2026 SaaS Benchmarks: The AI Monetization Gap M&A Buyers Are Missing

The 2026 SaaS benchmarks just published by Benchmarkit tell a story most operators will read backwards. On the surface, it’s a recovery: CAC payback improved 11%, Rule of 40 posted its best single-year gain in five years, and ARR per employee jumped 17%. Boards will celebrate. Bankers will use it to justify multiples. And almost everyone will miss the fact that the same 342-company dataset shows gross revenue retention falling four points, growth decelerating for the fourth straight year, and two-thirds of AI-enabled vendors still giving away the one feature buyers are willing to pay a premium for.

This isn’t a recovery story. It’s a bifurcation story. And if you’re valuing, building, or buying a B2B SaaS company right now, the gap between those two narratives is where the real M&A risk — and the real opportunity — is hiding.

We pulled apart the new Benchmarkit 2026 B2B SaaS and AI-Native Performance Benchmarks report — 342 participating companies, four years of trend data, segmented by ARR band, ACV, pricing model, and GTM motion — and ran it through an M&A due-diligence lens rather than an operating-benchmark lens. Here’s what the data actually supports, where the consensus reading breaks down, and what it means depending on which side of the table you sit on.

The Headline Recovery Is Real — And It’s the Wrong Story

Start with what’s true. Median CAC payback period improved from 18 months in CY-24 to 16 months in CY-25 — an 11% year-over-year gain and the largest single-year improvement in the four-year trend Benchmarkit tracks. Rule of 40 jumped from a 15% median to 25%, also the largest gain in five years of benchmarking. ARR per employee rose to $175,000, up 17% year-over-year, driven almost entirely by AI-assisted R&D productivity.

| The median company got more profitable and less defensible in the same twelve months. |

Read in isolation, that’s a market snapping back into efficiency. Read against the rest of the report, it’s something else. Gross revenue retention fell from 88% to 84%. The 75th percentile — the companies that are supposed to be immune to market-wide pressure — saw GRR fall from 95% to 91%. Growth rates fell for a fourth consecutive year, from 30% at the median in CY-22 to 20% in CY-25.

The efficiency gain and the growth deceleration are not two separate trends. They’re the same transition viewed from different angles. Companies freed up roughly 2% of revenue from sales and marketing, 8% from R&D, and 7% from G&A in a single year — largely by cutting cost, not by strengthening the business. That’s a cost-restructuring story wearing a recovery costume, and we’ve seen this exact pattern before in adjacent datasets:

Our analysis of the OPEXEngine 2026 benchmarks found the same divergence between headline growth and the retention quality underneath it.

For M&A purposes, this matters because efficiency metrics compress faster than they expand. A company that cut its way to a 25% Rule of 40 score can revert the moment growth-focused reinvestment resumes. A company that earned a 25% score through durable retention and pricing architecture won’t. Benchmarkit’s own framing captures the stakes: fewer than one in four companies in the sample are redeploying the 2025 efficiency windfall into structural advantage. The other three-quarters are either banking the gains, a transient recovery that reverts within 18 to 24 months, or drifting at the median, which, in a market where the median keeps decelerating, is not a stable place to stand.

Five Metrics That Actually Move the Multiple

Skip the vanity metrics. Here are the five data points from the 2026 benchmark set that should actually change how you underwrite a deal, price a target, or defend your own valuation in a process.

