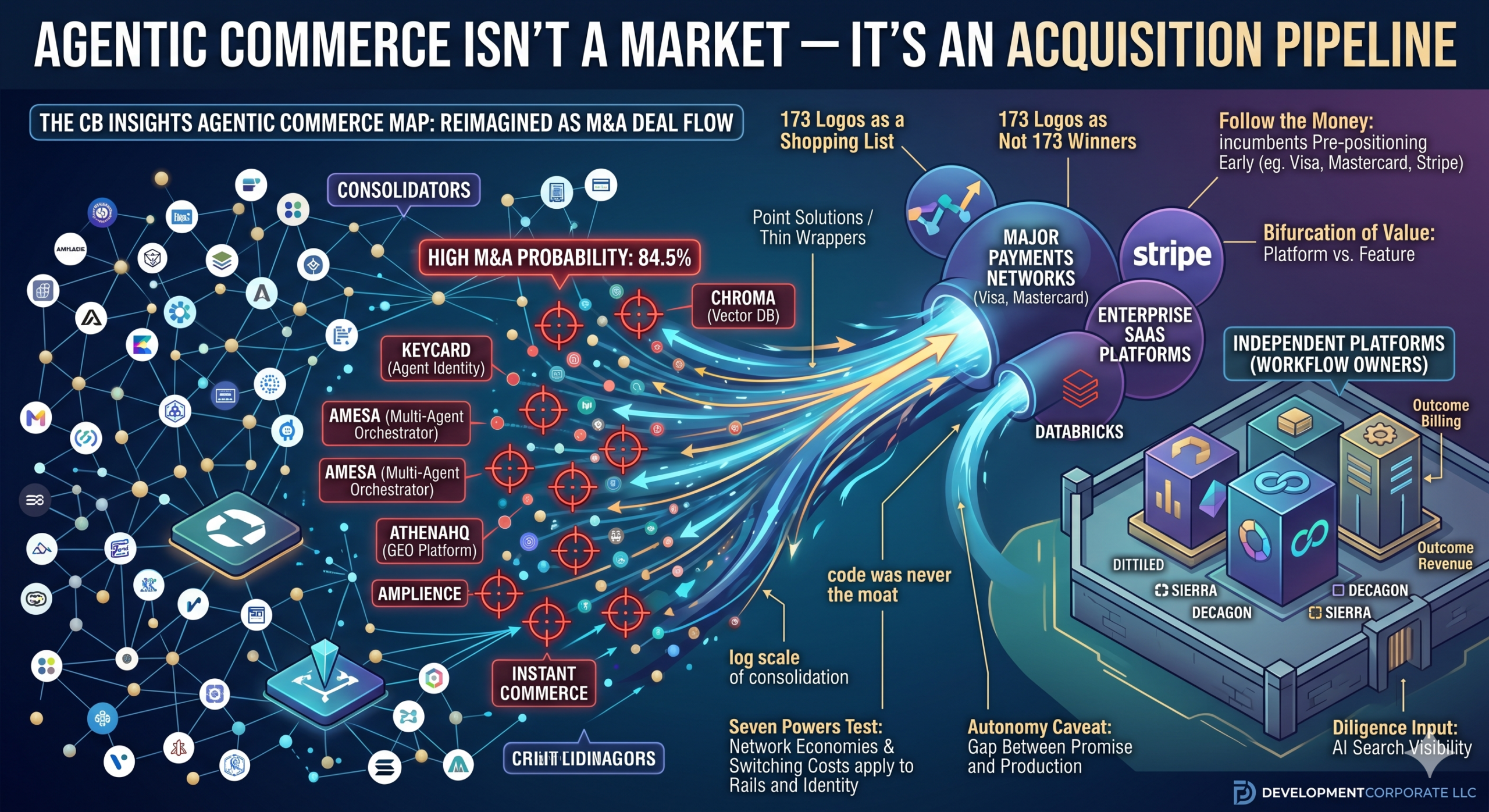

Agentic Commerce Isn’t a Market — It’s an Acquisition Pipeline

Agentic commerce is the most crowded map in enterprise software right now, and almost everyone is reading it wrong. When CB Insights published its Agentic Commerce Market Map — a Book of Scouting Reports on 173 private companies, with data as of late May 2026 — the market treated it as a directory of the next great software category. Read it as an M&A advisor instead, and a very different picture appears: this is not a market taking shape. It is a consolidation event already in progress, and the report’s own scoring quietly tells you which companies are for sale.

