The Roll-Up Reset: Why E2open Cleared at 3.4x When the Index Says 7x

A scaled, profitable, network-rich supply-chain platform — the kind the public index says is worth 7x revenue — sold for roughly half that. The gap is the whole story, and it tells founders exactly which valuation engine just died.

There is a number floating around the supply-chain software world right now that makes founders feel rich and makes acquirers laugh quietly into their term sheets. The number is 7x.

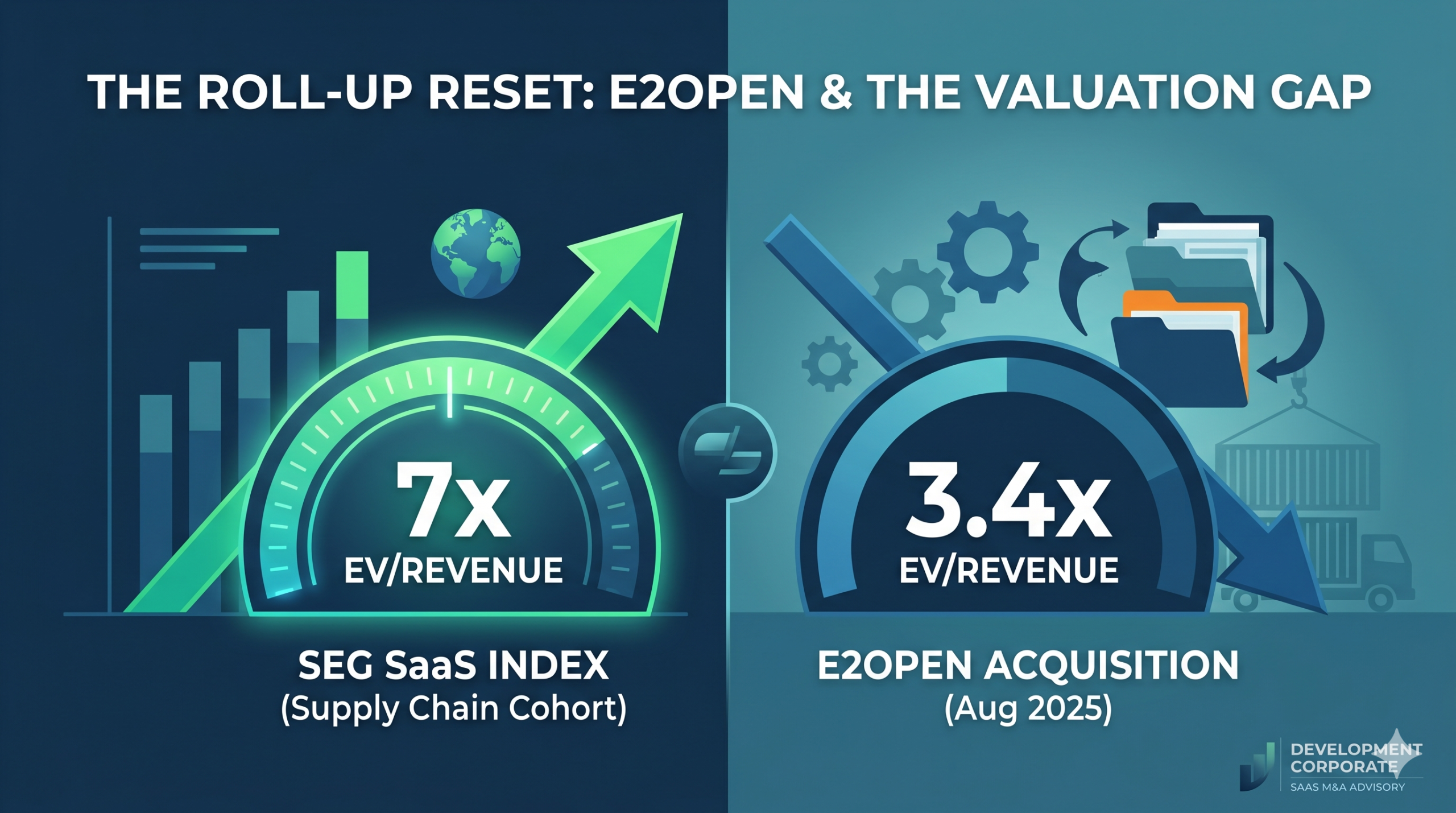

That is, roughly, the one-year median EV/revenue multiple for the ERP and supply-chain cohort in the SEG SaaS Index. It is a real number, drawn from real public companies, updated daily, and almost useless as a benchmark for what your supply-chain software business will actually fetch when somebody writes a check. I want to explain why, using the single cleanest piece of evidence available: WiseTech Global’s acquisition of E2open, which closed in August 2025 at an enterprise value of $2.1 billion on roughly $608 million of revenue.

