Product Managers Should Understand SaaS Revenue Basics

Understanding the dynamics of SaaS product revenues can be hard. Complex price plans, usage limits, overage charges, and seasonal variations introduce complexity. Product managers typically have limited access to monthly billing revenue data. It is hard for product managers to make fact-based decisions without revenue data. Product Managers Should Understand SaaS Revenue Basics.

SaaS Revenues Can Be Deceiving

SaaS revenue trends can be deceiving. The complexities of monthly billings, revenue recognition, deferred revenue, complex pricing plans, and seasonal business variations make what appears to be simple, complex.

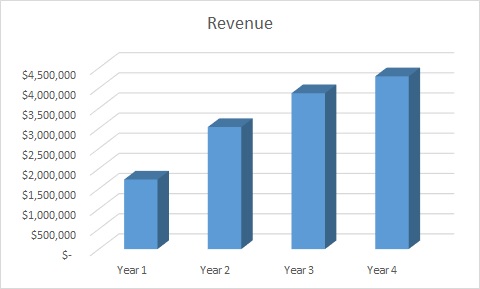

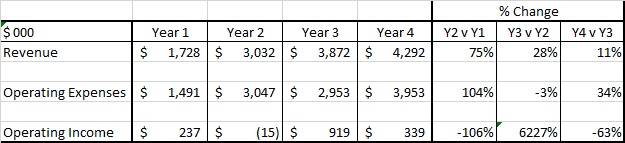

Last year I was asked by an investor to take a quick look at a SaaS product line. In less than four hours I discovered some disturbing things. On the surface, the product showed some potential:

A closer look showed that it had some challenges:

The revenue growth was good to begin with, but it was tapering off. The operating expense and income trends were confusing. If you need to brush up on your product management income statement analysis check out Why Should Product Managers Care About Income Statements?

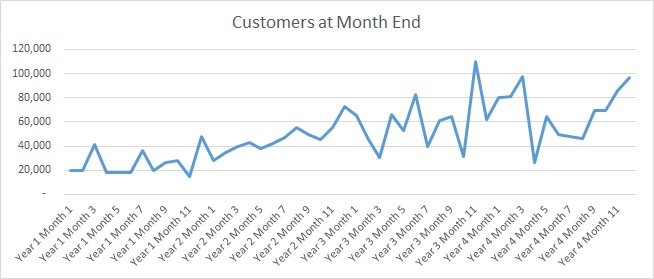

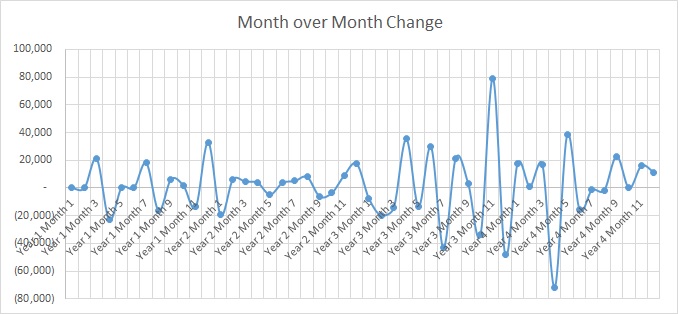

I asked for monthly customer data. What I received was troubling:

While the total customer count was growing, the monthly changes were huge:

Discussions with management revealed that customers had a short life expectancy. They would use the product for a month or two and then cancel. The company used Google Ads to drive new signups.

This is an example of some of the complexities that product managers face with SaaS revenues

Product Management SaaS Revenue Basics

Product managers should start with understanding some SaaS revenue basics. This includes things like how revenue is reported on a P&L, ASC 606, and revenue flux analysis.