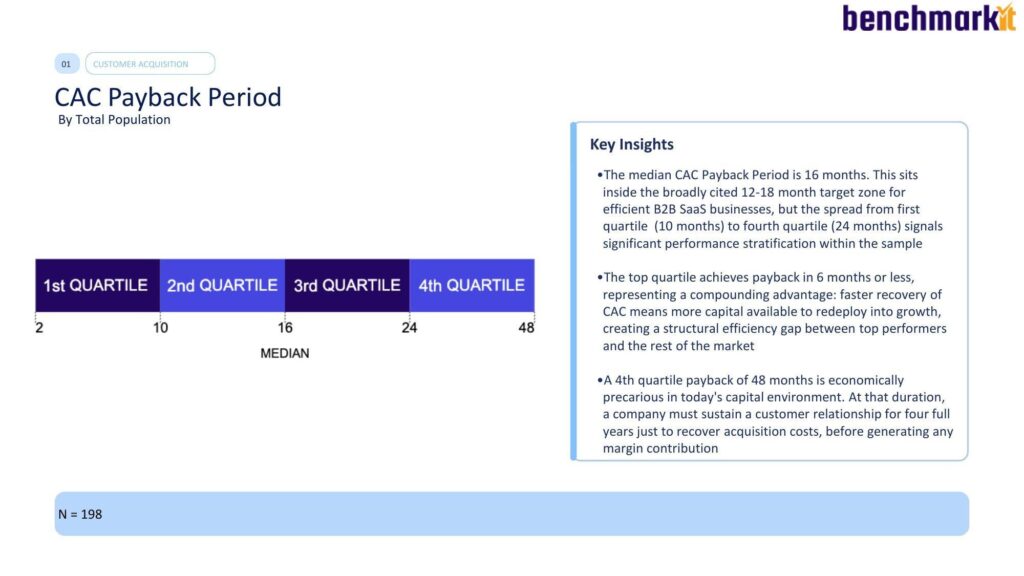

1. CAC Payback Period: The Spread Matters More Than the Median

CAC Payback Period by total population, Benchmarkit 2026 SaaS and AI-Native Performance Benchmarks (n=198).

The median CAC payback period across the 198-company cohort is 16 months, sitting inside the commonly cited 12 to 18 month efficiency zone. But the spread is the real signal: first-quartile companies achieve payback in 6 months or less, while fourth-quartile companies take 48 months — four full years just to recover acquisition cost before a dollar of margin shows up.

That spread is a valuation lever most acquirers underuse. A company sitting at 22-month payback in the 21 to 30% growth cohort, Benchmarkit’s data shows this segment paradoxically has the worst median payback, likely reflecting accelerated investment mode, is not automatically a red flag. But it demands a specific diligence question: is the elevated CAC buying durable growth, or masking inefficient GTM spend that a buyer will inherit?

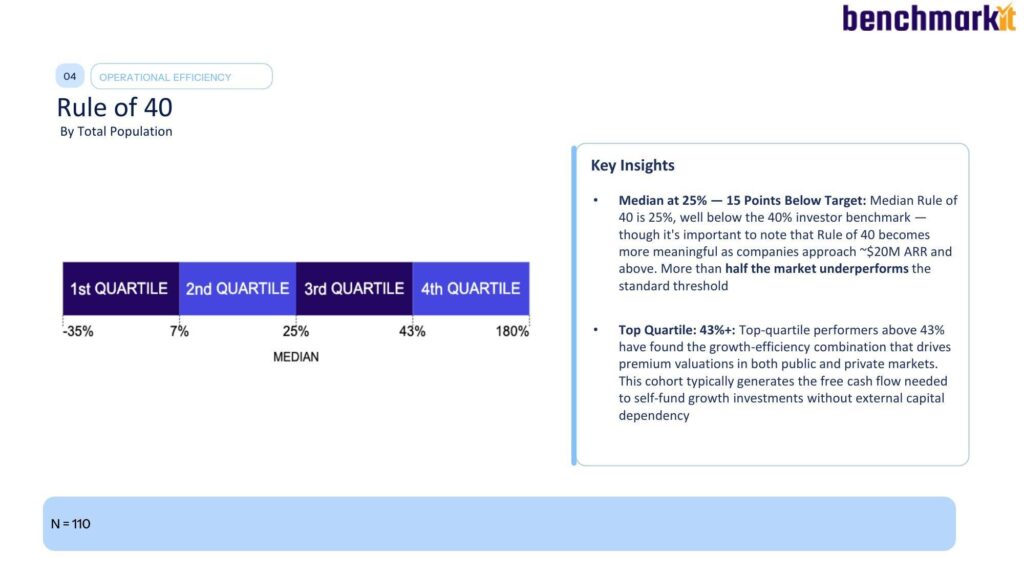

2. Rule of 40: A Metric That Just Got More Misleading

Rule of 40 by total population, year-over-year CY-22 through CY-25, Benchmarkit 2026 report.

Rule of 40, growth rate plus profit margin, jumped from a 15% median to 25% between CY-24 and CY-25, with the top quartile reaching 43%. Subscription-plus-usage pricing models led the cohort at 43% (75th percentile), which on its face validates the hybrid-pricing thesis.

