Is Palantir Still an Existential Threat to the SaaS Industry?

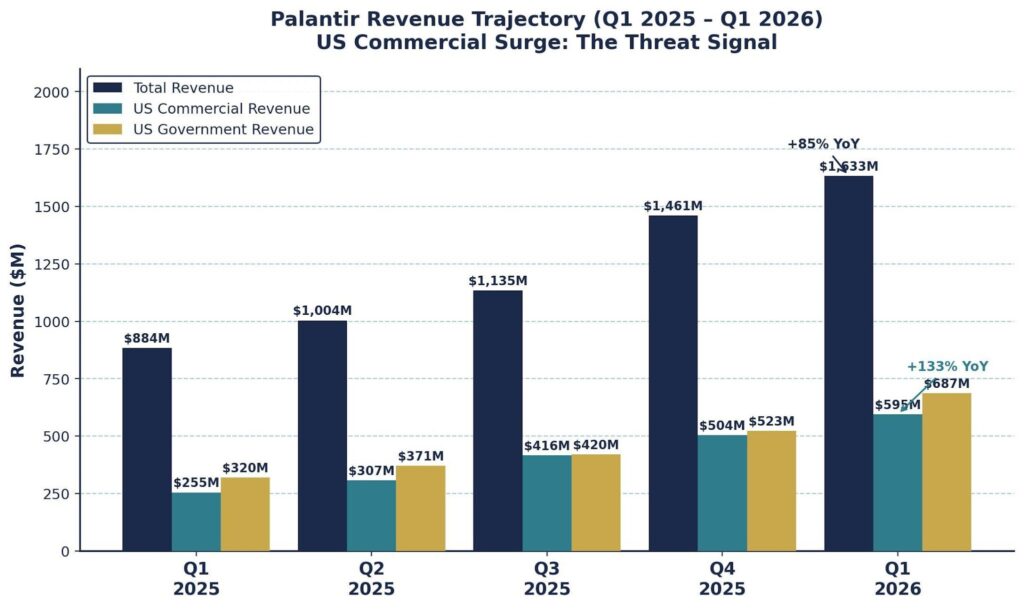

The Palantir existential threat to SaaS narrative refuses to die — and the data suggests it shouldn’t. After a sharp software sector selloff in early 2026 sent Palantir’s stock down 18% from its peak, a wave of analysts declared the company overvalued and the SaaS disruption story overblown. Then Q1 2026 earnings landed. Revenue of $1.63 billion. Growth of 85% year-over-year. US commercial revenue up 133%. A Rule of 40 score of 145% — matched only by NVIDIA, Micron, and SK hynix among the world’s 100 largest public companies.

This is not the profile of a company whose threat has faded. This is the profile of a company that used the selloff to accelerate. The question for enterprise software executives, M&A practitioners, and SaaS investors is not whether the threat is real. The question is: which SaaS companies are genuinely at risk — and which are not?

The Selloff That Changed Nothing Fundamental

Palantir stock dropped roughly 18% in the first quarter of 2026, caught in a broad software sector rotation driven by fears that AI agents would displace per-seat SaaS licensing. The bears had a coherent argument: if an AI agent can do the work of five employees, companies will stop paying for five software seats. Per-seat revenue collapses. The SaaSpocalypse narrative wiped more than $1 trillion in market cap from the software sector in less than 90 days.

The irony is that the selloff applied to Palantir the same logic that Palantir itself had been using against traditional SaaS vendors. Markets feared Palantir was just another software company vulnerable to AI commoditization. Q1 earnings demolished that thesis. As CNBC reported, Q1 marked Palantir’s fastest revenue growth rate since its 2020 direct listing. CEO Alex Karp drew a sharp distinction on the earnings call between Palantir and the AI model developers locked in a race to the bottom on token costs: “There seems to be a rotation amongst AI model companies who engage in an intensely competitive race in which we have seen token costs suffer a thousandfold decline.” Palantir is not in that race. It runs the layer above it.

