Product Managers: Q3 is Ending. Are you Going to Miss Your Bonus Again?

As the third quarter draws to a close, many product managers are asking themselves “Am I going to miss my bonus again?” Product manager incentive compensation is always a tricky thing. Product managers have responsibility but rarely have authority. It is hard for them to directly influence events and performance. As a result, it is hard to ensure the achievement of bonus targets. By the end of the third quarter, most product managers know where they are going to land in regards to their annual bonus. What can they do so that the pattern of missing their bonus is not repeated?

Product Manager Incentive Compensation

Product management is a well-paying job. Salar.com reports that mid-level product managers in the U.S. earn on average $90,000 in base salary and $6,6450 in bonuses in 2021. An annual survey from the Pragmatic Institute broke down the typical factors to calculate a bonus:

Factors for Calculating Bonus (% Bonus Eligible PMs Reporting)

- Average Bonus: $14,800 (14% of base salary)

- 89% Company Revenue/Profit

- 61% Personal Objectives

- 34% Product Revenue/Profit

- 5% Market Visits

- 9% Other

Around 60% of product managers are eligible to receive some type of equity, like stock options or restricted stock units. The reality is that the days of hitting the stock option lotto are gone. Check out The Liquidation Preference Effect -Your Equity Could Be Worth Millions — Or Nothing. It does a great job of describing the reality of equity compensation in today’s market.

As noted in The Challenges of Product Manager Incentive Compensation some challenges include:

- Low Leverage. When only 15% of compensation is ‘at at risk’ there are not many reasons for product managers to excel.

- Total Incentive is Capped. Bonus are most often ‘capped’—they cannot exceed a fixed amount of percentage of base salary. Typical product managers cannot overachieve their targets and get higher incentive payouts.

- Bonus Factors are not Aligned with Other Bonus Eligible Employees. Product manager bonus awards are often not aligned with incentive compensation for executives or sales.

For most product managers, sales incentive compensation has a more direct impact. Consider the following incentive compensation plan for a SaaS senior account executive. Here are a couple of key observations:

- Leverage. Base salary only accounts for 55% of the total compensation of on-target earnings. A significant part of a sales rep’s compensation is at risk and dependent on performance

- Incentive Compensation is not Capped. There is no cap on incentive compensation. If a sales rep exceeds quota they keep getting incentive payments

- Commission Rates Rise with Over-Performance. Commission rates are often tiered, but only once the quota has been achieved. Commission rates increase to 15%, almost double the rate for the first tier. Getting into ‘accelerators’ can drive significant sales performance

- SPIFFs. The SPIFF for financial institution wins is an indication that the enterprise values new financial institution wins, but only to a certain degree.

Product managers often face the need to accommodate the priorities of high-performing salespeople. As the comp plan illustrates, salespeople have significant incentives to overachieve. If winning a deal requires the delivery of a customer-specific feature, the salesperson will apply pressure on the product manager to deliver it. A promise that the feature will be delivered in the future will not suffice. Agile practices also introduce challenges. The re-prioritization of backlog items to accommodate sales priorities is common and encouraged. Product managers that disappoint top-performing salespeople can suffer significant career advancement risks.

The Second Half Syndrome

Product manager bonuses are nice, but definitely are not a ‘must have’ for most product managers. A 10% base salary bonus could pay for a nice trip with your family, a new toy (PC, Roomba, whatever), or let you dabble in cryptocurrencies like Bitcoin, Ethereum, or even Dogecoin.

Product managers are like any other bonus-eligible employee. They will bust their butts to achieve the goals set for them. By the end of September, they should have a pretty good idea of where they will end up for the year. If they are going to miss their bonus targets once again, the ‘second half syndrome’ can set in. The second half syndrome is that once you realize all of your extra efforts are not going to pay off in a bonus, you relax a bit. Why bust your ass when you don’t stand a chance of getting paid this year? Salespeople suffer the same fate. Once they realize they are not going to make quota this year, they slow deals down a little bit so that they slip into the next fiscal year. That way they can get off to a good start and have a better shot at beating quota next year.

