Software Equity Group Q1 2022 SaaS Public Market Update

The Software Equity Group (SEG) regularly publishes quantitative research on the software and SaaS market M&A activity. The SEG SaaS Index contains dozens of publicly traded SaaS companies. They recently published their SEG Snapshot: 1Q22 SaaS Public Market Update. It provides a ton of data on SaaS valuations and financial operating metrics. The impact of the market downturn can be clearly seen across all categories of SaaS.

I have extracted a few key data points including:

- SEG SaaS Index: Q1 2021 to Q1 2022

- EV/Revenue Multiple Distribution

- Monthly EV/Revenue Declines

- Revenue Growth Remained Strong, In Spite of Valuation Declines

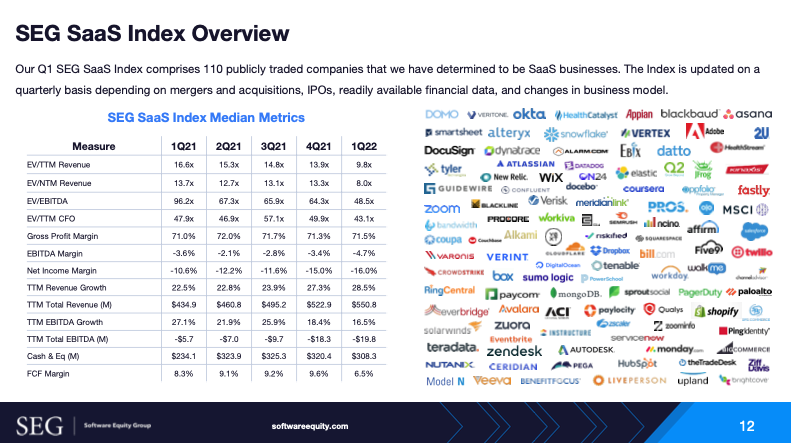

- Median Operating Metrics Remain Strong

- SaaS Product Category Performance

- SEG SaaS Index: Top 25%

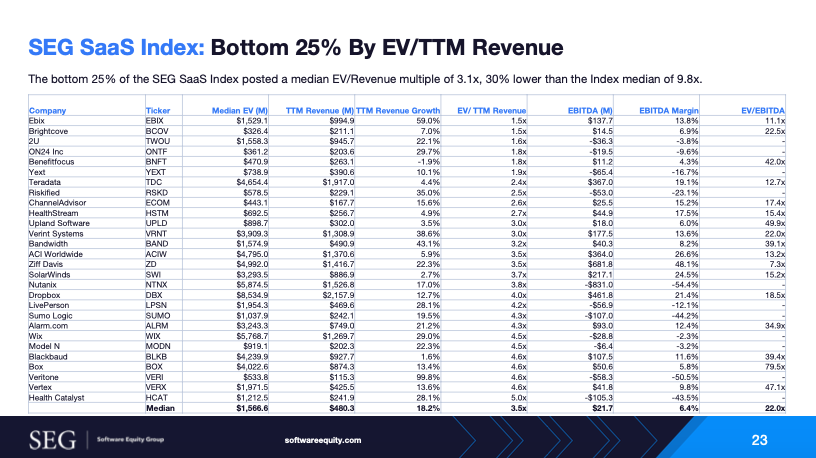

- SEG SaaS Index: Bottom 25%

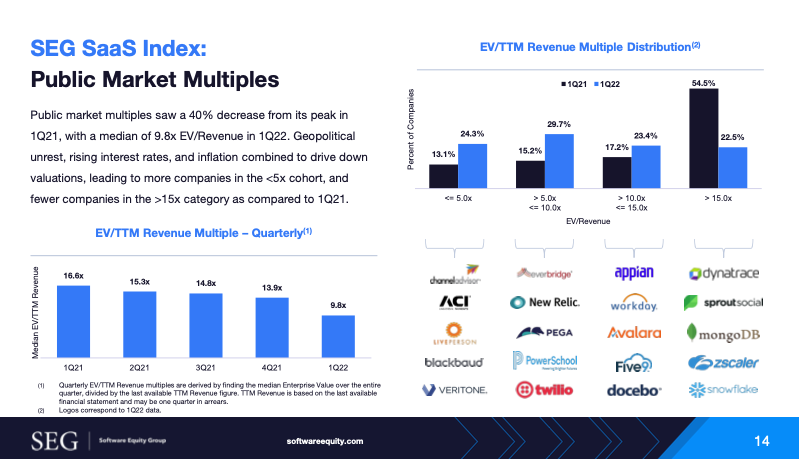

SEG SaaS Index: Q1 2021 to Q1 2022

SaaS valuations peaked in Q2 2021. Median EV/Revenue (ttm) slid from 13.8x in Q4 2021 to 9.8x in Q1 2022.

SEG Snapshot: 1Q22 SaaS Public Market Update

EV/Revenue Multiple Distribution

The percentage of the SEG SaaS Index trading above 15x declined dramatically.

