M&A Basics for Product Managers

The pace of mergers and acquisitions in the tech market is on track to set new records this year. The Software Equity Group reported that there were 3,052 software M&A transactions in 2020. In the first half of 2021, there were 769 deals. They estimate that 2021 will set a new record. Acquisitions are challenging times for product managers. On the one hand, they can provide an opportunity for career growth. They can also result in the elimination of a product manager’s job. Product managers should learn the basics of M&A. Product managers should learn the basics of M&A. Product managers need to understand M&A basics.

M&A Roles & Responsibilities

17 different roles take part in an M&A project. While the roles may vary from company to company, these are the typical players.

CEO/President

The top executive in your company will lead your project. They set the tone and drive the process. At the end of the day, they are accountable for the deal. The CEO/President will take part in almost every step of the process. Most CEOs will have had experience in M&A and will impart their particular style on the deal.

Personal styles vary significantly. One CEO that I worked for, who led over 60 M&A deals, was very aggressive. He dominated the process. His goal was to convert the executives and employees to his vision of a management system. Other CEOs I have worked for have taken a more collegial approach to the process aimed at winning the hearts and minds of the target company. A third CEO delegated most of the work to his executive team. One approach is not necessarily better than another. What is important is to understand how your leadership wants to approach the process.

Chief Financial Officer

The CFO/VP of Finance is involved in nearly every aspect of the process. First, they will be the definitive source of financial information and modeling. They build the models that describe the acquisition. CFOs play a major role in the due diligence process. They own financial due diligence. They often coordinate legal due diligence as well. The CFO will be actively involved in briefing boards of directors, investors, investment bankers, and lenders. CFOs bring a unique perspective to the table. They have practical insight into the operation of almost every function in the business.

CTO

The senior technology executive in the company participates in almost every part of the process. They may not be involved in the earliest stages of the process where the CEO/CFO first meets with the target company’s management. After the exchange of a term sheet, however, they will be actively involved. The CTO is the primary person to assess the quality and capabilities of the target company’s solutions, technology, and technical operations. They and their team will develop the technical diligence request and conduct technical due diligence. They assess the risks of the target company’s technology (e.g. disaster recovery, continuity of technical operations, etc.) In integration planning, they determine how to blend development teams and organizations, as well as development environments, data centers, and cloud operations.

VP Corporate Development

The VP of Business/Corporate Development coordinates the overall process. This includes doing baseline research, of acquisition candidates, and arranging initial meetings. They coordinate the due diligence process. This involves building diligence information requests, managing the confidential data room, and managing the logistics of the diligence process. They are also the point person for managing the relationships with Investment Bankers. They also coordinate the merger integration planning and rollout process.

General Counsel

Many companies have their own internal general legal counsel. They also use outside law firms to support various parts of the transaction. This includes activities such as legal due diligence, formation of legal entities to implement the acquisition, negotiation, and execution of agreements such as term sheets, definitive agreements, and regulatory filings.

VP Marketing/Chief Product Officer

Like the CTO and VP Operations, the senior marketing leader will get involved in the process once a decision has to work together has been made. In many organizations, product management responsibilities have been slit off into a new role, the Chief Product Officer (CPO). They will be accountable for assessing the product management and product marketing teams. They assess demand generation programs and major events like customer conferences, trade shows, etc. The VP Marketing handles relationships with industry analysts like Gartner, Forrester, Ovum, etc. They work on updating corporate branding, signage, websites, etc. They often oversee the work of product managers/product marketers in the M&A process.

VP Development

The VP Development works in diligence, integration planning, and rollout. They assist the CTO in the assessment of the development organization, development processes, and infrastructure.

VP Operations

The VP Operations for SaaS organizations plays a role similar to the CTO. During diligence, they assess the structure, capabilities, and certifications of data centers. They rationalize the costs and use of infrastructure software. During Integration planning, they build detailed plans to integrate the two company’s technical operations. Often, they will find best practices and capabilities in the target company’s operations that can leverage in their own.

VP Sales

The VP of Sales takes part in the latter stages of due diligence, integration planning, and acquisition rollout. VP Sales are often not involved in the early stage of the process due to concerns that their own company must continue to hit their revenue targets. The target company may be sensitive that they will expose too much info about major sales deals and the contents of their pipeline. After the definitive agreements are negotiated, the VP of Sales starts to play a more active role. They assess the structure, talent, and performance of the sales team. They look at sales compensation plans to determine how to integrate with their current sales compensation plan. They also assess the sales process and support tools like SalesForce. Often, the head of sales will tour International sales locations with the CEO and CFO during operational due diligence.