Revenue is the Solution to All Problems

I worked for Sterling Williams, the CEO of Sterling Software, for a number of years.I was a senior executive in one of the four main groups that made up Sterling Software. My group, a $350 million business, consisted of two product divisions and three international sales and support divisions. Every year we would sit down with Sterling and negotiate our annual plan for the next fiscal year. We had targets for revenue, operating profit, and earnings per share. Our substantial bonuses were tied to achieving these goals. The final numbers were used to provide guidance to Wall Street analysts. A significant portion of our personal wealth was tied up in Sterling stock and options. We were very motivated to achieve and exceed our annual targets.

Inevitably during the process, we would disagree. Sterling wanted higher numbers and we wanted lower numbers. Almost on cue Sterling would say “Revenue solves all problems.” If you could generate the revenue, you could manage to hit the operating profit and EPS targets. He had a way of simplifying things down to tier very basic nature.

The majority of product manager bonus factors can be tied back to increasing revenues. Product line revenues are an obvious target. Annual recurring revenue (ARR) and Monthly Recurring Revenues are as well. Net Dollar Retention is another. Operating profit comes from revenues. Indirect measures like Monthly Active Users, Custome Acquisition Cost, and Life Time Value all derive from revenue one way or another. If you can grow revenues, you should be able to hit your bonus targets.

SaaS Revenues Can Be Deceiving

SaaS revenue trends can be deceiving. The complexities of monthly billings, revenue recognition, deferred revenue, complex pricing plans, and seasonal business variations make what appears to be simple, complex. Product managers should understand how SaaS revenues work.

A Product Management SaaS Revenue Case Study

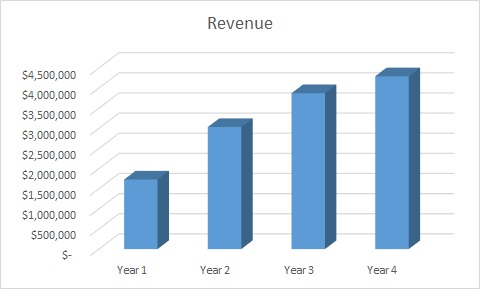

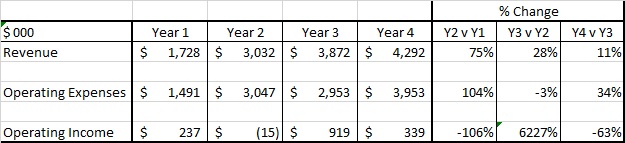

Last year I was asked by an investor to take a quick look at a SaaS product line. In less than four hours I discovered some disturbing things. On the surface, the product showed some potential:

A closer look showed that it had some challenges:

The revenue growth was good, to begin with, but it was tapering off. The operating expense and income trends were confusing. If you need to brush up on your product management income statement analysis check out Why Should Product Managers Care About Income Statements?

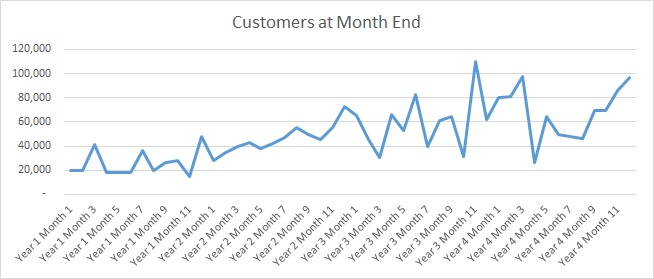

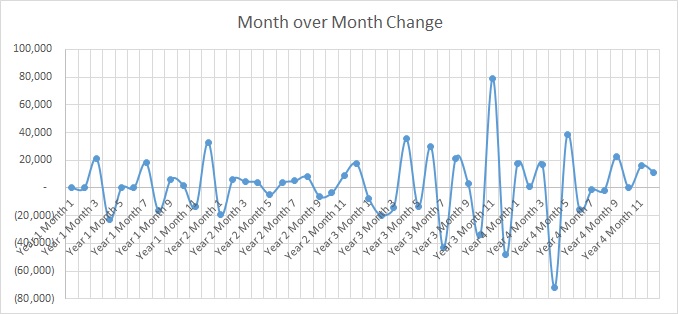

I asked for monthly customer data. What I received was troubling:

While the total customer count was growing, the monthly changes were huge:

Discussions with management revealed that customers had a short life expectancy. They would use the product for a month or two and then cancel. The company used Google Ads to drive new signups.