SEG Snapshot: 1Q22 SaaS Public Market Update

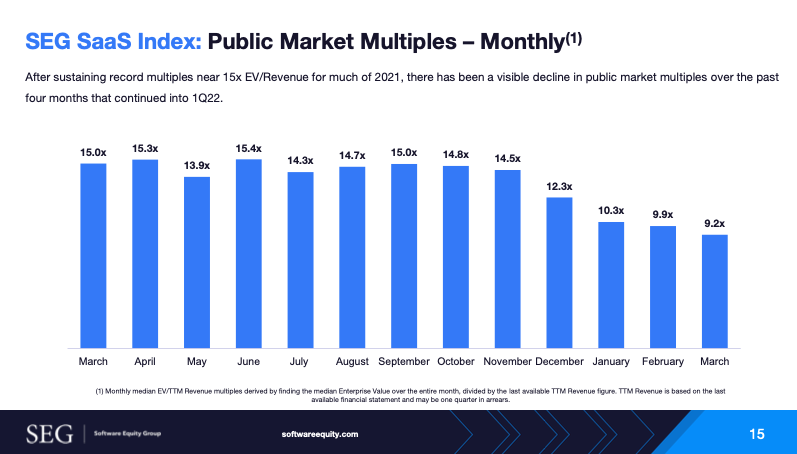

Monthly EV/Revenue Declines

Median E/Revenue multiples began to decline materially after Thanksgiving 2021. That ttrend continued each month in 2022.

SEG Snapshot: 1Q22 SaaS Public Market Update

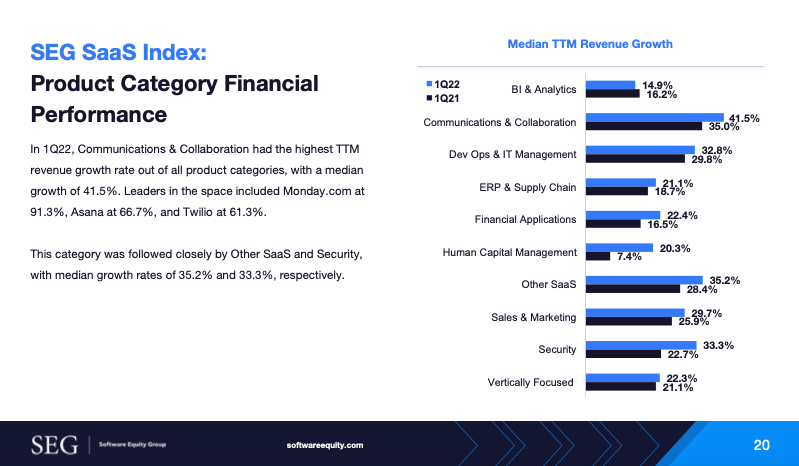

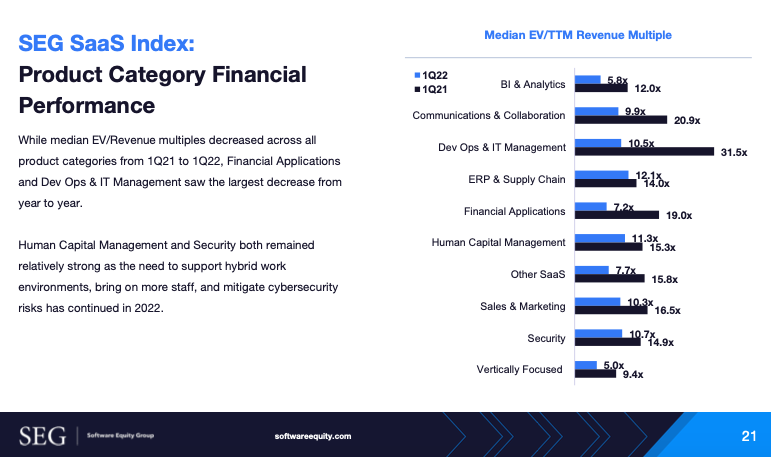

Revenue Growth Remained Strong, In Spite of Valuation Declines

Revenue growth remained strong across nine of the ten categories in the SEG Index.

SEG Snapshot: 1Q22 SaaS Public Market Update

Median Operating Metrics Remain Strong

Median operating ratios remain strong, while cash flow margins have declined.

SEG Snapshot: 1Q22 SaaS Public Market Update

SaaS Product Category Performance

This chart provides insights into which SaaS has experienced the biggest valuation declines in Q1 2022.

SEG Snapshot: 1Q22 SaaS Public Market Update

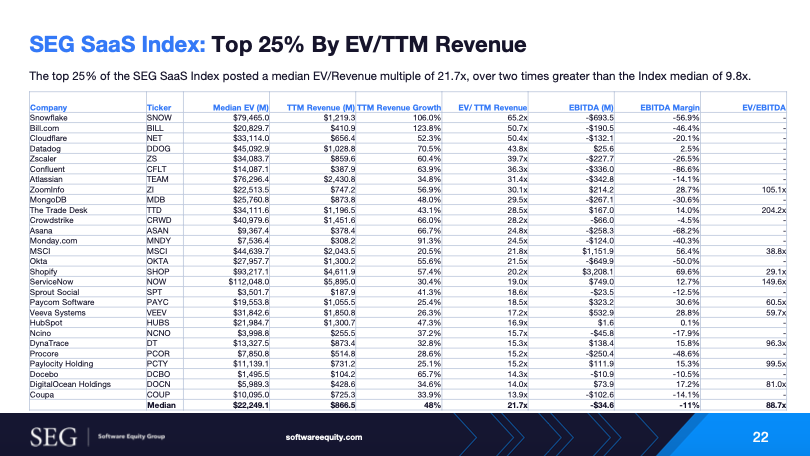

SEG SaaS Index: Top 25%

SEG Snapshot: 1Q22 SaaS Public Market Update

SEG SaaS Index: Bottom 25%