buy-side screening and pre-exit preparation. If you are evaluating a fork-based target or preparing a fork-based company for a transaction, contact us for a confidential discussion.

Reference Links

- GEO: Generative Engine Optimization (Aggarwal et al., KDD 2024)

- llms.txt specification

- VoiceInk (GPL v3 upstream of Unspoken)

- Unspoken llms.txt

- VS Code repository (MIT)

- Cursor

- SpaceX–Anysphere acquisition coverage (Yahoo Finance)

- Chromium project

- Brave 100M MAU announcement

- Brave transparency data

- Grafana repository (AGPL v3)

- Grafana Labs

- GNU GPL v3 license text

Figures as reported through July 2026: Cursor/Anysphere revenue milestones and the SpaceX acquisition agreement per Reuters, Yahoo Finance, and Tech Funding News coverage (deal expected to close Q3 2026, pending regulatory approval); Brave MAU per company announcement (October 2025); Grafana Labs valuation and ARR per TechCrunch (August 2024) and Forbes (September 2025) reporting. Licensing observations are informational, not legal advice.