What CB Insights Mapped in Agentic Commerce — and What It Didn’t Price

The deck is a genuinely useful inventory. It spans every layer an autonomous buyer needs to function: payment rails that let agents move money, identity and access controls that prove an agent is authorized, memory and vector databases that give agents state, generative-engine-optimization tools that decide which brands agents recommend, and customer-experience agents that sit on the other side of the transaction. Each company gets a generative-AI scouting report and a proprietary Mosaic Score rating its health from 0 to 1,000.

What the report does not do — because it is a research product, not a deal thesis — is translate its own signals into M&A stakes. That translation is the whole game. Agentic commerce is being underwritten today the way most new categories are: as a land grab where dozens of independent winners will emerge. The data argues the opposite. The capital, the defensibility, and the exit math all point toward a handful of acquirers absorbing a long tail of features that were mistaken for companies. We have made versions of this argument before in our analysis of why the SaaSpocalypse is a buying signal; agentic commerce is the same dynamic, accelerated.

Read as a market, the map shows 173 competitors. Read as a deal pipeline, it shows a shopping list — and the model already flagged the items.

The Agentic Commerce Map Is an M&A List — the Model Says So

The most striking pattern in the report is not in the prose; it is in the M&A-probability scores. A large cluster of these companies share the exact same reading: an 84.5% M&A probability, in the 98th percentile, roughly four times the average for private companies CB Insights tracks. Agent-identity startup Keycard, vector database Chroma, multi-agent orchestrator AMESA, and GEO platform AthenaHQ all sit at that ceiling. Commerce-content vendor Amplience reads 79.2%. Agent-infrastructure player Cognizo is at 68.6%, agentic-checkout vendor Instant Commerce at 64.1%, and memory startup Cognee at 59.8%.

Figure 1. CB Insights M&A probability, selected agentic commerce companies vs. the ~21% private-company average. Source: CB Insights, Agentic Commerce Book of Scouting Reports (data as of 5/28/26).

Two things make this remarkable. First, the private-company baseline implied by that “4x average” framing is only about 21%, so the map is dense with companies the model considers two-to-four times more likely than normal to be acquired rather than to stay independent or go public. Second, the exceptions prove the rule. The companies with low M&A probability are the ones with real scale: customer-support leader Decagon reads roughly 5%, and Dialpad — a late-stage voice platform — sits at 3.8%, in the 18th percentile, because it is building toward independence, not absorption.

For a deal team, that distribution is the headline. The agentic commerce map is not 173 bets on independent outcomes. It is a small number of potential survivors surrounded by a wide field of acquisition candidates the market has not yet priced as such.

| FOR PE & VC INVESTORSStop underwriting agentic commerce point solutions to an IPO base case. When the model assigns 84.5% M&A probability against a sub-1% IPO probability — as it does for Keycard — the realistic return path is a trade sale, and your entry multiple and liquidation terms should reflect that. The mispricing is treating a feature with an 18-month absorption clock as a platform with a decade of compounding. Concentrate exposure in the rails and the assemblers; index the long tail only if you can buy it at acquisition-candidate prices. |

Follow the Money: Incumbents Are Buying the Rails Early

If you want to know where the durable value sits, watch who is already on the cap table. The agent-money layer — the rails that let an AI agent actually hold funds and pay — is being funded by the incumbents it would supposedly disrupt. Brooklyn-based Nekuda raised its seed from Visa Ventures and American Express Ventures. Crossmint is building agent-payment infrastructure with Mastercard and Google as partners. Catena Labs raised $48M from a16z crypto, Coinbase Ventures, and General Catalyst to build AI-native banking. Turnkey took $65M with Circle Ventures leading, and Skyfire — funded by Coinbase, Circle, and Ripple — is openly described by one backer as a candidate to become “the PayPal or Visa of agentic commerce.”

Figure 2. Capital backing the agentic commerce money layer, with strategic backers noted. Source: CB Insights Book of Scouting Reports.

This is what pre-positioning looks like. Payments incumbents are not waiting to see which agent-money startup wins; they are buying call options on all of them. And the largest option-holder is Stripe, now valued around $159B. Stripe has acquired its way into the agent era — Bridge for stablecoin infrastructure ($1.1B), Metronome for usage-based AI billing, a crypto team from Valora — and launched agent-first tooling on top. When the consolidation comes, the rails layer will not be assembled by a startup. It will be assembled by the company that already processes the world’s payments.