VP Professional Services

The VP Professional Services work during due diligence, integration planning, and rollout activities. They will assess the consulting leadership and staff as well as their consulting offerings. They will also assess the depth, quality, and availability of external consulting partners.

VP Human Resources

The senior HR executive participates in due diligence, integration planning, and acquisition rollout. They will be responsible for assessing talent throughout the organization. During diligence, they will assess compensation plans, benefit plans, human resource information systems, training programs, compliance with various regulations, and employee-related litigation. During Integration Planning they will determine how to blend compensation and benefit plans. In many acquisitions, some employee positions are cut or made redundant. The senior HR executive will determine and manage severance plans. They orchestrate the process of notifying employees of the termination of their employment. They handle mandatory regulatory notifications, like warnings under the U.S. Worker Adjustment and Retraining Act. The VP HR will also coordinate dealings with international employee organizations such as European Works Councils.

Investment Bankers

Investment bankers are third-party agents that assist buyers or sellers in M&A transactions. Bankers work for either the buyer or the seller but not both. Often investment bankers introduce acquirers to potential acquisition candidates. Companies can also hire investment bankers to represent them in sale discussions. Sometimes bankers run an auction process where a seller tries to engage multiple buyers to maximize the sale price. Investment bankers serve as counselors to their clients, helping them to make the best possible decisions at each stage of the process. Investment bankers receive a retainer fee and a percentage of the final sale price. There may be bonuses for achieving certain goals like exceeding a target sales price or closing the deal in a short time frame.

Outside Legal Counsel

Outside Legal Counsel is often retained by a company’s General Counsel to assist in the transaction. They are experts in specific legal areas like drafting definitive agreements or obtaining regulatory approvals.

Valuation Consultants

Valuation consultants perform complex financial analyses. Valuing intangible assets is a common task. This is needed to determine how much accounting goodwill needs to be added to the acquirer’s balance sheet.

Public Relations Agency

Public Relations Agencies are often retained by the acquirer’s marketing organization to assist in message creation, media placements, and journalist interviews.

M&A Process

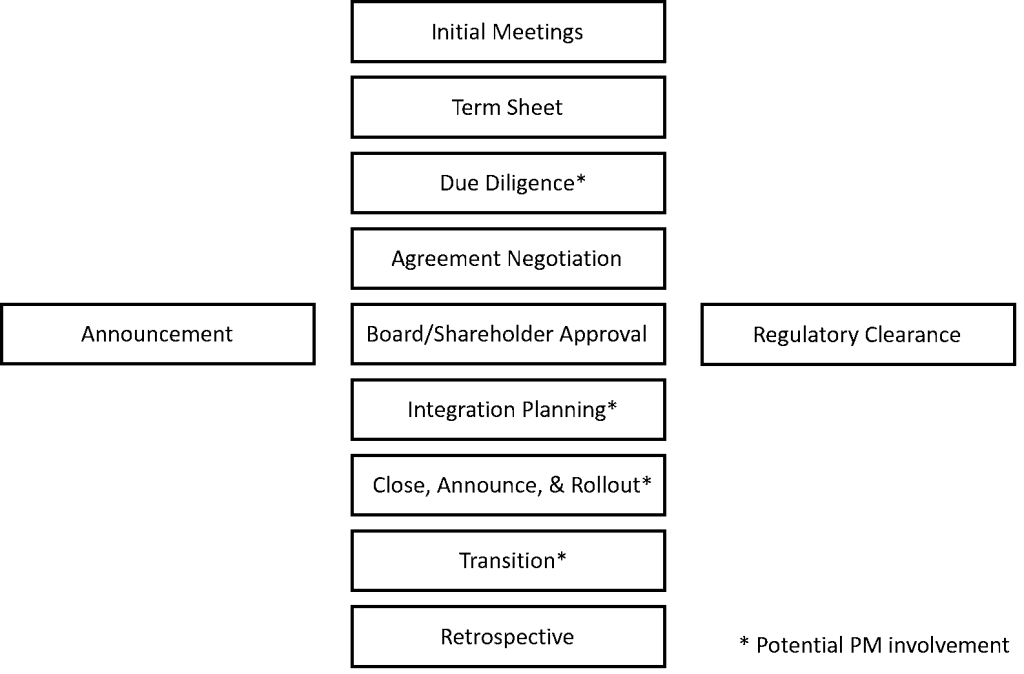

Most M&A projects follow a similar process. Some variations are depending on whether one or both of the companies is public and whether the deal requires regulatory approval. Unless they are actively involved in the deal team, product managers are usually only involved in a couple of the processes at most. Product managers should understand the overall process so they can properly prepare themselves and set the appropriate expectations with their team, peers, partners, customers, and prospects. The overall process looks like this:

Depending on the type of deal, not all steps are required. Here is a brief overview of each step in the process.