SaaS Revenue on the P&L

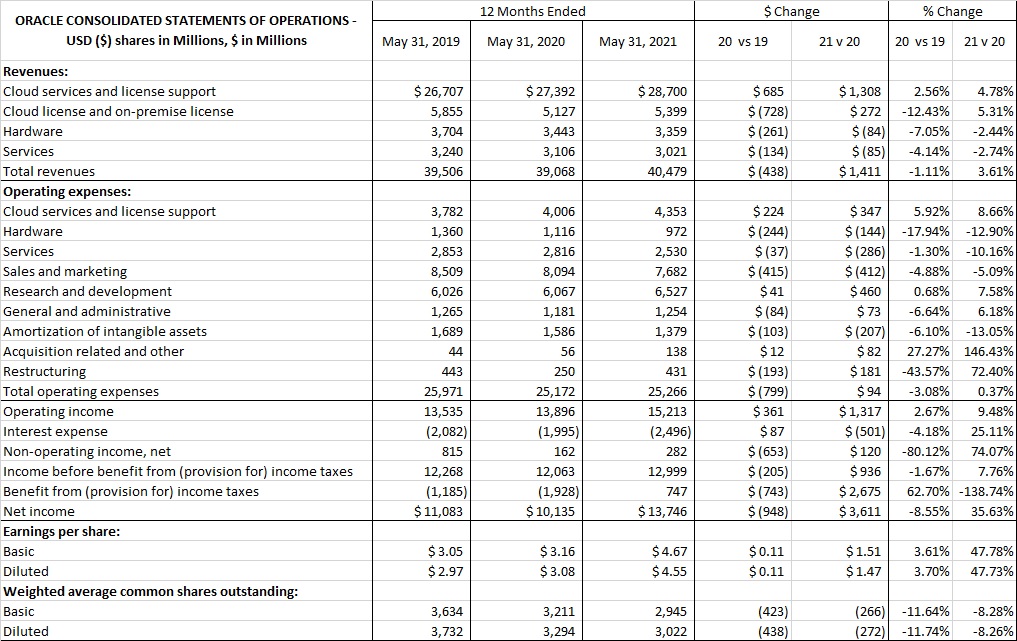

Revenue is the first thing reported on a P&L (aka Income Statement). Here is Oracle Corporation’s Income Statement from the last fiscal year as an example.

Revenues are the first component. Revenues are the sales that are recognized in a specific period. Oracle reports four types of revenue: cloud services and license support, cloud license and on-premise license, hardware, and services. Cloud services and license support are subscription revenues that are paid monthly or annually. Cloud license and on-premise license are perpetual licenses that are paid upfront. This was the normal business practice pre-SaaS. Hardware is the Sun Microsystems product line. Services are the professional services and training that Oracle offers its customers.

Product managers should understand the concept of revenue recognition and how it impacts their products. Revenue recognition is when a company can include specific sales transactions in its Income Statements. Consider a SaaS company whose fiscal year ends on December 31st. They sell an annual SaaS subscription to a customer in June for $120,000. The customer prepays the entire amount in July. The company is only allowed to ‘recognize $60,000 in the current fiscal year ($10,000/month). The remaining $60,000 will be recognized in the next fiscal year. As a result, the product manager’s product line will only get credit for the revenue recognized in the current fiscal year. This could impact their bonus among other things.

Revenue recognition is governed by the standards set by the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB). The specific policy is known as ASC 606 Contracts with Customers. ASC 606 not only deals with revenue recognition but expense recognition. This impacts a company’s profitability. AC 606 was initially launched in 2016 and all companies had to comply by 2020.

In the Oracle Income Statement, the cloud services and license support revenue line is an example of subscription revenues impacted by ASC 606. License support is what used to be called software maintenance revenue. These are services like customer support and software upgrades for on-premise licensed software like Oracle DBMS. Cloud license and on-premise license revenue cover perpetual licenses sold to customers. This was the industry standard pre-SaaS. These revenues are usually recognized all at once. Hardware revenues are similar. Services revenues are recognized as they are delivered.

To brush up on your P&L basics check out Why Should Product Managers Care About Income Statements?