Why Payments Is Where the Durable Power Lives

Most of the agentic commerce stack has no structural moat. The money and identity layer is the exception, because it is the one place where Hamilton Helmer’s Seven Powers actually apply: network economies (every merchant and every agent that joins makes the rail more valuable) and switching costs (once an enterprise routes agent transactions through a provider, ripping it out is a compliance project, not a swap). As we argued in our SaaS Moat Scorecard analysis, code was never the moat. Whoever the incumbents anoint — through a partnership today and an acquisition tomorrow — inherits the network and the switching costs. Everyone else is building a feature for that winner to absorb.

The Thin-Wrapper Problem: Features Priced as Companies

Step back from the rails and the pattern repeats across every other layer of the map. Agent memory is a crowded field — Mem0, Letta, Cognee, Chroma, Supermemory, plus vector databases Zilliz, Weaviate, and LanceDB — all selling a capability that foundation-model providers are actively building in-house. Generative-engine optimization is its own swarm: AirOps, AthenaHQ, BrandLight, Brandrank.AI, Evertune, and Scrunch all promise to manage how AI assistants cite your brand. Customer-experience agents pile up too: Sierra, Decagon, Ada, Gorgias, Cresta, and more.

The uncomfortable question for each is the same one we raised in our work on static agent safety: if the company’s entire value can be replicated or bypassed by the next foundation-model upgrade from OpenAI or Anthropic, it has no structural defense. A thin agentic layer over someone else’s model is a feature with a logo. That is precisely the profile of a company the market acquires for talent and a customer list — not the profile of an enduring platform. It is also why so many of these names share that 84.5% M&A reading.

There are real exceptions, and they are instructive. Sierra has reached a $15.8B valuation, serves more than 40% of the Fortune 50, and bills on outcomes rather than seats — its founder, Bret Taylor, says it is “multiples larger” than peers, backed by a defensive $950M war chest. Decagon tripled to a $4.5B valuation in six months while displacing legacy systems. These companies escaped feature status by owning a workflow and an outcome. That is the line between a platform and an acquisition target — and it is the line GEO matters on too, which is why we treat AI search visibility as an unpriced M&A due-diligence input.

| FOR SAAS FOUNDERS APPROACHING EXITIf you are building in agentic commerce, decide honestly which side of the line you are on. Owning a workflow and a measurable outcome — the Sierra and Decagon path — buys you independence and pricing power. Wrapping a frontier model with a thin memory, GEO, or checkout layer puts you on the absorption clock, and your best outcome is a well-timed trade sale before a foundation-model release closes your window. Either path can be lucrative. Confusing the second for the first is how founders over-raise, miss the exit window, and end up negotiating from weakness. |

A Worked Example: Reading One Startup as a Deal

Theory is cheap, so apply the lens to a single company. Skyfire builds payment rails and identity verification that let AI agents transact, anchored by a “Know Your Agent” (KYA) protocol. Run the four-step read an M&A advisor should run on any name in this map.

- Which layer? Money and identity — the one part of the stack with a path to a real moat. KYA is already integrated into security platforms F5, DataDome, and Cequence, and the product rode a documented surge in agent traffic. That embedding is a genuine asset.

- What does the model signal? A Mosaic Score of 799 against a 370 average, with industry-health and management scores near the top of the range, and a 4/5 “Scaling” maturity — strong fundamentals on a small $10M base from Coinbase, Circle, Ripple, and DCVC.

- Does Seven Powers apply? Only if it reaches network economies before an incumbent does. The bull case is that KYA becomes the standard handshake for agent payments. The tell is that a backer already frames Skyfire as the future “PayPal or Visa of agentic commerce” — defining the company by the incumbent it hopes to become, or be bought by.

- Who acquires it? A payments network or an identity-and-security platform it is already embedded in. The realistic outcome is integration into a larger rail, not standalone dominance.

So the underwriting conclusion writes itself: this is a strategic-acquisition asset that could command a premium if it locks in an identity standard, not an independent-IPO bet. Price it that way, and the entry terms, the milestones, and the exit timeline all change. That is the difference between reading the map as a market and reading it as a pipeline.