This is an example of some of the complexities that product managers face with SaaS revenues

SaaS Revenue on the P&L

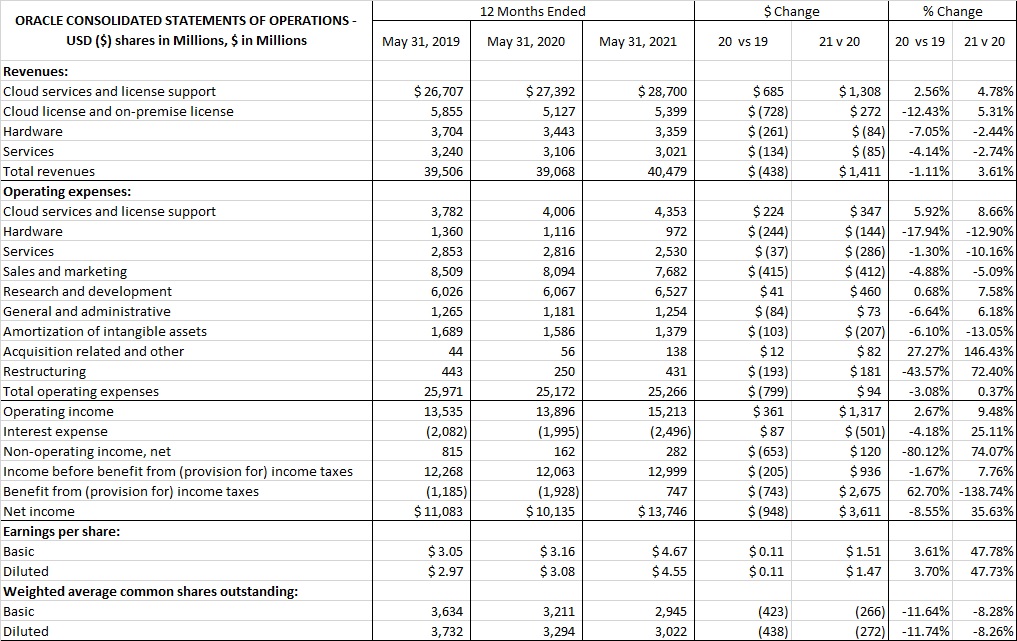

Revenue is the first thing reported on a P&L (aka Income Statement). Here is Oracle Corporation’s Income Statement from the last fiscal year as an example.

Revenues are the first component. Revenues are the sales that are recognized in a specific period. Oracle reports four types of revenue: cloud services and license support, cloud license and on-premise license, hardware, and services. Cloud services and license support are subscription revenues that are paid monthly or annually. Cloud license and on-premise license are perpetual licenses that are paid upfront. This was the normal business practice pre-SaaS. Hardware is the Sun Microsystems product line. Services are the professional services and training that Oracle offers its customers.

Product managers should understand the concept of revenue recognition and how it impacts their products. Revenue recognition is when a company can include specific sales transactions in its Income Statements. Consider a SaaS company whose fiscal year ends on December 31st. They sell an annual SaaS subscription to a customer in June for $120,000. The customer prepays the entire amount in July. The company is only allowed to ‘recognize $60,000 in the current fiscal year ($10,000/month). The remaining $60,000 will be recognized in the next fiscal year. As a result, the product manager’s product line will only get credit for the revenue recognized in the current fiscal year. This could impact their bonus among other things.

Revenue recognition is governed by the standards set by the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB). The specific policy is known as ASC 606 Contracts with Customers. ASC 606 not only deals with revenue recognition but expense recognition. This impacts a company’s profitability. AC 606 was initially launched in 2016 and all companies had to comply by 2020.

In the Oracle Income Statement, the cloud services and license support revenue line is an example of subscription revenues impacted by ASC 606. License support is what used to be called software maintenance revenue. These are services like customer support and software upgrades for on-premise licensed software like Oracle DBMS. Cloud license and on-premise license revenue cover perpetual licenses sold to customers. This was the industry standard pre-SaaS. These revenues are usually recognized all at once. Hardware revenues are similar. Services revenues are recognized as they are delivered.

To brush up on your P&L basics check out Why Should Product Managers Care About Income Statements?