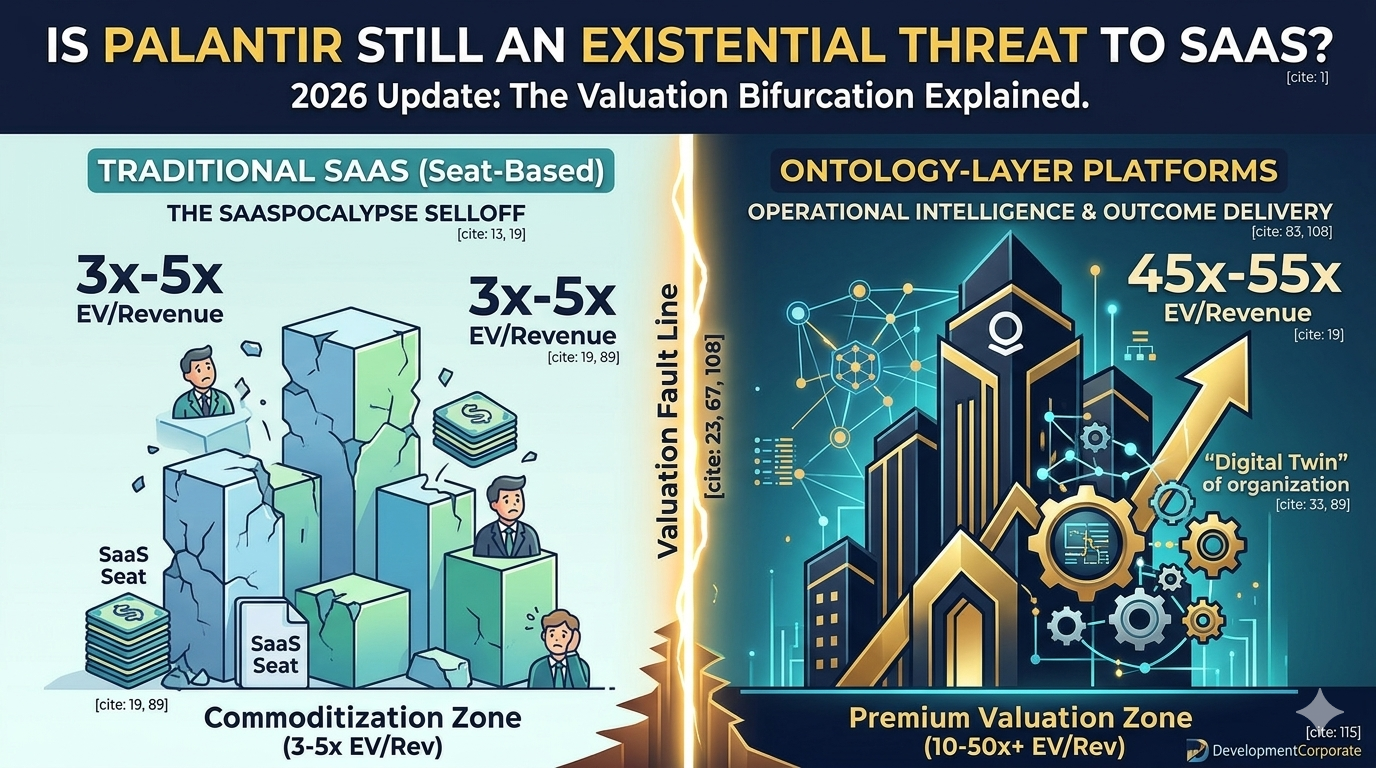

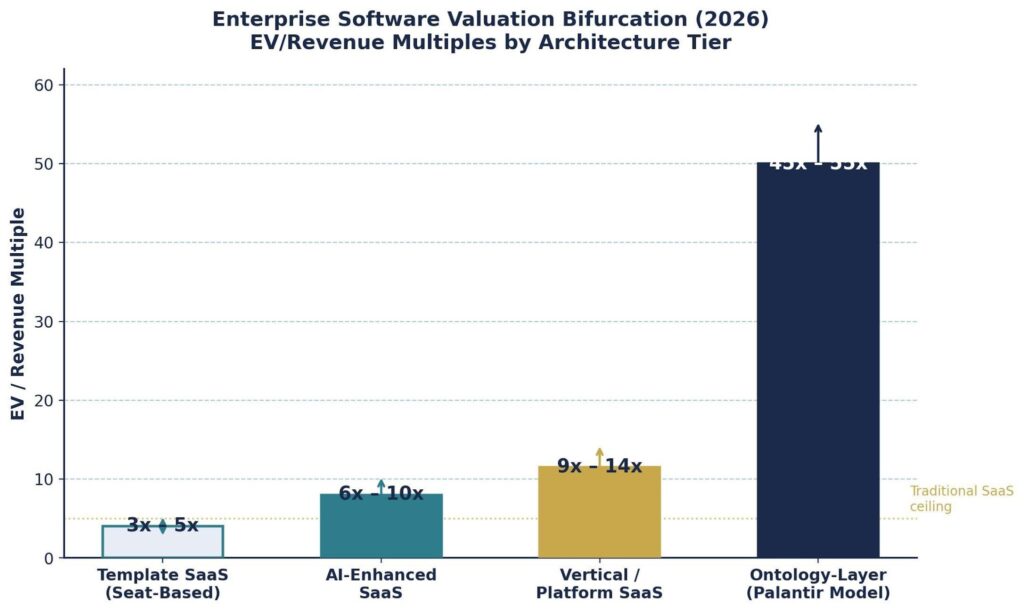

Figure 1: Enterprise Software Valuation Bifurcation (2026) — EV/Revenue multiples by architecture tier. The spread between template SaaS and ontology-layer platforms has widened in every quarter since 2023.

The Palantir Threat Is Real — Just Not for Everyone

The analytical error most commentary makes is treating “the Palantir threat” as binary. Either Palantir kills SaaS, or it doesn’t. The reality is more surgical. As our earlier analysis of the SaaS valuation bifurcation documented, the enterprise software market is splitting along a single fault line: software that gives users a place to manage work versus software that removes the work entirely.

Palantir’s deployment strategist Danny Lukus made the mechanism explicit in a Forbes piece: standard SaaS forces competitive sameness. When every company in an industry buys the same SAP module or Blue Yonder supply chain platform, no one has an advantage. Worse, when a vendor builds a custom feature for one customer, that feature becomes available to every competitor. You have paid to commoditize yourself.

The companies most exposed to this dynamic are those competing solely on template functionality at per-seat prices. The AI SaaS investment trends research confirms it: VC firms are now explicitly rejecting pitches for products that occupy “dead zones” — categories where an AI agent will soon perform the same function at a fraction of the cost. The Palantir model is not the only vector of pressure. It is the most articulate one.

The Ontology Layer: Why This Threat Does Not Fade

The most durable element of Palantir’s competitive position is architectural, not commercial. The Palantir Ontology — formalized in its Foundry platform — functions as an operational digital twin of the customer’s organization. It integrates physical assets, transactional logic, and decisional rules into a single coherent model sitting on top of existing infrastructure. The Ontology does not just connect systems. It encodes how the business actually runs.

This is the moat that standard SaaS cannot replicate. As our analysis of the a16z SaaS Moat Scorecard demonstrated using Hamilton Helmer’s Seven Powers framework, code was never the true moat in enterprise software. The moat lives in switching costs, data network effects, and embedded process scale. The Palantir Ontology delivers all three simultaneously — and it does so in a way that makes switching costs epistemic rather than merely technical. Replacing the Ontology layer means replacing the company’s operational knowledge infrastructure, not just migrating a database.

What makes this threat particularly durable is Palantir’s customer profile. Advance Auto Parts, Wendy’s, Tyson Foods, and General Mills are not technology companies experimenting with AI. They are operationally complex enterprises where supply chain execution directly drives margin. Palantir’s penetration into this segment — manufacturing now representing the largest vertical — confirms that the ontology-layer model works in production for the buyers who matter most to enterprise software M&A.