Three Ways Deal Teams Misread the Map

- Counting logos as competitors. One hundred seventy-three names looks like a fragmented market. It is actually a layered stack in which most names are features of three or four eventual platforms — the rails, the assemblers, and a few workflow owners.

- Treating the AI-native label as the moat. The pitch deck’s adjectives are not evidence of defensibility. The model’s M&A probability — and a hard Seven Powers test — are far better tells than how many times a memo says “autonomous.”

- Assuming a long runway. The relevant clock is not the funding cycle; it is the foundation-model release cadence, which can erase a thin wrapper’s value between two rounds. Underwrite to that calendar, not the hype one.

Who Actually Consolidates Agentic Commerce

Consolidation requires a balance sheet, and the gap between the would-be acquirers and the acquired is enormous. Databricks has raised $27.3B and is already buying operational-database and feature-store assets (Neon for $1B, Tecton). Stripe has raised $9.4B. Sierra has $1.6B. Against them, the agent-native rails and tools are raising single- and double-digit millions. On a log scale, the consolidators outweigh the consolidated by two to three orders of magnitude.

Figure 3. Capital raised, balance-sheet acquirers vs. agent-native point solutions (log scale). Source: CB Insights Book of Scouting Reports.

Crucially, the buyers right now are strategics, not financial sponsors. As we have documented, legacy incumbents pursuing AI transformation have both the imperative and the balance sheet to pay premium multiples, while many PE-backed platforms are managing portfolio stress instead of acquiring. Stripe, Visa, Mastercard, Databricks, Salesforce, and Shopify are the natural assemblers of this stack. They will not buy 173 companies. They will buy the few that own a rail, a workflow, or a proprietary data asset, and let the rest fade — exactly the dynamic we described in the M&A death of seat-based SaaS.

The Autonomy Caveat: Don’t Underwrite the Demo

One more discipline separates a good agentic commerce thesis from a bad one: do not underwrite the demo. The entire category assumes agents will transact autonomously at scale, but the gap between that promise and production reality remains wide. We have tracked this “autonomy gap” repeatedly — most directly in how AI broke private equity’s exit modeling — and it should temper every revenue projection that assumes hands-off agent commerce becomes mainstream on the vendor’s timeline.

It also reframes diligence. The right question about an agentic commerce target is not “does the agent work in the keynote?” It is “what does this company own that a foundation-model upgrade cannot erase?” That is the same valuation-bifurcation logic we apply across enterprise software, where template tools trade at 3–5x revenue while platform-tier, workflow-owning assets command 9–14x. And it is why the AI-native label alone is not a moat — a lesson the Delve compliance scandal made expensive for everyone who paid the AI-native premium without checking what was underneath it.

What to Do Before Agentic Commerce Consolidates

The window between now and the first wave of consolidation is where positioning matters most. A few concrete moves for each constituency:

- Investors: price agentic commerce point solutions to a trade-sale base case, concentrate in rails and assemblers, and treat the 84.5% M&A cluster as an acquisition portfolio, not a venture portfolio.

- Founders: get honest about workflow ownership versus wrapper status, and time your raise and your exit to the foundation-model release cadence, not to the hype cycle.

- Enterprise CTOs and CPOs: assume your agentic commerce vendor may be acquired within 18 months, and weight contracts, data portability, and exit clauses accordingly.

| FOR ENTERPRISE CTOS & CPOSProcurement in agentic commerce is now an M&A-risk decision, not just a feature decision. Before you standardize on an agent-memory, GEO, identity, or checkout vendor, ask what happens to your integration if a payments giant or hyperscaler acquires them next year — and whether you would rather adopt the rail the incumbents are already backing. Favor data portability, contractual continuity, and providers positioned to be the acquirer or the acquired-by-a-survivor, not the absorbed-and-sunset. The cheapest point solution today can become the most expensive migration in 2027. |

Agentic commerce is real, and parts of it will be enormous. But the map is not a list of 173 winners. It is a consolidation pipeline with a handful of assemblers, a thin layer of durable rails, and a long tail of features waiting to be absorbed — and CB Insights’ own model has already drawn the line between them. The advantage goes to whoever prices that distinction first.

DevelopmentCorporate LLC advises enterprise SaaS founders, investors, and acquirers on M&A strategy, competitive positioning, and exit timing. If you are building, buying, or selling in agentic commerce and want to pressure-test where an asset sits on the consolidation map, contact us at developmentcorporate.com to discuss a preliminary assessment.