Here’s the problem: Rule of 40 doesn’t distinguish between a point earned through growth and a point earned through margin expansion, and in 2025 nearly all of the gain came from the margin side. A company that improved its Rule of 40 score by cutting R&D 8 points and G&A 7 points looks identical on this metric to a company that improved by accelerating durable, retained growth. They are not the same asset, and they should not clear at the same multiple.

This is the exact composition-blindness we flagged in our review of the OPEXEngine cohort data: buyers who don’t decompose the score are pricing a restructuring as if it were a growth story.

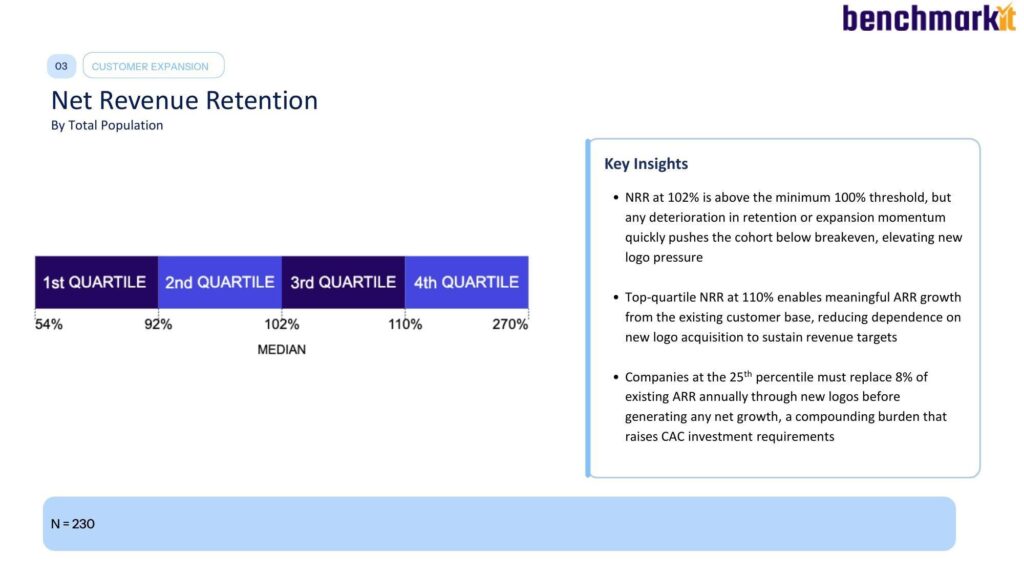

3. Net Revenue Retention: Pricing Architecture Is Now a Structural Determinant

Net Revenue Retention by total population, Benchmarkit 2026 SaaS and AI-Native Performance Benchmarks.

This is the single most important structural finding in the report. Usage-based pricing models post a 108% median NRR. Seat-based models post 95%, below the 100% breakeven threshold. That’s a 13-point structural gap, and Benchmarkit’s data shows it compounds annually rather than closing.

This isn’t a company-execution variable, it’s an architecture variable. A seat-based company cannot out-execute its way to usage-based retention economics without changing how it charges for its product. For an acquirer, that means NRR below 100% in a seat-based target isn’t automatically a distress signal, but it is a signal that the pricing model itself, not the sales team or the product roadmap, is the thing that needs to change post-close.

We’ve written previously about how net revenue retention is decomposed in M&A due diligence, the headline number matters less than whether it’s structurally supported.

There’s a second-order finding buried in the same section that deserves more attention than it gets: expanding an existing customer costs $0.80 per dollar of new ARR, versus $1.63 to acquire a new logo, meaning expansion is 53% cheaper. Yet the report also flags that when expansion crosses 40% of net new ARR (the current median), it starts signaling substitution for new-logo growth rather than amplification of it. A target with expansion-heavy ARR composition and a decelerating new-logo engine is a different asset than one growing on fresh logo acquisition, even at an identical blended growth rate.

4. ARR Per Employee: The Number That’s Rewriting Headcount Economics

ARR per employee benchmark by total population, Benchmarkit 2026 report.

Median ARR per employee hit $175,000 in CY-25, up 17% year-over-year, the largest gain Benchmarkit has recorded. The mechanism is transparent: R&D as a percentage of revenue fell from 35% three years ago to 27% today, with the 25th percentile of R&D spend now at just 22% of revenue, a level the report explicitly states is achievable only through AI-assisted engineering productivity.