Do that division and you get about 3.4x. Put enterprise value over subscription revenue alone and you can stretch it to maybe 4.2x. Either way, a scaled, profitable, Gartner-leading, network-rich supply-chain platform — the kind of asset the index says is worth 7x — sold for roughly half that to the only bidder who showed up with a real check.

That gap is the whole story. And the question worth asking is not “why did E2open sell cheap.” It is whether buyers have permanently reset how they value the entire private-equity-style consolidation playbook — the buy-cheap, bolt-on, re-rate-and-exit machine that has financed a decade of software M&A. My answer, after thirty years of watching software roll-ups inflate and deflate, is yes — but not in the way the headline number suggests. Something specific got repriced, and if you are a founder building toward an exit, knowing exactly what got repriced is the difference between a 4x outcome and an 8x one.

I have watched this movie before

Let me establish where I’m standing, because it matters for what follows.

I spent the formative part of my career inside the last great software consolidation wave. At KnowledgeWare and then Sterling Software in the late 1980s and 1990s, I led or worked on sixteen software-industry transactions totaling more than $300 million — including the $220 million carve-out of Texas Instruments’ software division, which made Sterling the world’s largest provider of CASE tools. Sterling itself was a roll-up. It acquired, integrated, cross-sold, and ultimately sold itself to Computer Associates in 2000. CA, of course, was the canonical software roll-up of its era — a company whose entire valuation thesis rested on the market’s willingness to capitalize acquired revenue at platform multiples. I tell the longer version of that story in The Ghost of CASE Tools.

Here is the thing nobody tells you about roll-ups until you’ve lived inside two or three of them: a roll-up is not a product strategy. It is a financial machine with a software wrapper. The machine has three engines. The first is organic growth — the acquired businesses keep selling. The second is leverage — you borrow cheaply against predictable recurring revenue and amplify your equity returns. The third, and the one everyone forgets, is multiple arbitrage: you buy small companies at low multiples, weld them into a platform, and exit the platform at a higher multiple than the sum of its parts.

When all three engines fire, the returns are spectacular. The deepest study of the buy-and-build strategy found it produced higher average IRRs than standalone buyouts — roughly 31.6% versus 23.1%. That is why, by deal count, add-on acquisitions became the dominant structure in U.S. buyouts, accounting for about 76% of buyout activity by mid-2025. The machine works. But it has a brutal failure mode: if two of the three engines stall at once, leverage stops amplifying gains and starts amplifying losses. That is precisely what happened to the software roll-up between 2021 and 2026 — a dynamic I unpacked in Operational Alpha Is a Warning Label for SaaS Sellers. And E2open is the autopsy.

What E2open actually was

Most coverage of the WiseTech deal framed E2open as a “supply-chain SaaS company.” That framing hides the most important fact about it. E2open was itself a roll-up.

It was assembled — first under Insight Partners, then taken public in 2021 through a SPAC sponsored by Chinh Chu’s CC Capital — out of a long string of acquisitions: BluJay Solutions, Amber Road, INTTRA, and others. Some were good. Some were legacy systems that, by the company’s own admission, were difficult to integrate. The result was a company with a magnificent connected network — 500,000-plus connected enterprises, thousands of blue-chip customers, real logos — sitting on top of a tangle of partially-integrated code and the debt of a decade of dealmaking.

For roughly two years before the sale, E2open’s revenue declined. The quarter before the deal was announced marked its first positive year-over-year revenue growth in over two years — about 1%. Gross margin sat around 65%. The company generated EBITDA — about $158 million of it on $608 million of revenue — but the growth engine, the first of our three engines, was dead.

So here is a PE-style consolidation roll-up, fully built out, brought to market through a strategic review run by Rothschild & Co. And the best available outcome was a sale to a strategic acquirer, WiseTech, at roughly 3.4x revenue — with founder Richard White’s team underwriting an explicit synergy case ($85–$120 million of cost synergies, $30–$50 million of revenue synergies) and a day-one EPS-accretion story. Not a sponsor stepping up to take the platform private at a premium and run the playbook again. A strategic, paying a cash-flow-and-synergy price.

