Operational Alpha Is a Warning Label for SaaS Sellers

Private equity says it has matured. Read through an M&A valuation lens, its new playbook is a signal that the easy SaaS exit is gone.

Operational alpha is the phrase private equity now uses for its newest source of returns: value built by genuinely improving how a company runs, instead of by cheap debt and rising multiples. Alvarez & Marsal’s May 2026 survey of 200 European PE professionals and portfolio-company executives argues that the industry has matured into this discipline. It is a confident, carefully built report. It is also — read through an M&A valuation lens — one of the more consequential warning labels a SaaS founder will see this year.

The reason is simple. The same report that celebrates operational alpha also documents a buyer universe that is shrinking for software, holding existing assets longer, and missing its own value-creation targets roughly two times out of three. The surface story is maturity. The sell-side story is a contracting set of exit routes and a higher execution bar on every deal you bring to market.

What “Operational Alpha” Actually Means

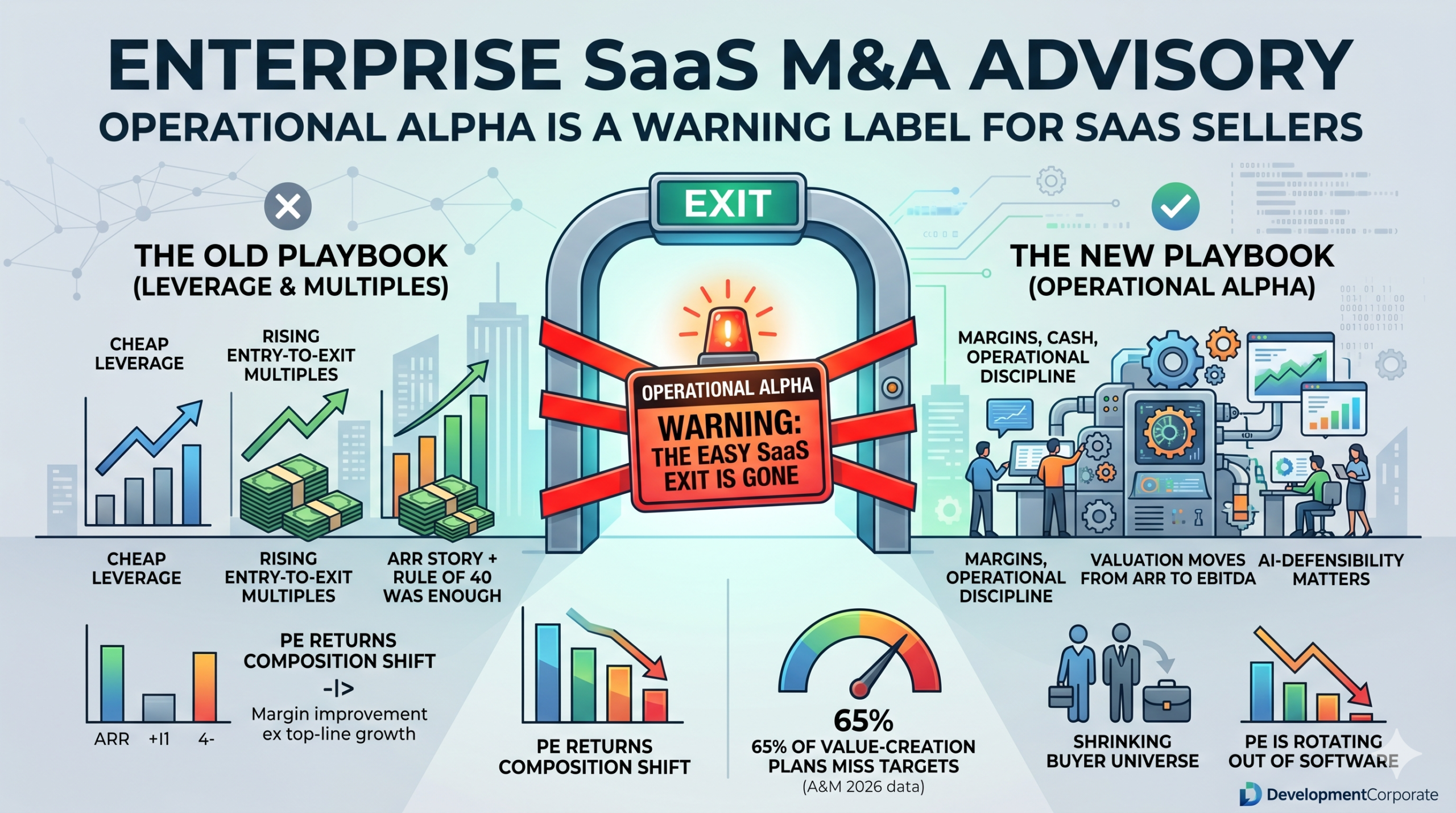

For most of the 2010s, private equity returns leaned on three forces: cheap leverage, steadily rising entry-to-exit multiples, and buy-and-build roll-ups financed by that cheap debt. A sponsor could buy a company, add a few acquisitions, refinance, and sell into a higher-multiple market a few years later. The operating business barely had to change.

That era is over. Higher rates, entry multiples still sitting near record highs, and a selective exit market have removed the financial tailwinds. A&M’s data shows the consequence directly. Among European deals the firm analyzed, EBITDA margin improvement accounted for 51% of EBITDA growth on assets exited in 2025 — more than double the share seen before 2023. The contribution of top-line expansion fell from 78.5% to 49% over the same window. In plain terms, the returns are now being manufactured inside the business, through pricing, cost, cash and operational discipline, rather than handed to sponsors by the market.

That is operational alpha: measurable, durable improvement that is less dependent on market conditions. A&M frames it as the industry growing up. For a consulting firm whose business is operational improvement, that framing is unsurprising — and largely correct on its own terms. The question is what it signals to everyone standing on the other side of the deal table.

The Confession Hidden Inside the Operational Alpha Story