ASC 606

ASC 606 Contracts with Customers. is the revenue recognition standard that affects all businesses that enter into contracts with customers to transfer goods or services – public, private and non-profit entities. Both public and privately held companies should be ASC 606 compliant now. In the past, revenue recognition standards differed between the generally accepted accounting principles (GAAP) in the United States and the global provisions set by the International Financial Reporting Standards (IFRS). It was universally acknowledged that these rules needed to evolve due to varying ways they were being applied and loopholes they created, so the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) launched a joint initiative to better align these standard practices globally, which resulted in the 2014 publication of the new “Topic ASC 606: Revenue from Contracts with Customers”. ASC606 started being implemented in 2016, by 2020 all companies had to comply

Basic revenue recognition is similar, but now there are more complicated requirements for handling items like Post Contract Support (PCS), setup/customization fees, variable considerations like Service Level Agreement bonuses, and penalties. Check out this excellent primer from PWC on the differences between GAAP reporting and ASC 606 reporting.

On the expense side, Incremental costs of obtaining a contract (commissions, etc.) ae handled differently than under GAAP/IFRS. Commission expenses can continue to be recognized when incurred if the determined amortization period is one year or less. Commission expenses must be amortized for individual reps over the anticipated life of the customer if the contract is longer than one year, but any indirect or rolled commissions for supervisors/managers will continue to be recognized immediately regardless of the determined contract term length. Every time the existing rep or other rep sells to the customer again, you must evaluate if that extends the life of the customer or servicing existing life expectancy. For each additional commission calculated and paid, you must be able to quantify the impact their action did to further that customer for commission expense amortization considerations.

The practical implementation of ASC 606 results in higher profitability for most products due to the longer-term amortization of incremental costs of obtaining a contract. Revenue is generally not affected since under GAAP and IFRS revenue recognition was tied to when the service was delivered. In the case of prepays, like a prepaid annual subscription, the cash payment was recorded as deferred revenue and then recognized month by month.

ASC 606 is a complicated topic that I usually beyond the scope of most product managers’ training. They should work closely with their finance team to understand how ASC 606 has impacted the P&L of their products. Check out Why Product Managers Should Become Best Friends with Finance Team

Why is Understanding SaaS Revenues Important for Product Managers?

Most product management bonuses are tied directly to or derived from SaaS revenues. Product managers need to understand how the business looks at and reports on revenues. A challenge product managers face is that SaaS revenues are recognized as subscription revenues. They are recognized on the P&L one month at a time. In the pre-SaaS days, license revenues were recognized all at once. If a deal closed on December 30th, they could recognize it all in December. In the SaaS world, they could not recognize anything – it would all be recorded as deferred revenue. One month would be recognized at the end of January. In the ‘old days’ many sales reps made their entire quota off of one or two deals in December. These elephant hunters lived and died by the big deal. Even in the SaaS era, salespeople are often compensated on Total Contract Value – the sum of all non-cancellable payments a customer commits to. Product managers are usually only bonuses on recognized revenue.

How Can Product Managers Drive Revenue

Product managers can drive more revenue for their products. To start, product managers should understand SaaS revenue basics at their company. Check out Product Managers Should Understand SaaS Revenue Basics. There are two ways product managers can drive revenue: Optimizing Current Revenue Streams and Innovating New Revenue Streams.

Optimize Current Revenue Streams

These tactics may bring some short-term benefit but probably won’t drive so much improvement that you’ll make your bonus targets this year. The math of subscription revenue recognition is tough. You can’t make up for poor performance early in the year by a blitz at the end of the year. But you can lay the foundation for next year’s success. Here are three tactics you can consider.

1. Optimize Demand Generation Programs

Armed with the knowledge gained from Tiering, Money Wheel and Win-Loss Analysis re-examine your current demand generation programs. Look at the segments of the market where you are succeeding and double down on the investments you are making to target them. Add more ad spend, more webinars, more events/conferences, more thought leadership blog pieces. Conversely, look at areas where you are not succeeding. Experiment with eliminating investments in demand generation that target those segments. The risk is not too high – those segments are not producing significant revenues for you anyways.

2. Re-evaluate Pricing & Packaging

In a mature business, a significant part of MoneyWheel transactions will involve Expansion and Add-on sales. Pricing and packaging can have a major impact on sales in these areas. Win-Loss Analysis can help confirm customers’ acceptance or rejection of your pricing and packaging policies.