Read that sequence again, because it is the entire thesis in one transaction. The roll-up exit — the part where a sponsor pays up because they believe they can re-rate the aggregated platform — did not happen. It was no longer available. The asset cleared to whoever had a strategic reason to own the cash flows.

Five deals, four years, one trend

One transaction is an anecdote. So here is the cohort — five take-privates and strategic acquisitions in the ERP / supply-chain / planning / procurement neighborhood, lined up by announcement date:

| Target | Buyer (type) | Announced | Segment | EV | EV / Revenue |

|---|---|---|---|---|---|

| Anaplan | Thoma Bravo (sponsor) | Mar 2022 | Planning / EPM | $10.7B | ~18x trailing (14x fwd) |

| Blue Yonder | Panasonic (strategic) | Apr 2021 | Supply chain | $8.5B | ~8x (67% recurring) |

| Coupa | Thoma Bravo (sponsor) | Dec 2022 | Spend mgmt | $8.0B | 8.4x forward |

| Logility | Aptean / TA-Insight-Clearlake | Jan 2025 | SC planning | ~$0.44B | ~4.3x |

| E2open | WiseTech (strategic) | May 2025 | Supply chain | $2.1B | ~3.4x (4.2x on subscription) |

Anaplan went to Thoma Bravo in March 2022 at roughly 18 times trailing sales — a growth-equity darling taken private at the absolute top. Coupa followed in December 2022 at about 8.4x forward revenue, after a process that reportedly drew fourteen bidders — already a meaningful step down nine months later. Blue Yonder, the purest supply-chain comp on the board, sold to Panasonic in 2021 at roughly 8x on just over $1 billion of revenue.

Then the regime changed. Logility — a clean, profitable, 85%-recurring supply-chain planning vendor — was bought by Aptean, a consolidator backed by TA Associates, Insight Partners, Charlesbank, and Clearlake, for $14.30 a share in January 2025 — an enterprise value near $440 million on about $102 million of revenue, roughly 4.3x. A literal PE roll-up bought a literal supply-chain SaaS asset, and the number was four-ish. Five months later, E2open cleared at 3.4x.

Now stand back and look at the shape. The 2021–2022 cohort cleared at 8 to 18 times revenue. The 2025 cohort cleared at 3.4 to 4.3 times. That is not noise. That is a roughly 60% compression in clearing prices for substantively similar assets over a 36-month window.

And here is the tell that it’s structural rather than asset-specific: that haircut almost exactly tracks the public-market reset. The SaaS Capital Index peaked near 18.6x EV/revenue in late 2021 and entered 2026 at roughly 6 to 7x — also about 60%. The private deals didn’t compress because the assets got worse. They compressed because the entire pricing regime moved underneath them, and private valuations adjust through transactions with a lag — the same sequential EV/revenue decline I’ve been tracking since 2024.

The 7x is a survivorship mirage

So why does the index say 7x while the deals print at 3.4x? Because the public-market category median is a survivorship statistic, and you are reading it wrong if you treat it as a benchmark for your business.

The ERP & supply-chain category median is pulled upward by a handful of high-quality names that bear no resemblance to the assets actually changing hands. Descartes trades around 7.5x on healthy double-digit growth and a 45-plus Rule of 40. Samsara trades above 10x. Those companies are not for sale — and if they were, they would sell above the median, not at it. Meanwhile the blended median across the entire SEG SaaS Index is just 3.0x. The category median describes the companies that earned the right to stay public and independent. It does not describe the troubled, low-growth, integration-laden roll-up that hits the market because its sponsor needs liquidity.

This is the part founders consistently get wrong. They pull a public-comp median off a beautiful interactive chart, apply it to their own ARR, and walk into a process anchored on a number that describes a population they are not part of. It is exactly the valuation trap I’ve warned about: the right comp for E2open was never the 7x category median. It was the bottom-quartile, sub-30-Rule-of-40 cohort — which trades at or below 3x. Measured against that, WiseTech arguably paid a small premium. The market did not get cheaper across the board. It bifurcated — and the gap between the two halves has never been wider.

What actually reset (and what didn’t)

Let me be precise about the claim, because precision is the whole point.

Buyers did not abandon consolidation. Buy-and-build is more dominant by deal count than it has ever been. Sponsors still have well over a trillion dollars of dry powder. The arbitrage logic — buy small at low multiples, exit large at high multiples — still works mechanically; sub-$100 million buyouts traded around 6.4x EBITDA while mega-deals above $5 billion traded around 16.9x, and that ten-turn spread is the entire reason roll-ups exist. It has not closed.