Strip away the optimistic packaging and the numbers describe a market under real stress. European PE funds are sitting on an inventory of more than 14,000 companies, nearly 4,000 of which have been held for six years or more. Median hold times for sold assets touched a record 6.6 years in 2024 before easing to 5.8 in 2025 — still near historic highs. Fundraising for buyout funds fell again, and established managers captured 85.6% of the capital that was raised, squeezing everyone else.

Here is the detail that should stop any seller cold. Sponsors have professionalized exactly as the maturity narrative claims: 58% now deploy value-creation resources in the first 100 days, up from 29% a year earlier; AI use in value creation jumped from 41% to 63%; and 97% now say ESG credentials help portfolio performance, up from 68%. The operational machine is unmistakably faster and more sophisticated.

And yet 65% of respondents say less than half of the value-creation plans they built over the past two years have actually been realized — essentially flat versus the prior year. More effort, more tooling, more early engagement, and the same shortfall. A&M attributes this to capacity gaps (cited by 41%) and specialist-expertise gaps (37%). Whatever the cause, the operational alpha that underwrites today’s stretched entry valuations is, by the industry’s own admission, mostly not landing.

Figure 1. The operational machine has accelerated, but the share of value-creation plans that miss their targets has not moved. Source: Alvarez & Marsal, Operational Alpha (2026); DevelopmentCorporate analysis.

| FOR PE / VC INVESTORSIf two-thirds of value-creation plans are still under-realized despite earlier, AI-enabled execution, the bottleneck is not effort — it is underwriting. When entry valuations are justified by operational improvements that miss ~65% of the time, the return model carries a structural execution discount that most committee memos do not price. We unpack the related modeling problem in When AI Broke Private Equity’s Crystal Ball. |

Operational Alpha Raises the Bar on Every SaaS Exit

For a SaaS founder, the operational-alpha shift changes the exit math in a specific, uncomfortable way. Private equity has been the most reliable institutional buyer of mid-market software for a decade. In the old model, a clean ARR story plus Rule of 40 was often enough; the sponsor would supply the financial engineering. In the operational-alpha model, the sponsor is buying a transformation thesis — and pricing your company on whether that thesis can be executed.