Critically, these customers are not canceling Salesforce subscriptions. They are canceling Accenture statements of work. As Visser Labs noted, Palantir is not fighting the SaaS collapse narrative — it is monetizing the layer that emerges after it. The traditional enterprise systems integrator layer, not horizontal SaaS, is the primary casualty.

Figure 2: Palantir Revenue Trajectory (Q1 2025 – Q1 2026). US commercial grew 133% YoY in Q1 2026, with full-year 2026 US commercial guidance raised to $3.224B+ (≥120% growth). Source: Palantir earnings releases.

Where the Threat Has Real Limits

Intellectual honesty requires engaging the skeptic’s case — and it is a strong one. Forbes contributor Steve Banker, the supply chain journalist who published Danny Lukus’s “SaaS is dead” argument, does not accept it uncritically. Banker’s core counterpoint: AI code generation tools can build custom workflow applications quickly, but quickly does not mean well.

Supply chain software companies like Manhattan Associates have spent decades developing mathematically sophisticated algorithms for demand forecasting, network optimization, and constraint-based scheduling. These are not UI workflows that a forward-deployed engineer can replicate with Claude and a few sprints. They are operations research problems with decades of intellectual property embedded in them.

Lukus partially concedes this. He acknowledges that most manufacturing clients deploy Palantir initially for Sales & Operations Execution — exception handling, automated responses, PO routing — rather than advanced mathematical planning. S&OE is fundamentally about workflow automation, not algorithmic sophistication. That is a significantly narrower claim than the headline implies.

The implication for M&A practitioners is critical: the Palantir threat is domain-specific. It is highest for workflow-intensive, exception-heavy operational environments. It is far lower for mathematically sophisticated planning systems, regulated data environments with deep compliance infrastructure, and products where the core value is analytical precision rather than decision automation. The 2026 SaaS benchmark data shows that companies in the latter categories are still commanding premium multiples — the selloff has not been undifferentiated.

| 🔵 INTELLIGENCE FOR PE/VC INVESTORS |

| The Palantir recovery from the 2026 selloff — 85% revenue growth, Rule of 40 of 145% — confirms the ontology-layer model is not speculative. Price it accordingly in portfolio valuations. |

| Key diligence test: Can your portfolio company articulate a differentiation story that survives the ‘template commoditization’ test? If a Palantir forward-deployed engineer could replicate the core workflow in a quarter, you have a valuation problem. |

| The AI valuation gap is real: 83% of active buyers report paying higher multiples for AI-native or AI-integrated targets, per the SEG 2026 SaaS M&A Buyers report. But the distribution is skewed — premium multiples require demonstrable customer-specific IP, not AI marketing language. |

| Palantir’s growth is concentrated in US commercial manufacturing, not enterprise SaaS categories. Your portfolio company’s exposure depends on vertical, not sector. |

| The SaaSpocalypse selloff created buying opportunities in companies with genuine ontology-layer or data-moat characteristics that were mispriced alongside the broader software correction. |

The Palantir Test: Five Questions for Every SaaS Asset

The practical implication of the Palantir threat is not a category-level verdict — it is a diligence protocol. Every enterprise software company, and every investor in one, should be able to answer these five questions. Together they determine whether the Palantir threat is existential, manageable, or largely irrelevant for a specific asset. As the AI valuation gap analysis confirms, the spread between commodity SaaS multiples and platform-tier multiples has widened in every quarter since 2023.

1. What is your differentiation story in 48 hours?

If your product management team cannot explain in 48 hours why a Palantir forward-deployed engineer could not replicate your core workflow, you have a positioning problem. The answer must be specific — proprietary data models, customer-specific decision logic, regulatory moat — not generic feature breadth.

2. How many Excel workarounds live around your product?

The Excel workaround count is a diagnostic for template fit. Every manual export, offline calculation, or spreadsheet bridge in the customer environment is evidence that the template does not match how the business actually runs. This is exactly the gap Palantir’s forward-deployed model targets. A high workaround count in a customer base is both a product weakness and a competitive vulnerability.

