“SaaS Is Dead” Is the Wrong Diagnosis — But Palantir Is Pointing at Something Real

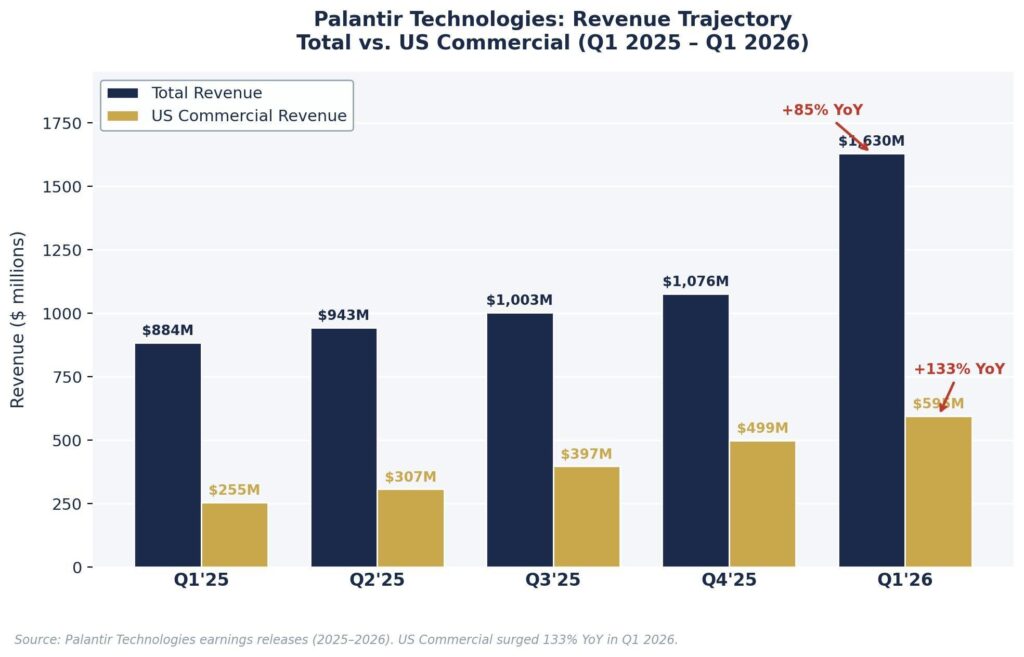

“SaaS is dead.” Those three words, delivered by Danny Lukus, a deployment strategist at Palantir Technologies, sent ripples through enterprise software circles this week. Published on May 16 by Forbes contributor Steve Banker, the claim lands with unusual weight. Palantir is not some analyst firm speculating from the sidelines. The company just reported Q1 2026 revenue of $1.63 billion — up 85% year-over-year — with US commercial revenue surging 133% to $595 million. It now sits among the top 20 most valuable US firms at a $320 billion market cap. When a company performing at that altitude declares a business model dead, the enterprise software industry should pay attention.

But here is the analytical problem: “SaaS is dead” is the wrong diagnosis. It is a provocative marketing thesis dressed up as market analysis. The actual signal in Palantir’s argument is far more actionable — and far more consequential for M&A valuation — than a headline obituary. What Palantir has articulated is not the death of software-as-a-service. It is the emergence of a valuation fault line that will define enterprise software acquisition pricing for the next decade.

What Palantir Actually Said — And What It Didn’t

Lukus’s core argument has two parts worth separating carefully.

First, he argues that standard SaaS forces companies into competitive sameness. When every competitor in an industry buys the same SAP or Blue Yonder supply chain module, no one has an advantage. Worse, when a company asks its software vendor to build a custom feature, that same feature becomes available to every other customer. “You have ceded your strategic differentiation,” Lukus said. Most enterprise deployments still require Excel workarounds — an implicit admission that the standard product does not fit how the business actually runs.