ASC 606

ASC 606 Contracts with Customers. is the revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services – public, private and non-profit entities. Both public and privately held companies should be ASC 606 compliant now. In the past, revenue recognition standards differed between the generally accepted accounting principles (GAAP) in the United States and the global provisions set by the International Financial Reporting Standards (IFRS). It was universally acknowledged that these rules needed to evolve due to varying ways they were being applied and loopholes they created, so the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) launched a joint initiative to better align these standard practices globally, which resulted in the 2014 publication of the new “Topic ASC 606: Revenue from Contracts with Customers”. ASC606 started being implemented in 2016, by 2020 al companies had to comply

Basic revenue recognition is similar, but now there are more complicated requirements for handling items like Post Contract Support (PCS), setup/customization fees, variable considerations like Service Level Agreement bonuses and penalties. Check out this excellent primer from PWC on the differences between GAAP reporting and ASC 606 reporting.

On the expense side, Incremental costs of obtaining a contract (commissions, etc.) ae handled differently than under GAAP/IFRS. Commission expenses can continue to be recognized when incurred if the determined amortization period is one year or less. Commission expenses must be amortized for individual reps over the anticipated life of the customer if the contract is longer than one year, but any indirect or rolled commissions for supervisors/managers will continue to be recognized immediately regardless of the determined contract term length. Every time the existing rep or other rep sells to the customer again, you must evaluate if that extends the life of the customer or servicing existing life expectancy. For each additional commission calculated and paid, you must be able to quantify the impact their action did to further that customer for commission expense amortization considerations.

The practical implementation of ASC 606 results in higher profitability for most products due to the longer-term amortization of incremental costs of obtaining a contract. Revenue is generally not affected since under GAAP and IFRS revenue recognition was tied to when the service was delivered. In the case of prepays, like a prepaid annual subscription, the cash payment was recorded as deferred revenue and then recognized month by month.

ASC 606 is a complicated topic that I usually beyond the scope of most product managers’ training. They should work closely with their finance team to understand how ASC 606 has impacted the P&L of their products. Check out Why Product Managers Should Become Best Friends with Finance Team

SaaS Revenue Flux

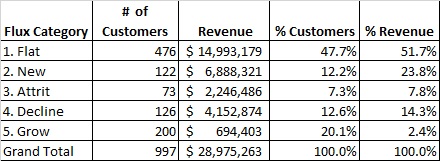

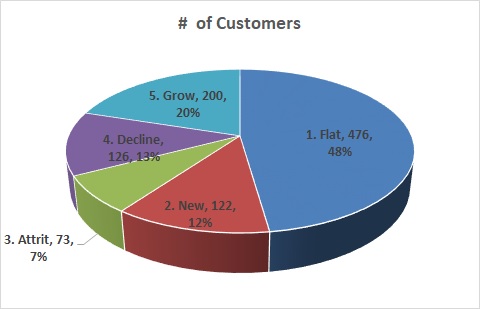

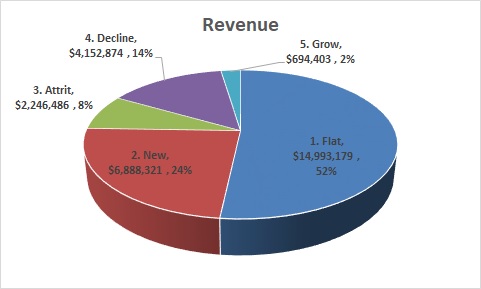

SaaS revenues fluctuate monthly. New customers come on board and existing customers quit. If the SaaS product’s pricing plan includes some type of a metered component (# of users, # of transactions, etc.) monthly billings could go up or down. Or just stay flat. Deciphering the trends is important for product managers. There are five flux categories:

- Flat. Month to month billings are the same

- New. New customer added in a month

- Attrit. Customers who left in a month and had no billings

- Decline. Customers whose billings declined in comparison to the prior month. This could be due to some change in a metered component (Users, Transactions, etc.)

- Grow. Customers whose billings grew in comparison to the prior month.