3. Do your switching costs survive an ontology migration?

Most SaaS switching costs are technical: data migration, integration re-wiring, retraining. These are meaningful but finite. Palantir-style switching costs are epistemic: replacing the platform means replacing the operational knowledge model of the business. If your switching costs are purely technical, they are finite. If they are epistemic — embedded decision logic, custom ontology, proprietary workflow encoding — they are structural.

4. Is your value proposition about task access or outcome delivery?

The core fault line in the 2026 SaaS go-to-market data is between products that provide access to functionality and products that deliver outcomes. If your product gives users a place to manage work and the user still makes the decision, you are in the task-access category. If your product removes the work — routes the exception, triggers the order, closes the loop autonomously — you are in the outcome-delivery category. The market is repricing the gap between them.

5. Does your AI integration add intelligence or add features?

The AI funding data from 2025–2026 shows that buyers are no longer rewarding AI as a feature. The question is whether AI integration creates structural differentiation — proprietary models trained on customer-specific data, autonomous decision loops that encode organizational logic — or whether it is a co-pilot wrapper on top of a standard template workflow. The former commands premium multiples. The latter is already being priced as a commodity.

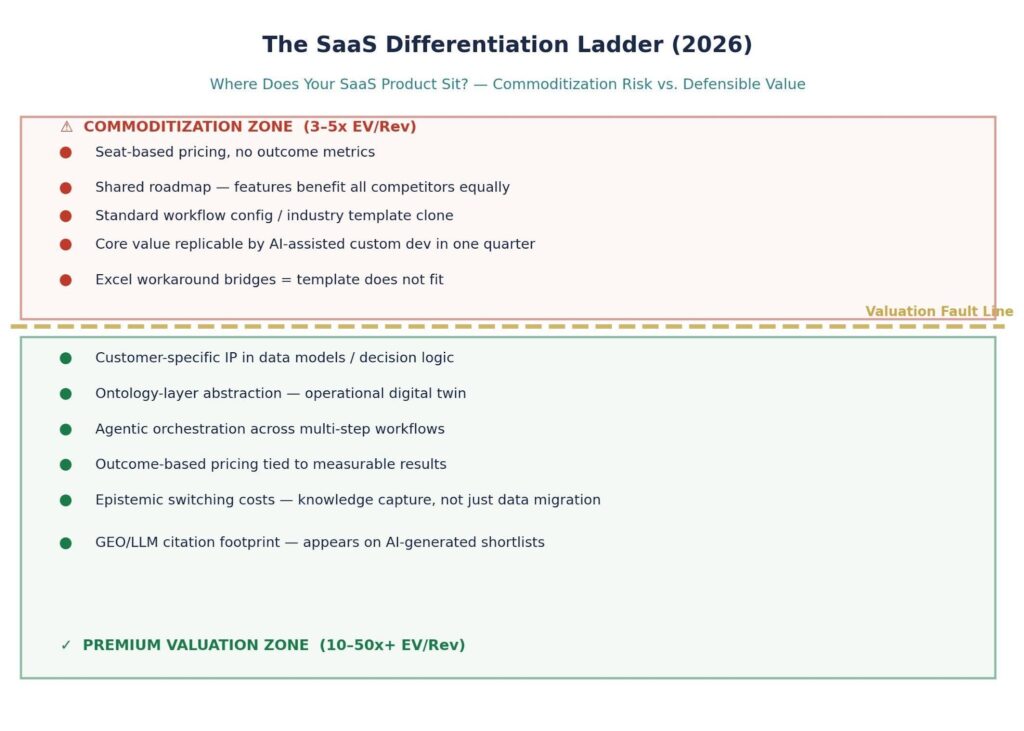

Figure 3: The SaaS Differentiation Ladder — Commoditization Risk vs. Defensible Value under the Palantir framework. Products below the fault line command premium M&A valuations; those above face continued multiple compression regardless of AI feature additions.