That has two effects on your valuation. First, the buyer’s confidence in its own operating plan now sits inside the multiple it will offer. A sponsor that has watched 65% of its plans under-deliver will haircut ambitious synergy and margin assumptions accordingly. Second, the basis of valuation is moving from revenue to earnings. We have documented how SaaS private credit lenders have

abandoned ARR-based underwriting in favor of EBITDA floors — a shift that historically precedes the equity market by 6 to 18 months. A&M’s data is that equity shift arriving: the value PE now manufactures is overwhelmingly margin, cost and cash, not the top-line growth story SaaS decks are built to sell. See SaaS Private Credit Lenders Are Done With ARR and the 2026 benchmarks that reveal a valuation trap, not a recovery.

Figure 2. The composition of PE returns has inverted: operational excellence now contributes more EBITDA growth than top-line expansion. Source: A&M analysis of 239 Western European PE exits, 2013–2025.

There is a buyer-side trap inside this shift that cuts the other way, and sellers should understand it because it will shape diligence. When margin expansion comes from cutting sales, marketing and back-office spend rather than from operating leverage, a disciplined acquirer will normalize that EBITDA back down before applying a multiple. A headline margin built on under-investment can swing enterprise value by 25–30% once a buyer restores the capacity needed to sustain growth. If your margin story is composition-light, expect it to be re-priced in the data room.

| FOR SAAS FOUNDERS APPROACHING EXITAudit your EBITDA the way a sponsor’s operating partner will. Separate margin earned through genuine operating leverage from margin earned by starving growth, and be ready to defend pipeline coverage and new-logo bookings through the cut. The margin story buyers are misreading is exactly the line item that determines whether your number survives diligence intact. |

The Signal Founders Cannot Ignore: PE Is Rotating Out of Software

The single most important sentence in the A&M report, for a software seller, is not about operational alpha at all. It is the observation that the AI disruption that triggered “a material reset in public software valuations in early 2026” is pushing leading sponsors to reorient their underwriting away from capital-light businesses and into so-called “heavy assets” — manufacturers, industrial suppliers and tangible-goods companies seen as less exposed to technological obsolescence.

Read that as a demand-side shock to SaaS exit multiples. Your most active institutional buyer is, at the margin, deciding that software’s defining advantage — its capital efficiency — is now a liability, because the same lightness that made it scalable makes it replicable by an AI-native competitor in twelve to eighteen months. This is not a hypothetical. Public SaaS multiples that briefly touched 15x revenue in 2021 compressed below 5x by early 2026, and private valuations sit below that still.

The defensible-versus-exposed split now governs which software assets sponsors will still chase. AI-defensible software — proprietary data, embedded workflows, strong gross retention, a credible automation roadmap, what Hamilton Helmer would call a durable Power — still commands premiums. AI-exposed, single-function software faces compressing multiples and a thinning buyer list. We trace this bifurcation in The AI Valuation Gap and in why the SaaS-pocalypse is also a buying signal for the right assets.

The financing plumbing reinforces it. As we detailed when JPMorgan marked down its software loans, less available back-leverage means lower prices a PE buyer can justify paying. A sponsor that is both wary of software’s AI exposure and constrained on leverage is a structurally weaker bidder for your company than the same sponsor was in 2021.

The Exit Logjam Behind the Rebrand

If sponsors are buying less software and holding everything longer, where does the liquidity come from? Increasingly, from not selling at all. A&M’s data on how funds handle aging assets is the clearest tell that operational alpha is partly a coping mechanism for a jammed exit market.

Half of sponsors are now choosing to refinance and extend the value-creation runway while they wait for better conditions, up from 47%. The share turning to the secondary market or continuation funds nearly doubled to 43%, from 24% a year earlier. And forced sales at lower valuations collapsed to 7%, from 29% — not because the assets are suddenly worth more, but because sponsors have found ways to avoid crystallizing the price the market would actually pay today.