Second, Lukus argues that the economics of custom software development have fundamentally changed. Historically, bespoke enterprise software was prohibitively expensive: months of requirements gathering, high failure rates, enormous total cost of ownership. Today, AI-powered code generation tools — including Anthropic’s Claude and OpenAI’s Codex — can build custom workflows at a fraction of the historical cost. Palantir’s forward-deployed engineers use these tools to rapidly prototype, iterate, and deploy customer-specific solutions. A complex supply chain workflow that would have taken a year to build can now be operationalized in a single quarter.

Notice what Lukus did not say. He did not say that recurring revenue is dead. He did not say that cloud delivery is finished. What he said is that the template model — standardized product, seat-based pricing, shared feature roadmaps — is losing its value proposition against an approach that combines AI-accelerated custom development with enterprise ontology infrastructure.

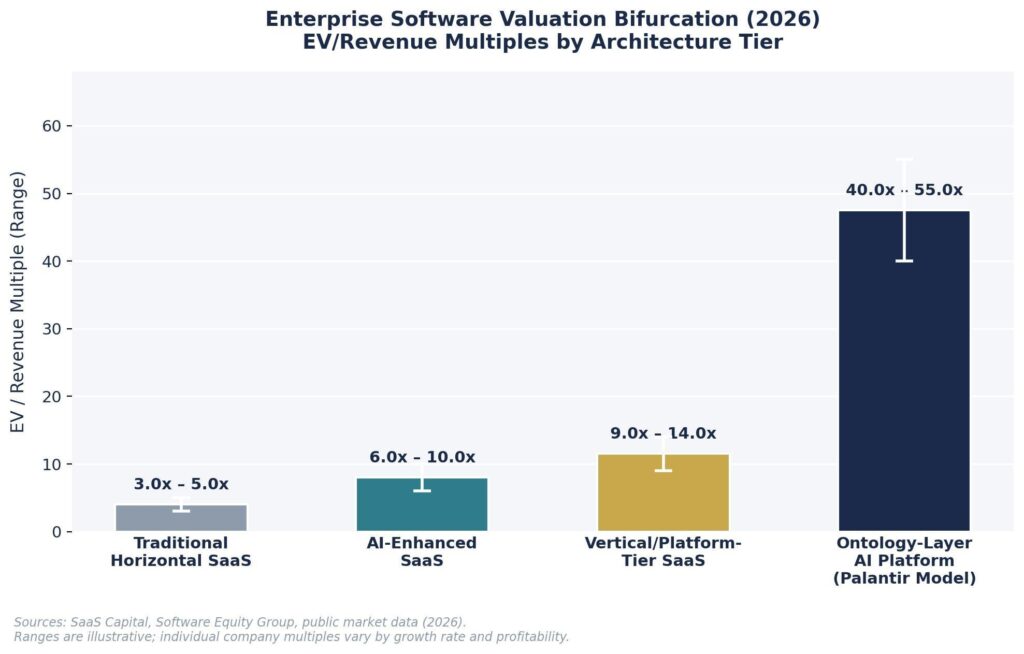

Figure 1: Enterprise Software Valuation Bifurcation (2026) — EV/Revenue multiples by architecture tier. The spread between template SaaS and ontology-layer platforms has widened significantly in the current market.

The Real Thesis: SaaS Bifurcation, Not SaaS Death

The market’s dominant narrative reads the “SaaS is dead” claim as an industry-wide obituary. The data tells a more nuanced story. As we analyzed in The Agentforce Illusion, the enterprise software market is not collapsing — it is bifurcating. The companies facing an existential threat are those that compete solely on template functionality and seat count. The companies commanding premium multiples are those that have become load-bearing infrastructure in their customers’ decision cycles.

This bifurcation is playing out in real M&A valuations. Traditional horizontal SaaS is trading at 3–5x EV/Revenue. AI-enhanced SaaS is landing in the 6–10x range. Vertical, platform-tier solutions command 9–14x. And the Palantir model — ontology-layer, agentic, outcome-based — is valued at market premiums that dwarf the entire category. Palantir itself trades at roughly 49x annualized revenue. That is not a SaaS valuation. That is an infrastructure valuation.