| 🟡 INTELLIGENCE FOR SAAS FOUNDERS PREPARING FOR EXIT |

| The Palantir threat is not symmetrical. It does more damage to some SaaS companies and creates positioning opportunities for others. Know which side you are on before entering an exit process. |

| If your product encodes customer-specific business logic, proprietary data models, or deep integration with operational decision cycles, you may be sitting on undervalued infrastructure that the current market is mispricing. |

| The most durable exit story in 2026: ‘We are the system of record for a workflow that matters, and switching means dismantling operational knowledge — not just migrating data.’ This is the framing that commands premium multiples. |

| Template commoditization lands hardest on shared feature roadmaps, seat-based pricing without outcome metrics, and tools that sit alongside Excel rather than replacing it. Audit your product against all three before setting valuation expectations. |

| Palantir’s commercial customer base — Advance Auto Parts, Tyson Foods, Wendy’s — signals where ontology-layer competition is real. If your vertical serves operationally complex enterprises in manufacturing, distribution, or supply chain, the competitive analysis is not theoretical. |

The Verdict: Existential for Some, Irrelevant for Others

Palantir is not an existential threat to SaaS as a category. It is an existential threat to a specific stratum of SaaS — the template-based, seat-licensed, shared-roadmap layer that competes on feature breadth rather than embedded intelligence. That stratum is larger than most M&A models currently price in. As the SaaSpocalypse buyings signal analysis noted, agentic AI deployment at enterprise scale is still 18–36 months away from widespread operational reality — but the valuation repricing is happening now. Markets do not wait for deployment.

Palantir’s Q1 2026 performance — the fastest revenue growth in its history as a public company, a Rule of 40 score matched only by semiconductor infrastructure leaders, and $4.2–4.4 billion in full-year free cash flow guidance — is not a speculative thesis. It is an executed business model. The selloff was a misjudgment, not a signal of structural fragility. The recovery confirms it.

For enterprise software companies and their investors, the actionable conclusion is straightforward. The Palantir threat is not a macro verdict on the sector. It is a due diligence instrument. Apply the five-question framework above to every asset in the portfolio. The companies that score well — customer-specific IP, epistemic switching costs, outcome-based pricing, agentic workflow automation — will trade at infrastructure multiples regardless of what happens to template SaaS valuations. The companies that score poorly have a positioning problem that AI feature announcements will not solve.

| 🔵 INTELLIGENCE FOR ENTERPRISE CTOs & CPOs |

| The Palantir test is also a vendor evaluation instrument. Before your next ERP or SCM renewal, run a differentiation audit: which capabilities give your supply chain a competitive advantage that your current platform cannot encode? |

| Apply the Excel workaround test to your current software stack. Each manual data export or spreadsheet bridge is evidence the template does not fit — and a signal of where ontology-layer value is highest. |

| Palantir’s commercial wins are concentrated in S&OE (Sales & Operations Execution) — exception handling, PO routing, stock-check automation — not advanced mathematical planning. Evaluate AI vendor claims accordingly. |

| GEO/LLM citation footprint is now a software selection variable. Vendors with strong LLM visibility appear on AI-generated shortlists that competitors miss. Factor this into vendor evaluation methodology. |

| The API gating risk is real: if your agent-based workflows depend on SaaS vendor API openness, you carry a structural fragility that Palantir’s data-layer integration model sidesteps entirely. |

The Bottom Line

The Palantir selloff changed the narrative. The Palantir recovery changed it back. What remains constant is the structural reality: a valuation fault line now divides enterprise software between companies that access workflow and companies that encode operational intelligence. The former faces sustained multiple compression. The latter commands infrastructure-tier multiples regardless of market sentiment cycles.

The question every enterprise software company — and every investor in one — needs to answer is not “is SaaS dead?” It is: “where does our product sit on the differentiation ladder, and what is that position worth in the next deal?” If you do not yet have a clear answer, that is itself an answer. Schedule a confidential conversation with DevelopmentCorporate to apply this framework to your specific asset.

About the Author

John Mecke is Managing Director of DevelopmentCorporate LLC, an M&A advisory firm specializing in enterprise SaaS transactions. With 30+ years of enterprise software experience and $175M+ in completed acquisitions, DevelopmentCorporate helps founders, PE sponsors, and enterprise buyers navigate valuation strategy, competitive positioning, and exit planning.