What reset is narrower and more lethal: the market stopped paying a premium for aggregated scale alone, and it repriced the exit multiple the whole model is underwritten against.

Go back to the three engines. In 2021, a sponsor could assume durable organic growth and a stable-to-rising exit multiple. Both blew up at once. Growth got harder as the easy SaaS land-grab matured. And the exit multiple — the price the next buyer would pay for your assembled platform — collapsed from the high teens toward the mid-single digits. As Apollo put it bluntly: when two of the three traditional value levers, growth and exit multiples, come under pressure simultaneously, leverage magnifies the downside. E2open had a network, logos, EBITDA — and nothing a sponsor could re-rate. So no sponsor bid the platform up. A strategic took the cash flows.

That is the reset, stated cleanly: not “consolidation is dead,” but “the financially-engineered, low-organic-growth roll-up has been repriced from a growth-multiple asset to a cash-flow-and-synergy asset.” If the only thing your platform offers a buyer is scale, the buyer now pays you a cash-flow multiple for it. The premium for the aggregation itself — the thing that made the machine print money — is gone.

The financing channel quietly closed

There is a second, less-discussed reason these assets clear lower, and it has nothing to do with multiples on a chart. It has to do with who can still afford to bid.

Roll-ups run on leverage. The whole model assumes a deep, liquid market of lenders willing to finance the platform’s debt and refinance it on the way to exit. That market has narrowed sharply. Roughly 40% of private-credit borrowers now carry negative free cash flow, PIK usage is climbing even as headline spreads compress, and something like 46% of outstanding software loans mature within four years. As I argued in SaaS Private Credit Lenders Are Done With ARR, credit markets reprice risk 6 to 18 months ahead of the equity M&A market — so the ARR-lending collapse is a leading indicator for deal multiples, not a lagging one.

The mechanism is direct. As lenders reassess which models are durable, refinancing gets selective, buyer leverage tightens, and the pool of viable acquirers shrinks — precisely for the assets most dependent on credit to transact. Low-growth roll-ups are the single most credit-dependent category in software, so they get hit twice: once on the multiple, once on the financing. The JPMorgan software-loan markdowns were the institutional confirmation of a dynamic already visible in deal flow. Note that WiseTech funded the entire E2open purchase with a fresh $3 billion syndicated facility — but WiseTech is a profitable, fast-growing strategic with the balance sheet to support it, not a sponsor stacking leverage on a no-growth target.

The AI overlay — why this isn’t just a cycle

If all of this were merely cyclical, you could wait it out. I do not think that’s what’s happening, and the reason is the same one I keep returning to. In the late 1980s, the CASE tools my companies sold were going to automate software development. The category attracted enormous capital, consolidated rapidly, and then got disrupted by a shift in how software was actually built — a fifty-year pattern that rhymes uncomfortably with today. The roll-ups that aggregated CASE assets at premium multiples watched those multiples compress as the demand thesis eroded. The aggregation didn’t save them; it just meant they’d assembled a larger pile of a depreciating asset.

We are at a structurally similar moment, and the smart money is pricing it in. The Q1 2026 “SaaSpocalypse” erased on the order of a trillion dollars of aggregate SaaS market capitalization. The driver is not a recession — it’s a re-underwriting of software’s durability in an AI world. As I documented in The AI Valuation Gap, 83% of M&A buyers now pay higher multiples for AI-native or AI-integrated targets, and 85% cite commoditization from AI as their single biggest long-term concern about SaaS cash-flow durability.

Look at the legacy roll-up profile through that lens. Much of what got rolled up between 2018 and 2021 was exactly the replicable, seat-based, point-solution functionality now most exposed to AI substitution. The market isn’t just discounting these assets for low growth — it’s discounting them for fragility, for the rising probability that the acquired functionality gets commoditized by something a competitor can stand up in a quarter. That is a permanent repricing of risk, not a temporary repricing of rates. The moat scorecard — proprietary data plus mission-critical workflow — is now the line between the two halves of the bifurcation.

What this means if you’re a founder

If you’re building a B2B SaaS company with any thought of an eventual sale — and at the pre-seed and seed stage I work with, you should think about it from day one — here is what the roll-up reset means in practice. (For the early-stage version of these numbers, see Enterprise Value of Pre-Seed and Seed-Stage SaaS Acquisitions in 2025.)