Figure 3. Faced with aging assets, sponsors are extending and refinancing rather than selling. Source: Alvarez & Marsal, Operational Alpha (2026).

Continuation vehicles have moved from niche to mainstream. According to Schroders Capital, continuation investment volumes have grown at a 27% CAGR since 2012, reached roughly $70 billion in 2024, and are projected to exceed $300 billion by 2034. Jefferies puts total secondary volume at a record $240 billion globally in 2025, up 48% year over year, with about a fifth of all PE exits now flowing through continuation structures.

For a founder, the continuation-fund boom is double-edged. It keeps capital recycling through the system, which is good for overall deal activity. But it also means a meaningful share of “exits” are sponsors selling assets to themselves — liquidity events that do not require a fresh, arm’s-length buyer to validate a price. That is not the competitive, multiple-setting auction a seller wants to walk into. And A&M notes the catch for the companies inside these vehicles: when an asset is granted “more time,” the bar on operational delivery rises, not falls.

| FOR ENTERPRISE CTOS / CPOSWhen a strategic vendor sits in a PE portfolio that is refinancing and extending rather than exiting, expect intensified monetization pressure: dynamic pricing, packaging changes, and aggressive cross-sell aimed at the margin and cash targets the sponsor now lives by. Build pricing-protection and continuity terms into renewals, and treat a vendor’s ownership status and hold age as first-class procurement and concentration-risk inputs. |

What Operational Alpha Means for Your 2026 Exit Plan

The takeaway is not that SaaS exits have disappeared. It is that the operational-alpha era rewards a specific kind of seller and punishes the rest. The founders who clear the bar will be those who arrive with the proof a sponsor can no longer generate cheaply on its own. Concretely:

- Lead with earnings quality, not ARR. Present clean, accrual-based, normalized EBITDA and be able to show that margin came from operating leverage, not from cutting the muscle a buyer will have to rebuild.

- Pre-build the value-creation plan the sponsor would otherwise underwrite. Pricing, working-capital and procurement initiatives that you can evidence as already in motion de-risk the buyer’s thesis — the very thesis that misses 65% of the time when they run it themselves.

- Document AI-defensibility explicitly. Proprietary data, switching costs, retention durability and a credible roadmap against AI-native entrants now sit directly in the buyer’s terminal-value model. Silence on AI exposure reads as risk.

- Treat exit timing as a window, not a floor. With sponsors rotating toward heavy assets and leaning on continuation vehicles, the pool of motivated software bidders is thinner and more selective than headline deal counts suggest.

Founders who want the full survival framework should read The SaaS Exit Crisis: A Survival Guide for CEOs Navigating the AI Era, which maps these dynamics into a concrete exit-planning sequence.

The Bottom Line for SaaS Sellers

A&M is right that private equity has changed in a durable way. Financial engineering is no longer enough, and operational alpha — real, measurable operating improvement — is now the main engine of returns. The report makes that case well, and PE-backed businesses are demonstrably outgrowing public peers as a result.

But maturity for the buyer is not the same as opportunity for the seller. The operational-alpha era arrives bundled with a wary attitude toward software, a financing environment that caps what sponsors can pay, an exit market so jammed that “don’t sell” has become the default strategy, and an honest admission that the operational improvements underwriting today’s prices mostly fail to fully materialize. For a SaaS founder reading the same report, the right response is not optimism about a maturing industry. It is preparation for a buyer who is more selective, more earnings-focused, and harder to impress than at any point in the last decade.

Operational alpha is a genuine discipline. It is also a warning label. The founders who read it as one — and rebuild their exit narrative around earnings quality and AI-defensibility before they enter a process — will be the ones who still command a premium when the buyer universe has quietly contracted around them.

Planning a SaaS exit in the operational-alpha era?

DevelopmentCorporate provides M&A advisory and exit strategy for enterprise SaaS companies — from earnings-quality positioning and AI-defensibility narratives to buyer mapping and diligence preparation. Start the conversation about how the shift to operational value creation should shape your timing and your terms.