An interesting story from a Win-Loss Analysis project helps confirm this. A SaaS company that offered a solution for marketing automation was concerned that customers were not upgrading from their entry-level package to the standard enterprise package. Pricing was based on what feature set the customer selected and the volume of transactions processed by the platform every month. In the entry-level offering, customers were allowed 10,000 transactions a month for a flat fee. Anything over 10,000/month resulted in an overage fee. The enterprise edition offered more features and more transaction tiers/prices based on usage. The company had a built-in lead generation system – when an entry-level customer exceeded their 10,000 transactions/month usage for more than two months, it triggered an alert to the sales. The rep to reach out to the customer and offer an upgrade to the enterprise package. On the surface it makes sense, the customer obviously saw value in the solution and the enterprise package should give them a bigger bang for the buck. Unfortunately, the customers strongly resisted upgrading.

Win-Loss Interviews revealed why. When customers have presented the enterprise package the cost was anywhere from five to ten times more than they were spending today. The enterprise package also included eight new premium features that were not available in the standard package. Customers had two problems with the enterprise upgrade proposals. First, almost all of them did not find significant value in the newly available features. Second, the volume tiers in the enterprise package were so huge even the largest users of the standard package could never consume them, even if they tripled their current volume. Customers simply did not see the benefit from spending five to ten times what they were spending today. Instead what most customers did was ration the use of the product so they would not incur significant overage fees. The company’s pricing and packaging strategy actually encouraged customers to use and spend less. It opened the door for competitors to come in and offer commoditized pricing and steal-away customers.

3. Focus on Repeatable, Scalable Sales Transactions

Money Wheel Analysis when combined with sales region and sales rep quota performance can give you insights into why the most successful reps are winning and why the lowest-performing reps are struggling. Sales management and sales rep performance are complicated topics. Most sales teams have top performers, average performers, and low performers. Performance can vary across territories and countries. Some sales reps are innately more talented than others. You can use the information you developed in your baseline analysis in two ways. First, you can understand why specific reps are having significantly more success in selling certain types of transactions than others. Is their territory richer in prospects that respond to these types of sales transactions? Or do they have an approach and process that resonates especially well? Understanding how to replicate the success of the best sales reps across the entire sales force. This is one of the most productive investments you can make.

You can also look at sales reps that are struggling. While some reps just are not good at sales, most performance problems can be traced to gaps in knowledge and experience. For example, if the Money Wheel Analysis shows that a rep has not done any financially driven deals while the best reps achieve 40% of their quota from these deals, it is usually a knowledge/experience issue versus sales incompetence. By sharing your Money Wheel Analysis with the sales force and reaching out to the underperforming reps you can help them improve their performance and results. A rising tide lifts all boats and more revenue will help you get closer to achieving your bonus.

Innovate New Revenue Streams

Optimizing existing revenue streams can only yield so much incremental revenue. It is important to start with optimization strategies since they tend to yield increased revenue sooner and at a lower risk. For mature software companies (>5 years old), the next step is to look at structural changes. These changes can include new add-on products, expanding to new geographic markets, or competitive steal-away programs based on price commoditization.

1. Add-On Products

The first strategy is to consider developing a new add-on product that complements your core product. Through the use of open-source software components and Agile development techniques the time and cost to deliver a Minimal Viable Product is a fraction of what it was five years ago. While a new product will not solve your bonus problems this year, it can lay the foundation for long-term success. New product development always is risky. Companies with a portfolio of existing products are often loathe to take the risk of new product development. Past experiences that have failed are often a barrier as well.

The paradigm of Minimal Viable Products is a potential game-changer for mature organizations. It can also provide a boost of energy for marketing, sales, and development teams. Given the relatively low cost of developing an MVP that can be cross-sold into your existing customer base, it is a risk worth taking.

2. New Geographic Markets

International expansion is critical for every software company. International expansion is almost always required for a company to scale beyond $50 million in revenue. As noted in American Product Managers Should Live Overseas for a While

A Senior Vice President who ran my company’s international operations had a famous quote “We have more in common than what divides us.” In general, you will find that international customer business processes have similar challenges and opportunities as their American counterparts. The process to sell and deliver just-in-time bumpers for Mercedes cars in Germany is similar to the process they use in Tuscaloosa, Alabama. A master purchase order is negotiated, a purchase order release is sent with that day’s quantity requirements, the vendor confirms the shipment with an advanced shipping notice, the truck shows up at the right dock at the right time with the bumpers, a shipment receipt is generated, the vendor generates an invoice, Mercedes checks the shipment receipt and the purchase order release and sends an electronic funds transfer to pay for the bumpers. The only material difference is that in Germany the documents are exchanged using the EDIFACT EDI standard, in Alabama they use the X12 EDI standard.