- Stop anchoring on public comps. The 7x you read off the index describes companies that earned the right to be independent. The realistic private range for a lower-middle-market SaaS business in 2026 is roughly 3x to 7x ARR, with a median around 4.5x. The top of that range is reserved for 30%-plus growth, 120%-plus NRR, and a Rule of 40 above 50.

- Organic growth is the only engine you fully control. The reset killed the acquired-growth premium. Buyers will no longer pay a platform multiple for revenue you bought rather than built. Net revenue retention above 110% is the single most legible proof that your growth is real and durable.

- Customer concentration quietly sets your multiple. I’ve watched two companies with identical ARR receive offers 2x to 3x apart, and the variable was almost always concentration. A business with 40% of revenue in one logo trades at 2x to 3x almost regardless of growth; the same business with no customer above 10% can command 5x to 6x.

- Be the thing AI can’t replicate. If your moat is a feature set, assume a buyer’s own engineering team with a good model can rebuild it. If your moat is a unique data asset accumulated through use, or a workflow so embedded that ripping it out is unthinkable, you’re on the right side of the bifurcation.

- Profitability bought Logility a turn. It is not a coincidence that the cleaner, profitable, 85%-recurring asset cleared above the larger, troubled, debt-laden one. In a market that has stopped paying for growth-by-acquisition, demonstrated cash generation is the next-best thing you can show — the same lesson at the center of the SaaS exit crisis.

The historical rhyme

Software consolidators get a premium multiple for exactly as long as the market believes acquired revenue is durable and the platform compounds. The moment organic growth stalls, the market stops capitalizing that acquired revenue at platform multiples and re-rates the whole thing toward a cash-flow number. I watched it happen to the CASE-tools consolidators. I watched a version of it shape how CA was ultimately valued. I am watching it happen now to the supply-chain and ERP roll-ups assembled in the last cycle — and the seller-expectation gap it creates is the most common reason good processes stall.

E2open is the cleanest single data point I’ve seen for the pattern in years: a fully-built PE-style roll-up, brought to market through a formal review, that could not find a sponsor willing to pay up for the aggregated platform and instead cleared to a strategic at roughly 3.4x on a synergy case. Logility, the cleaner version of the same story, cleared at four-ish. Both sit a full regime below the 8-to-18x their predecessors fetched in 2021 and 2022.

So — have buyers reset valuation expectations for PE-style consolidation roll-ups? Yes. But the precise reset is this: the exit-multiple re-rating and the premium-for-scale assumption that powered the entire model have been repriced toward cash-flow-and-synergy multiples, while the AI overlay has converted what looked like a cyclical discount into a structural one. Consolidation isn’t dead. The free lunch in consolidation is.

For founders, the implication is almost old-fashioned, which I find satisfying after thirty years of watching the fashions cycle. The market has stopped paying for financial engineering and started paying — again — for the boring fundamentals: durable organic growth, diversified revenue, real retention, genuine workflow lock-in, and the discipline to generate cash. Build that, and you’re on the right side of the bifurcation. Build a pile of acquired revenue and hope for a re-rate, and you’re E2open, running a strategic review and taking the one bid that shows up.

Work with DevelopmentCorporate

DevelopmentCorporate LLC is an M&A advisory and strategic-consulting firm for pre-seed and seed-stage B2B SaaS founders — competitive intelligence, win/loss analysis, GEO / LLM-visibility strategy, and exit advisory. John Mecke has 30+ years in enterprise software, including 16+ acquisitions totaling over $300M at KnowledgeWare and Sterling Software. Book a call.

Notes on sources & method

Deal values and terms are drawn from acquirer and target press releases and public filings: WiseTech/E2open ($2.1B EV, ~$608M revenue, ~$158M EBITDA; closed Aug 2025); Aptean/Logility ($14.30/share, Jan 2025; revenue and ~$79M cash from Logility FY25 filings, with ~4.3x an estimate net of cash); Thoma Bravo/Anaplan ($10.7B, ~18x trailing sales, Mar 2022); Thoma Bravo/Coupa ($8.0B, ~8.4x forward revenue, Dec 2022); Panasonic/Blue Yonder ($8.5B EV on >$1B 2020 revenue, 67% recurring, Apr 2021). Public-market context from the SEG SaaS Index, the SaaS Capital Index, and published 2026 private-equity and software-valuation research. Multiples are computed on the revenue bases noted; where total versus subscription revenue materially changes the figure, both are given. This piece is commentary, not investment advice.