The 75th percentile now operates at $253,000 ARR per employee against a $175,000 median, a 1.4x gap the report says headcount cuts alone cannot close. That gap is durable capability, not a one-time restructuring benefit, and it should be treated as such in diligence.

This tracks with what we’ve observed elsewhere in the AI-native cohort, companies profiled in our piece on AI SaaS investment trends and VC rejection signals are running at a fraction of the headcount that PLG-era companies required to hit the same ARR milestones.

The strategic read for founders: if your R&D-to-revenue ratio still sits above 30% and your ARR-per-employee is tracking below $175K, that’s not a rounding error against the benchmark, it’s a signal that your engineering organization hasn’t yet redesigned itself around AI-assisted development, and a buyer’s diligence team will notice.

5. Gross Revenue Retention: The Metric Nobody Improved

The uncomfortable data point sitting underneath all four “recovery” metrics: GRR fell from 88% to 84% at the median, and from 95% to 91% at the 75th percentile, the largest single-year decline in the trend. This is explicitly framed in the report as a market-level dynamic, not a company-execution failure. Top performers were not immune.

That framing matters for valuation. If GRR decline were isolated to poorly-run companies, it would be a company-specific discount. Because it’s market-wide, it should be read as a repricing of the entire asset class’s retention durability, every SaaS target in a 2026 process is operating against a lower retention baseline than it was two years ago, and comparables built on 2023 or 2024 retention assumptions are stale.

| PE/VC INVESTOR TAKEAWAYThe composition of a Rule of 40 or ARR-per-employee score now matters more than the score itself. A target that hit 25% Rule of 40 through cost-cutting and a target that hit it through durable usage-based pricing and retained growth should not clear underwriting at the same multiple, even though the benchmark treats them identically. Build a decomposition step into your IC memo template before your next process, and weight GRR trend as heavily as the headline growth number. |

The AI Monetization Gap Nobody Is Pricing Into Multiples

This is where the 2026 benchmark data gets genuinely contrarian, and where the report’s “Frontier” section, covering 254 B2B SaaS and AI-native companies, deserves far more attention than the retention and efficiency metrics that dominate the headlines.

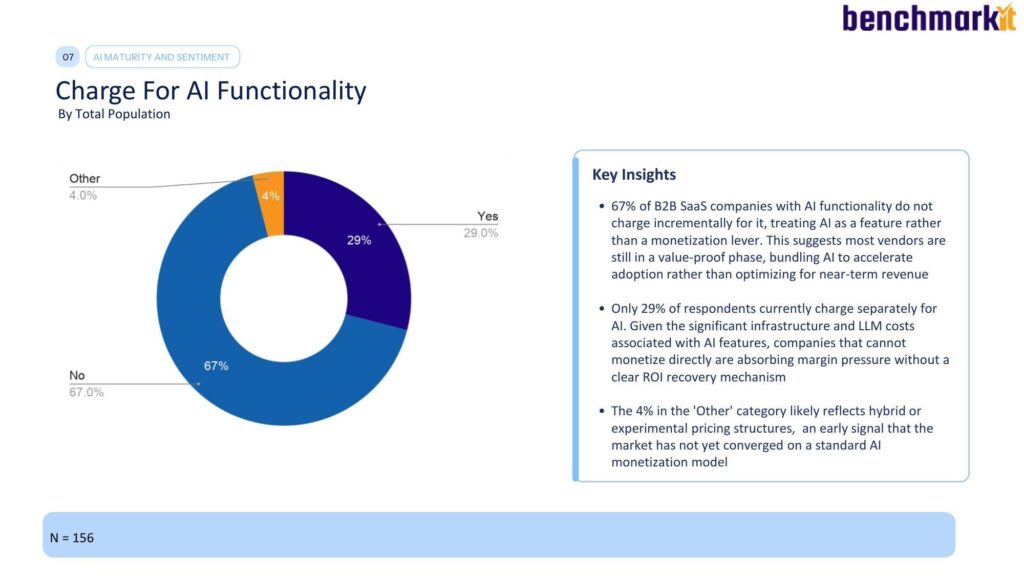

Charge for AI functionality by total population, Benchmarkit 2026 report (n=156).