American Product Managers Should Live Overseas for a While

Beginning international expansion or moving into new geographies is not a short-term proposition. While it is easier today to internationalize a SaaS application in comparison to the old days of on-premise software, there is a lot more that is required to be successful. Your company needs to build marketing, sales, enablement, and support infrastructure to serve international customers. In certain geographies like the U.K., India, and Australia/New Zealand you can get away with an American English version of your product and English-speaking marketing, sales, and support personnel. In other geographies like Germany, France, Spain, Italy, and Russia you will eventually have to take the plunge and build a business infrastructure with people that can speak the local language. Again, international expansion is important, but it is a long-term strategy.

3. Competitive Steal-Away

A third strategy is to focus on competitive steal away. In most mature markets (Early/Late Majority in the TALC) there are multiple competitors chasing the same customer opportunities. Your competitor’s customer bases are prime opportunities for you. These customers have already seen the value of investing in solutions like yours to address their business needs. If they saw value in a competitor’s solution, they should see value in your solution as well. A radical strategy is to consider commoditizing the price of your offering to steal away your competitor’s customers.

In most mature markets price eventually becomes an issue. Solutions that address the same business problem usually end up with prices that are at least in the same order of magnitude as each other. Assuming that the cost of migrating from a competitor’s solution to yours is not too cost-prohibitive, you can use price as a tool to steal away your competitors’ customers. Almost all markets commoditize eventually. Some examples are the cost of long-distance telephone calls or mobile phone minutes. CPU processing power is another example. The impact of Netflix on cable TV subscriptions is a third example.

For SaaS companies, you need to understand the unit economics of delivering revenue on your platform. Most companies have a lot of surplus capacity in their infrastructure. The costs of adding another ten, twenty, or hundred customers are minimal. You can use the same infrastructure and same enablement, support, and operations personnel that you use to service your existing customers. Therefore, adding incremental revenue is almost cost-free. You can continue to do this until you hit an inflection point where you need to add material amounts of new costs to service the revenue.

While you are in this zone the price you charge for the service is almost irrelevant. This gives you an opportunity to commoditize and decimate your competition. You can lower your price by 50% and steal your competitors’ business. Customers that use a solution only switch to a competitive solution for a few reasons. One reason is that there has been a serious performance issue such as frequent and prolonged outages. Another reason is cost. If the cost of a comparable competitive solution is a fraction of the current solution, there can be a compelling economic reason to make a change. The risk of making the change, however, has to be minimal. There can be no hiccups or surprises during the migration.

This is a radical solution to your stalled revenue growth challenges. Changing the price economics carries both significant risks but opportunities as well. This strategy works best when your agreements with customers are not month-to-month but have some fixed term, like 12 or 24 months. In this type of situation, your existing customers are locked into their contracts and pricing. You can pillage your competitor’s customer base while not risking too much damage to your own customer base. Eventually, your existing customers will come up for renewal and they will expect to get price concessions similar to what you offered the ‘steal away customers. But you will have enjoyed the benefit of the incremental revenue in the interim which was the goal of the exercise.

Price commoditization eventually comes to all competitive software markets. History has shown that the first market player to commoditize pricing can enjoy outsized benefits.

Summary

As the third quarter draws to a close, many product managers are asking themselves “Am I going to miss my bonus again?” Product manager incentive compensation is always a tricky thing. Product managers have responsibility but rarely have authority. It is hard for them to directly influence events and performance. As a result, it is hard to ensure the achievement of bonus targets. By the end of the third quarter, most product managers know where they are going to land in regards to their annual bonus. There are six tactics they can use to ensure they will not miss it again. Tactics like Optimizing Demand Generation Programs, Re-evaluating Pricing & Packaging, Focusing on Repeatable, Scalable Sales Transactions, Introducing Add-on Products, Entering New Geographic Markets, and Competitive Steal-Aways have proven to drive significant revenue growth.