The fault line Palantir is describing is not between “SaaS” and “not SaaS.” It is between software that gives users a place to manage work and software that removes the work entirely. As we documented in our analysis of the AI funding landscape in 2025, investors are already pricing this distinction. The enterprise software companies that command premium capital are those that can demonstrate outcome delivery — not feature access.

| INTELLIGENCE FOR PE/VC INVESTORS |

| The Palantir thesis is a diligence red flag for portfolio companies positioned as standard horizontal SaaS. |

| Key question: Can your holding articulate a differentiation story that survives the “template commoditization” test? |

| Valuation compression risk is highest for: seat-based pricing models, shared roadmap feature development, and standard workflow configurations. |

| Premium multiples (15x+ EV/Revenue) require demonstrable evidence of: customer-specific IP, proprietary data models, or ontology-layer abstraction that locks in workflow logic. |

| Agentforce’s $500M ARR demonstrates platform distribution power — not category-wide agentic adoption. Diligence AI-native targets with this distinction in mind. |

| ACTION: Run a “Palantir test” on your portfolio SaaS assets — if a forward-deployed engineer could replicate the core workflow in a quarter, you have a valuation problem in the next exit cycle. |

Why the Palantir Ontology Layer Is the New Enterprise Moat

The most strategically significant element of Palantir’s architecture is the Ontology — a concept that most M&A analysts have not yet built into their diligence frameworks. The Palantir Ontology functions as an operational abstraction layer that serves as a digital twin of the organization. It integrates physical assets (plants, equipment, products), transactional concepts (orders, financial events), and decisional logic (who can do what, under what conditions) into a single coherent model sitting on top of existing infrastructure.

This is architecturally different from traditional middleware or integration platforms. The Ontology does not just connect systems — it encodes how the business actually works. When Palantir builds a supply chain workflow for a manufacturer, the business logic, decision rules, and data relationships are captured in an organizational model specific to that company. The result is switching costs that are not just technical — they are epistemic. Replacing the Ontology layer means replacing the company’s operational knowledge infrastructure.

From an M&A perspective, this is the new moat. As we noted in our analysis of user research SaaS valuations, the companies commanding the highest acquisition premiums are those embedded in how organizations make strategic decisions. The Palantir Ontology is the supply chain version of that dynamic — and the M&A market is only beginning to price it.

Figure 2: Palantir Technologies Revenue Trajectory (Q1 2025 – Q1 2026). US commercial revenue grew 133% YoY in Q1 2026, driven by manufacturing and supply chain deployments. Source: Palantir earnings releases.

The Skeptic’s Case — And Why It Matters for Diligence

Forbes contributor Steve Banker does not accept the Palantir thesis uncritically, and his skepticism is analytically valuable. Banker explicitly questions whether AI code generation tools can produce production-quality optimization and forecasting algorithms. He notes that supply chain software companies like Manhattan Associates have spent decades developing cutting-edge mathematical algorithms. “Quickly does not mean well,” Banker writes — a distinction that matters enormously in operational contexts where forecast accuracy drives billions in working capital decisions.

Lukus partially concedes the point. He acknowledges that most manufacturing clients initially deploy Palantir for Sales & Operations Execution — sensing exceptions, routing decisions, triggering automatic responses — rather than advanced mathematical optimization. S&OE is fundamentally about workflow automation and exception handling, not algorithmic sophistication. That is a significantly narrower claim than “SaaS is dead” implies.

The diligence implication is critical. The Palantir thesis is most credible in workflow-intensive, exception-heavy operational domains (supply chain execution, procurement, field operations). It is far less credible as a replacement for mathematically sophisticated planning systems in demand forecasting, network optimization, or financial modeling. Acquirers evaluating enterprise software assets should map their target’s core value against this distinction before extrapolating the Palantir narrative to their category.