Thirty-five percent of respondents introduced AI into their product within the past 12 months, the single largest cohort in the sample, and another 24% plan to add AI in 2026. Combined, nearly six in ten B2B SaaS companies are either newly AI-enabled or on the immediate launchpad. Only 9% shipped AI more than 24 months ago, which means the first-mover advantage many 2023 AI adopters were counting on has not had time to compound into durable differentiation for most of the market.

| 67% of B2B SaaS companies with AI functionality do not charge incrementally for it. |

That’s the number that should reframe every AI-native valuation conversation happening in a 2026 deal room. Vendors are treating AI as a bundled feature, not a monetization lever. Only 29% currently charge separately for AI capability. Given the infrastructure and inference costs associated with running AI features, the companies that can’t monetize directly are absorbing margin pressure with no clear recovery mechanism, a dynamic that shows up nowhere in the Rule of 40 calculation until it eventually erodes the margin side of that equation.

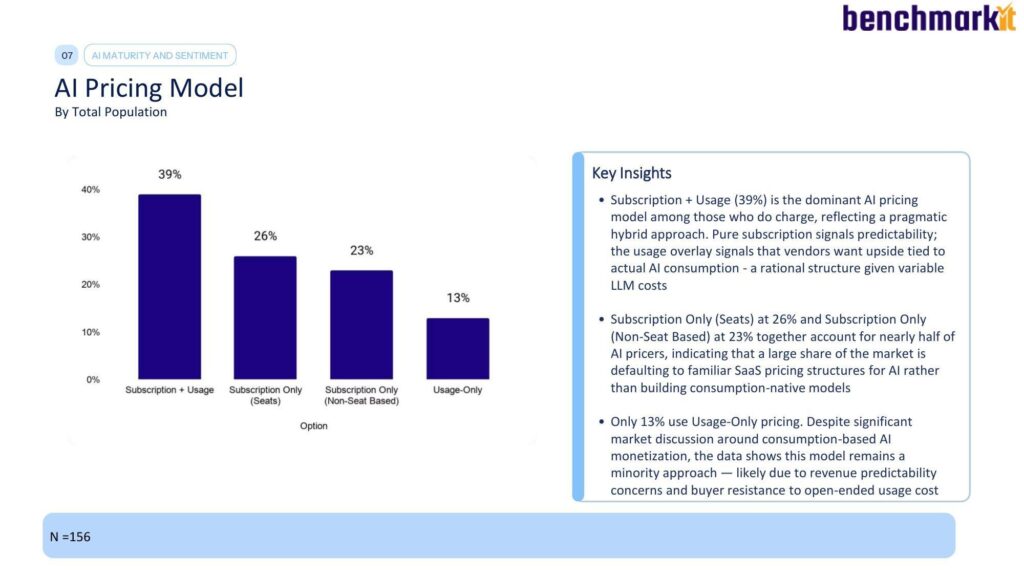

AI pricing model by total population, Benchmarkit 2026 report (n=156).

Among the minority that do charge for AI, subscription-plus-usage is the dominant model at 39%, a pragmatic hybrid that gives vendors upside tied to actual consumption while preserving revenue predictability. But subscription-only models (seat-based at 26%, non-seat-based at 23%) together account for nearly half of AI pricers, meaning a large share of the market is defaulting to familiar SaaS pricing architecture for AI rather than building genuinely consumption-native monetization. Only 13% use pure usage-based pricing for AI specifically, despite the broader market narrative around consumption-based AI monetization, actual adoption remains a minority approach.

The pattern also splits sharply by go-to-market motion. Product-led companies show a striking preference for usage-only AI pricing at 60%, versus just 7% for sales-led organizations, which lean heavily toward subscription-plus-usage (36%), enterprise buyers still want the predictability of a negotiated hybrid structure even when the underlying cost driver is variable.

Why this is an M&A issue and not just a pricing issue:

A target that has shipped AI features but hasn’t monetized them is carrying two liabilities simultaneously. First, the infrastructure cost of running those features is compressing gross margin without a corresponding revenue offset, a drag that will show up eventually in the operational efficiency metrics buyers already scrutinize. Second, and more importantly, the absence of AI-specific pricing means the company has no proof point that its AI capability is something customers value enough to pay for, as opposed to a checkbox feature shipped to avoid losing deals.