Let’s look at some examples: This table summarizes the SaaS flux analysis for a product:

Here are some graphs that help illustrate it a bit better:

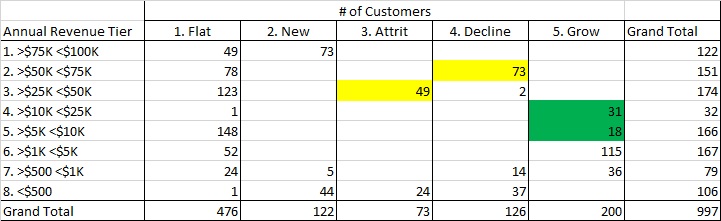

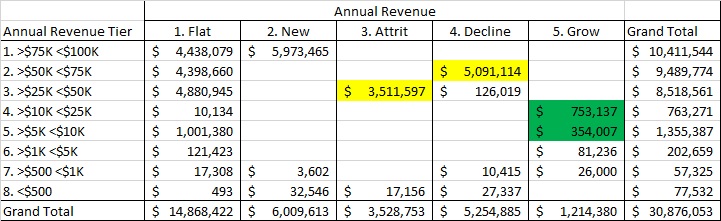

You can extend the analysis by adding in revenue tiers:

This type of analysis helps product managers to zero in on customers whose behavior they should understand better.

Product Managers Need to Understand Why

Product managers need to understand the reasons why flux is occurring in their product lines. The best way to do that is through qualitative interviews with customers (aka Win/Loss Analysis)

Win/Loss interviews provide an opportunity to dive deeply into the reasons behind customer decisions. They can provide the qualitative data you need to develop effective strategies and tactics to counter customer churn. In a typical project, a subset of customers who have dropped your solution and those who have decided to renew is selected. You can also explore customers whose usage has either significantly increased or decreased. Next, an interview guide is developed to help script calls with these customers to ensure that all appropriate bases are covered. Next, customers are recruited to participate in the process. Generally, the salespeople that were involved in the initial deal or renewal are encouraged to help get customers to participate in the project. Sometimes an incentive like a $25 or $50 gift card is used as a reward for participating in the process. Ideally, 30 to 40 calls are arranged to provide enough of a sample set to derive real results. Experience has shown that only one in four contacts end up agreeing to participate in Win/Loss calls. For more information about conducting qualitative interviews heck out Win-Loss Analysis: Process & Lessons Learned

Product Management SaaS Revenue Data Challenges

Most product managers face significant challenges when it comes to SaaS revenue data. Some companies have sophisticated applications like SaaSOptics, Recurly, or Chargebee. Solutions like these incorporate sophisticated subscription billing, payment gateways, and analytics. They ensure a SaaS vendor can report ASC 606 compliant numbers.

Many companies don’t have these types of purpose-built solutions. They rely on their existing accounting systems and homemade solutions using Excel.

In either case, product managers often do not have access to the data. It is often considered to be proprietary and confidential. Only executives, finance team members, and board members have access. There are concerns that product managers would leak the information to outside parties.

When faced with these challenges, creative product managers use proxies to approximate SaaS product revenue trends. A proxy uses data a product manager has access to estimate what the actual product revenue data trends are. For example:

- Salesforce Automation Data. Analytics data from tools like Salesforce.com or Keap can provide information about customer wins and customer expansions.

- Customer Support Data. Customer support applications like ZenDesk, SAP Service Cloud, or Orale Service can also provide data about new customers

- In-App Analytics. Product managers can instrument their applications to provide helpful information like free to paid subscription conversions, usage data, etc.

Proxy data is not as good as actual revenue data, but over time product managers can learn how to leverage it to make better decisions to drive revenue, retention, and customer satisfaction.

Summary

Rich SaaS Revenue data can enable a product manager to make better fact-based decisions about priorities and marketing/sales programs. Understanding the basics of ASC 606 revenue accounting is important. Understanding why customer revenues grow, decline, or cancel is critical. Many product managers do not have access to actual SaaS product revenues. There are proxy techniques they can use to approximate what the actual data looks like.