| INTELLIGENCE FOR SAAS FOUNDERS PREPARING FOR EXIT |

| The Palantir argument is not symmetrical — it hurts some SaaS companies and rewards others. |

| If your product is a horizontal workflow tool replicable by a forward-deployed engineer in a quarter, you have a positioning problem that will show up in your exit multiple. |

| If your product encodes customer-specific business logic, proprietary data models, or deep integration with operational decision cycles, you may be sitting on undervalued infrastructure. |

| The “template commoditization” argument lands hardest on: shared feature roadmaps, seat-based pricing without outcome metrics, and tools that sit alongside Excel rather than replacing it. |

| The most durable exit story in the current market: “We are the system of record for a workflow that matters, and switching means dismantling operational knowledge — not just migrating data.” |

| See our analysis of the SaaS Exit Crisis and AI funding dynamics for tactical frameworks on repositioning before an exit process. |

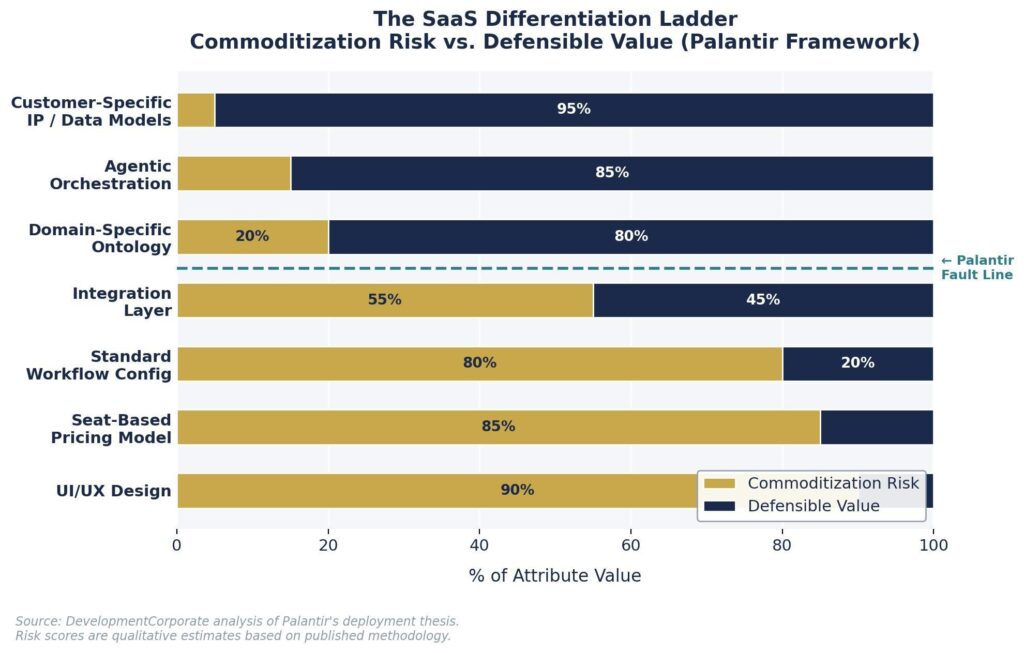

Figure 3: The SaaS Differentiation Ladder — Commoditization Risk vs. Defensible Value under the Palantir Framework. Attributes below the fault line command premium M&A valuations; those above face continued multiple compression.

A Due Diligence Framework: Where Does Your Target Sit?

The Palantir thesis creates a practical diligence framework. The central question is not “does this company use AI?” It is “where does this company sit on the differentiation ladder?”

High-Risk Attributes (Commoditization Zone)

- Seat-based pricing with no outcome metrics

- Feature roadmap driven by majority-customer consensus (benefits all competitors equally)

- Standard workflow configuration that mirrors industry templates

- Core value proposition replicable through AI-assisted custom development

- Primary integration through spreadsheet export/import — the “Excel workaround” signal

Defensible Attributes (Premium Valuation Zone)

- Customer-specific IP embedded in data models or decision logic

- Ontology-layer abstraction that serves as an organizational digital twin

- Agentic orchestration across multi-step operational workflows

- Outcome-based pricing tied to measurable operational results

- Switching costs that are epistemic (knowledge capture) rather than merely technical

Our EV/Revenue multiple analysis shows that the spread between commodity SaaS (3–5x) and platform-tier software (15x+) has widened in every quarter since 2023. The Palantir thesis is not creating this bifurcation — it is articulating a fault line that the data already reflects. Acquirers who have not built this distinction into their valuation models are systematically mispricing both risk and opportunity.