We’ve flagged this exact dynamic in our broader work on the AI valuation gap in SaaS M&A: per-seat pricing built on the assumption that human headcount drives usage deteriorates structurally as AI agents replace human operators, and a target with no credible transition path to consumption or outcome-based pricing is carrying unmodeled revenue risk that should discount, not inflate, the multiple.

There’s a related and under-examined risk sitting alongside monetization: whether the target’s AI functionality is even visible to the buyers evaluating it.

As we’ve documented in our research on generative engine optimization and LLM citation footprint, the traditional SaaS brand-building playbook, gated whitepapers, analyst placements, LinkedIn thought leadership, is largely invisible to the AI models buyers now use for vendor research.

A target with strong AI functionality but a citation footprint built entirely on gated content is sitting on an asset that neither ChatGPT, Perplexity, nor Gemini can surface to a prospective buyer typing “best AI-native software” into a chat window. That gap doesn’t show up in the Benchmarkit dataset, but it compounds the monetization gap the dataset does surface: undermonetized AI features that are also undiscoverable represent a double blind spot in most current diligence processes.

| SAAS FOUNDER TAKEAWAYIf your product shipped AI in the last 12 months and you haven’t built a specific pricing line for it, you’re in the 67% majority, but that’s not a comfortable place to be heading into a 2026 or 2027 exit conversation. Buyers are starting to ask directly what percentage of your AI feature usage converts to willingness-to-pay. Run a Van Westendorp or Gabor-Granger pricing test on your AI functionality this quarter, even if you don’t flip the switch immediately. Having the data ready is worth more at the negotiating table than having the feature. |

The Gap Thesis: What the Data Shows vs. What the Market Assumes

Pull the threads together and a consistent structure emerges, one that maps closely to what we’ve called the “gap thesis” in prior analysis: the distance between what vendors and market narratives claim and what the empirical benchmark data actually supports.

Claim: The efficiency recovery signals a healthier market.

Data: The recovery is concentrated in cost reduction (R&D down 8 points, G&A down 7 points, S&M down roughly 2 points), while GRR, the metric that measures whether the underlying business is getting more durable, fell four points in the same period. The market is more efficient and less defensible simultaneously.

Claim: Hybrid and usage-based pricing is a nice-to-have optimization.

Data: It’s a structural 13-point NRR gap that compounds annually. Companies still running pure seat-based pricing in 2026 are not making a neutral commercial choice, they’re accepting a below-breakeven retention ceiling that no amount of operational excellence can fully offset.

Claim: AI features are a monetization opportunity SaaS companies are actively capturing.

Data: 67% of companies with AI functionality aren’t charging for it. The monetization opportunity is real, but the capture rate is low, and the market has not converged on a standard model even among the minority that do charge.

Claim: ARR-per-employee gains reflect broad AI-driven transformation.

Data: The gain is real and structurally durable, but it’s concentrated at the top quartile ($253K vs. $175K median), meaning the “AI productivity dividend” narrative is currently a top-quartile phenomenon being generalized to the whole market.

Claim: Growth deceleration is cyclical and will reverse with market conditions.

Data: This is the fourth consecutive year of decline, from 30% median growth in CY-22 to 20% in CY-25, with the 75th percentile falling even harder, from 75% to 42% over the same period. Four consecutive years is not a cycle. It’s a structural deceleration.

What This Means If You Sit on the Buy Side, the Founder Side, or the Buyer-of-Software Side

For PE and VC Investors

The efficiency metrics in this report are necessary underwriting inputs, but they are not sufficient. A target’s Rule of 40, CAC payback, and ARR-per-employee scores need to be decomposed into their growth component and their margin component before they inform a multiple. The report’s own “Path A / Path B / Path C” framework, restore margin and distribute capital, incrementally reinvest, or redesign the operating model around pricing, expansion, and AI productivity, is directly usable as a diligence lens: ask management which path they’re on, and verify the answer against the R&D ratio, pricing architecture, and expansion dependency data, not against the pitch deck. An estimated 60%-plus of the benchmark population is on Path A or B; fewer than one in four is actually executing Path C. Pricing that fourth-quartile executor at the same multiple as a Path C company is a systematic overpayment risk sitting in plain sight across the current deal pipeline.