Initial Meetings

Most acquiring organizations have a process for developing their acquisition strategy. This involves identifying and analyzing potential acquisition candidates and monitoring market conditions. When the time is right, the first step is for the acquirer to approach a potential acquisition candidate. The CEO and the VP Corporate Development reach out and arrange an initial meeting. The purpose of these meetings is to explore whether there is an interest and fit between what the two companies are trying to achieve.

If one or more of the companies involved in the deal is public, then the chronology of these early meetings is disclosed in a proxy statement filed with the SEC. For example, check out page 95 of Sendgrid’s proxy statement that was filed in conjunction with its acquisition by Twilio in 2018.

Term Sheet

If the initial meetings are positive, the next step is for the acquirer to submit an initial offer that is often known as a term sheet. A term sheet is a non-binding offer that describes the significant terms and conditions that would govern the deal. Most potential acquires require some type of formal offer before they will commit to entering into formal acquisition activities. They want to be able to judge the suitability of a potential deal as well as the likelihood that the acquirer can execute and close the deal.

Due Diligence

The next step is for the acquirer to conduct legal, financial, and operational due diligence. Due diligence helps the acquirer understand the details of a target’s business as well as risks and opportunities. This information helps assess whether their initial offer is fair and that they can achieve the benefits of the acquisition.

Legal due diligence looks at matters like corporate organization, stockholders, contracts, litigation, and regulatory matters to name a few. Financial diligence focuses on the quality and accuracy of the target’s financial statements, financial systems, cash flow, debt agreements, etc. Operational due diligence focuses on a detailed understanding of a company’s operations – marketing, product management, development, operations, customer service, sales, professional services, human resources, and finance/administration. Product Managers are often involved in operational due diligence activities due to their intimate knowledge of markets, customers, roadmaps, competitors, etc.

Agreement Negotiation

The next step is to draft and negotiate the formal definitive agreements to implement the acquisition. These can include stock purchase agreements or asset purchase agreements. Often the drafting of these agreements occurs in parallel with due diligence. These are very detailed documents that cover every aspect and contingency of the deal. For example, you can check out the definitive agreement for SendGrid to be acquired by Twilio here starting on page 68.

Board/Shareholder Approval

The next step is for the board of directors and often shareholders to approve the deal. If both companies are privately owned, usually board approval is the only thing required. Sometimes lenders/debt holders also have to approve the deal. If one or both of the parties is public, then a shareholder vote is required in addition to the board approval. Usually, a special meeting is called and a formal proxy statement is filed with the SEC and sent to all shareholders of record. Depending on corporate by-laws, specific notice (often 30 days) is required before the shareholder vote can be held. If the deal requires regulatory approval, that approval must be obtained before holding the shareholder vote.

Regulatory Clearance

Many acquisitions, even between two privately held companies, must obtain regulatory approval before they can be completed. In the USA, the Hart-Scott-Rodino (HSR) Act governs mergers. If one of the parties to the merger has more than $50 million in annual revenue, HSR approval is required. Companies file a notification with the Federal Trade Commission that reviews it for antitrust concerns. Most requests are approved within 30 days. In rare cases, the FTC makes a ‘second request’ for additional information before approving the deal. In rare cases, the FTC will sue the companies in federal court to block the deal. Some deals involving foreign companies must also obtain national security clearance from the Committee on Foreign Investment in the United States (CFIUS). Deals involving UK operations or businesses require approval from the UK Competition and Markets Authority. Deals involving EU participants may require approval from the European Commission.

One regulatory matter product managers should be aware of is the Worker Adjustment and Retraining Notification Act (WARN Act). The WARN Act requires that employers provide workers with a 60-day notice of plans to terminate 50 or more employees from a location that employs at least 100 workers. California and 12 other states have their version of the WARN Act that imposes additional employer obligations. Some aggressive acquirers will issue WARN notices before the closing of a deal.

Integration Planning

This is the process the acquirer uses to plan how to merge the two companies. Product managers, because of their deep insight into products and markets, are often involved in integration planning activities. The integration process will depend a lot on how the acquirer plans to blend the two companies. Most integration planning activities consist of:

- Organization Chart & Roster Development

- Business Plan Development

- Transition Plan Development

- Separation Planning

- Announcement

- Transition Plan Management

An important aspect of integration planning is that it enables the management teams of both companies to get to know each other. Acquirers often use integration planning to indoctrinate the acquired company’s teams with their management system. A management system includes things like values, approaches to departmental organization, and even product management methodologies. Google’s approach is very different than Broadcom’s. Once they have learned about a pending acquisition or merger, product managers should investigate the acquirer’s management system. Check out Product Managers: How to Survive an Acquisition for more details.