The Advance Auto Parts Signal: Reading Palantir’s Commercial Playbook

The disclosure that Advance Auto Parts is working with Palantir on inventory replenishment and pricing is more significant than it appears. Auto parts distribution is operationally dense, margin-sensitive, and dependent on millions of SKU-level decisions made daily across thousands of locations. It is exactly the kind of domain where workflow-intensive S&OE value is highest and where standard ERP configurations leave the most Excel-shaped gaps.

The pattern is consistent across Palantir’s commercial customer base: Wendy’s, Tyson Foods, General Mills. These are not technology companies experimenting with AI. They are operationally complex enterprises where supply chain execution directly drives margin. Palantir’s penetration into this segment — now representing 46% of revenue with manufacturing as the largest vertical — is evidence that the ontology-layer model works in production for the buyers who matter most to enterprise software M&A.

This is the most important counterpoint to the “SaaS is dead” framing. Palantir is not competing with most SaaS companies. It is competing with the systems-integrator layer — the expensive, slow, failure-prone custom development market that SaaS was originally supposed to replace. The customers choosing Palantir are not canceling Salesforce subscriptions. They are canceling Accenture statements of work.

| INTELLIGENCE FOR ENTERPRISE CTOs & CPOs |

| The Palantir thesis forces a question standard procurement rarely asks: what is the strategic cost of template standardization? |

| If your business model depends on operational differentiation — service levels, inventory positioning, pricing agility — running the same platform as your competitors has a real strategic cost. |

| Apply the Excel Workaround Test: count the manual data exports, offline calculations, and spreadsheet bridges in your current software stack. Each one is evidence the template does not fit. |

| AI agents in supply chain are most credible for: exception handling, PO parsing, stock-check orchestration, S&OE workflows. They are far less credible for advanced demand planning, network optimization, or constraint-based scheduling. |

| GEO visibility is now a software selection variable: vendors with strong LLM citation footprints appear on AI-generated shortlists that others miss entirely — factor this into your vendor evaluation methodology. |

| ACTION: Before your next ERP or SCM renewal, run a differentiation audit — document which capabilities give your supply chain a competitive advantage that your current platform cannot encode. |

The Bottom Line: A Bifurcation Signal, Not an Obituary

“SaaS is dead” will generate clicks and conference debate. The more useful framing is: standard template SaaS is losing its valuation premium to software that captures and operationalizes customer-specific business logic. That is a market force, not a marketing line.

Palantir’s Q1 2026 performance — 85% revenue growth, 133% US commercial growth, $320 billion market capitalization — is not the profile of a company predicting its own industry’s death. It is the performance profile of a company that has found a new stratum in the enterprise software value chain: above the template SaaS layer, below the custom enterprise development layer, and increasingly inseparable from the operational knowledge of its largest customers.

For M&A practitioners, the actionable insight is straightforward. The valuation compression affecting traditional SaaS assets is structural — and the Palantir thesis explains the mechanism. Companies that encode customer-specific operational intelligence into their product will command infrastructure-tier multiples. Companies that sell access to standardized functionality at per-seat prices will face continued multiple compression regardless of how many AI features they add to their marketing decks.

The question every enterprise software company — and every investor in one — needs to answer is not “is SaaS dead?” It is: “where does our product sit on the differentiation ladder, and what is that position worth in the next deal?”

─────────────────────────────────────────────────────────────────────

DevelopmentCorporate LLC provides M&A advisory and strategic consulting for enterprise SaaS companies. With 30+ years of enterprise software experience and $175M+ in completed acquisitions, we help founders, PE sponsors, and enterprise buyers navigate valuation strategy, competitive positioning, and exit planning. Schedule a confidential conversation →