For SaaS Founders Approaching Exit

The metrics buyers will actually interrogate in 2026 diligence have shifted. NRR quality (is it usage-based or seat-based, and what’s the trend), GRR trend (not just the current number, the four-year direction), AI monetization proof points (not just AI feature shipping velocity), and ARR-per-employee relative to the $175K median and $253K top-quartile benchmark are now table-stakes diligence questions, not nice-to-haves. If your growth story is expansion-heavy, above the 40% of net-new-ARR threshold the report flags, be ready to show that new-logo acquisition is being amplified, not substituted for, because buyers now know to ask.

For Enterprise CTOs and CPOs

The vendor evaluation calculus is shifting in a way this data makes explicit. A vendor still on pure per-seat pricing in 2026, with no usage or outcome-based component, is carrying revenue-model risk that should factor into your procurement risk assessment, not because the product is bad, but because that vendor’s own retention economics are structurally capped below the usage-based cohort’s, and a vendor under retention pressure has different incentives around your contract terms, your renewal negotiation, and your support quality than one operating from a position of compounding strength. Ask your vendors directly: what percentage of your AI functionality is monetized versus bundled, and what’s your NRR trend over the last three years, not just the current quarter.

| ENTERPRISE CTO/CPO TAKEAWAYA vendor’s pricing architecture is now a proxy for its retention risk. Before your next renewal negotiation, ask your top SaaS vendors for their NRR trend and whether their AI functionality is monetized or bundled. The answers tell you more about contract risk than their feature roadmap does. |

The 18-Month Window

Benchmarkit frames this explicitly as a limited window: how leadership teams redeploy the 2025 efficiency gains over the next 18 months will determine whether the performance gap to the frontier closes or widens beyond recovery. That’s not investor-relations language, it’s a testable claim the four-year trend data actually supports. Companies on Path A revert to previous performance levels within 18 to 24 months as AI-native competitors compound their structural advantages. Companies on Path B track the median trajectory, which, given four consecutive years of growth deceleration, is a declining target, not a stable one. Companies on Path C capture the structural advantages the benchmark data shows compounding annually: usage-based pricing’s NRR premium, vertical SaaS’s CLTV:CAC advantage (5.6x versus 4.1x for horizontal players), and the AI-productivity ARR-per-employee gap.

The uncomfortable implication for anyone valuing, running, or buying a B2B SaaS company right now: the current benchmark snapshot looks better than the underlying trajectory. Multiples set against this quarter’s Rule of 40 or CAC payback number, without decomposing where that number came from and where the four-year trend is heading, are being set against the wrong picture.

Where to Go From Here

If you’re heading into a 2026 process, as a buyer, a seller, or a strategic evaluating a vendor, the practical next step is the same regardless of which side of the table you’re on: decompose every headline metric into its growth component and its margin/cost component, check the NRR against pricing architecture rather than treating it as a monolithic score, and ask directly whether AI functionality is monetized or merely shipped. The companies and buyers doing that work now are the ones who will be pricing Path C correctly while the rest of the market is still pricing the recovery narrative.

DevelopmentCorporate works with SaaS founders, PE sponsors, and strategic acquirers to translate benchmark data like this into deal-specific valuation and due-diligence frameworks. If you’re evaluating a target, preparing for an exit, or want a second opinion on how your own metrics stack up against the 2026 cohort, reach out to discuss your specific situation.

Frequently Asked Questions

What is the median Rule of 40 score for B2B SaaS companies in 2026?

The median Rule of 40 score across Benchmarkit’s 342-company 2026 cohort is 25%, up from 15% the prior year, the largest single-year gain in five years of benchmarking. The top quartile reaches 43%, led by subscription-plus-usage pricing models.

What is a good CAC payback period for a SaaS company in 2026?

The 2026 median CAC payback period is 16 months, improved from 18 months in CY-24. Top-quartile companies achieve payback in 6 months or less, while fourth-quartile companies take up to 48 months.

How does usage-based pricing affect Net Revenue Retention?

Usage-based pricing models post a median 108% NRR versus 95% for seat-based models, a 13-point structural gap that the 2026 benchmark data shows compounding annually, independent of company-level execution quality.

Are B2B SaaS companies charging for AI features?

No, 67% of B2B SaaS companies with AI functionality in their product do not charge incrementally for it, according to the 2026 benchmark data covering 254 B2B SaaS and AI-native companies. Only 29% currently monetize AI directly.

Sources: Benchmarkit 2026 B2B SaaS and AI-Native Performance Benchmarks (June 2026); DevelopmentCorporate analysis.