Close, Announce & Rollout

Closing is the formal legal process of completing the acquisition. Depending on the deal, this can include the execution of definitive agreements, conducting a shareholder meeting, proxy vote, notification of appropriate governmental agencies/stock exchanges, and the disbursement of funds. This step is generally not held in public.

Concurrent with the closing the acquisition is rolled out to employees, shareholders, customers, partners, industry analysts, and the press. Generally, all-hands employee meetings are held after notifications to terminated employees are conducted. Individual organization and team meetings often help after the general all-hands meeting. Press releases are issued and industry analysts are briefed. Sometimes analysts are briefed before the rollout on an embargoed basis – they agree not to publish anything until the public rollout date.

Transition

Transition is the process of executing the changes required by the integration. This includes mundane things like updating company signage and websites, transitioning employees to new benefit plans, updating security badges, etc. Sometimes the activities are more significant like closing office locations, divesting non-core businesses, etc. Some employees might not have been selected to continue employment with the new company, but are retained for some time to transition their responsibilities to other employees.

Retrospective

60 to 90 days after the completion of the acquisition a post rollout assessment or retrospective is often held. The goal of this assessment is to identify what worked, what did not work, and how the process can be improved for the next acquisition. There is an old saying that “No battle plan survives the first contact with the enemy”. The same is true for acquisitions. Detailed planning and experience can help, but there are so many moving parts in an acquisition that there are always opportunities to improve. If you need to brush up on your financial literacy basics, check out the following articles:

- Why Should Product Managers Care About Income Statements?

- Why Should Product Managers Care About Balance Sheets?

- Why Product Managers Should Care About Cash Flow Statements

The M&A Model

Almost all acquisitions involve what is euphemistically called “The Model”. The model is a Pro-forma financial plan that includes a P&L, Balance Sheet, & Cash Flow Statement for the combined companies. It reduces all of the assumptions the acquirer has into traditional financial statements that everyone can understand. The Model is also used to determine whether an acquisition would be accretive or dilutive to earnings at specific purchase prices An initial version of the Model is built after the first set of management meetings. It is refined as the acquirer moves through the acquisition process. Acquirers are constantly testing their assumptions to improve model accuracy. For public companies, the model is used to provide formal guidance to stock analysts.

The details of The Model are rarely shared outside of a few very senior executives. Product managers rarely see it. Yet, The Model will describe what revenues are expected, what operating costs will be needed, and what profit expectations are. His can result in an increase or decrease in investments in specific product lines. It can also impact headcount. The Model will describe how product management will be organized and staffed in the new combined organization. It will describe what products will be divested or even retired.

Product Manager Acquisition Do’s and Don’ts

Acquisitions represent significant change and that can be uncomfortable for a lot of people. Change management professionals call the time between when an acquisition is announced and it closes the ‘valley of death’. Productivity drops and team members stress out over what changes the deal will bring to them. Based on experience there are some definite Do’s and Don’ts during this difficult time:

Do’s

- Accept that you are not in control. It is difficult, but as a product manager, you have little control over the acquisition process. You can just control how you choose to behave and react.

- Learn about the acquirer and its history. Spend some time doing basic research about the acquirer. You will find things you like and things you dislike. Most successful acquirers know that while they need to imbue their culture in the acquired company, they also must learn how to adopt the best of what the acquired company has into their company.

- Understand and support the process. Learn what you can about the planning and integration process. Provide whatever support is asked for in a timely and professional manner.

Don’ts

- Break confidentiality of the integration process. If you are fortunate to be invited into the integration planning process never, ever, break the confidentiality of those activities. While you may be tempted to tell your friends what you are learning about strategy changes or job cuts, don’t. More than one employee has been abruptly terminated as a result of breaking confidentiality.

- Speculate about job cuts. While it may be tempting, do not speculate about potential job cuts. Integration planning exercises are fluid processes and things can change up to the last minute.

- Spread rumors. Rumor mongering between the time an acquisition is announced and it closes is almost a national sport. Spreading rumors will just serve to upset people. When you are not in control of a process it is natural to be frustrated by a lack of information.

- Post negative items on social media. Venting on social media is a common thing, but doing it during an acquisition is almost a sure-fire ticket to get put on the “Cut” versus “Keep” list. A classic example of this is the infamous Cisco Fatty story.

Summary

The pace of mergers and acquisitions in the tech market is setting new records. Acquisitions are challenging times for product managers. On the one hand, they can provide an opportunity for career growth. They can also result in the elimination of a product manager’s job. Product managers should learn the basics of M&A. They need to understand M&A Roles & Responsibilities, the M&A Process, the Model that governs M&A, and the definite do’s and dont’s.