The AI Capex Credit Cycle: Why 2008 — Not 2000 — Is the M&A Playbook

The AI capex credit cycle is being misdiagnosed by almost everyone arguing about it. The bulls point to record revenue levels and exploding backlogs. The bears point to unsustainable valuations. Both are answering the question “is this 2000 again?” — and according to a widely circulated July analysis from Groundbreaker Research, that is the wrong question entirely. The financing architecture underneath the AI build-out doesn’t resemble the dot-com equity bubble. It resembles the 2008 subprime credit machine — and credit machines don’t break when demand collapses. They break when growth merely decelerates.

For M&A practitioners, this distinction is not academic. It determines when the repricing arrives, which assets it hits first, and what diligence must look like between now and then. We have been documenting the downstream version of this thesis for months — in the collapse of ARR-based lending and JPMorgan’s preemptive software loan markdowns. The Groundbreaker piece supplies the macro architecture those signals plug into. This article translates it into deal terms.

The Bubble Debate Is Arguing About the Wrong Derivative

Groundbreaker’s framework rests on three numbers that describe any growing quantity: the level (how big it is), the first derivative (how fast it’s growing), and the second derivative (whether that growth is accelerating or decelerating). Markets are instrumented to watch the first two. Sell-side models forecast levels; momentum strategies trade velocity. Almost nothing is built to watch acceleration — which is precisely where regime change first becomes visible.

The 2008 analogy is the proof case. The popular memory holds that home prices fell, so borrowers defaulted. The sequence was actually the reverse: subprime delinquencies inflected upward in 2006, while national home prices were at all-time highs and still rising. What had changed was the rate of appreciation — it had decelerated. The 2/28 hybrid ARM was a refinancing treadmill powered by acceleration, and when appreciation slowed, the treadmill failed a full year before prices declined. Economist Didier Sornette made the point that treating the price decline as an external shock gets the mechanics backwards: the deceleration was generated inside the structure itself.

The lesson: any financing structure whose serviceability depends on refinancing into growth does not need a downturn to break. It needs only a slowdown in the growth rate. Everything looks fine in the window between the second derivative rolling over and the first derivative hitting zero — record revenue, positive growth, triumphant press releases — while the structure underneath is already broken.

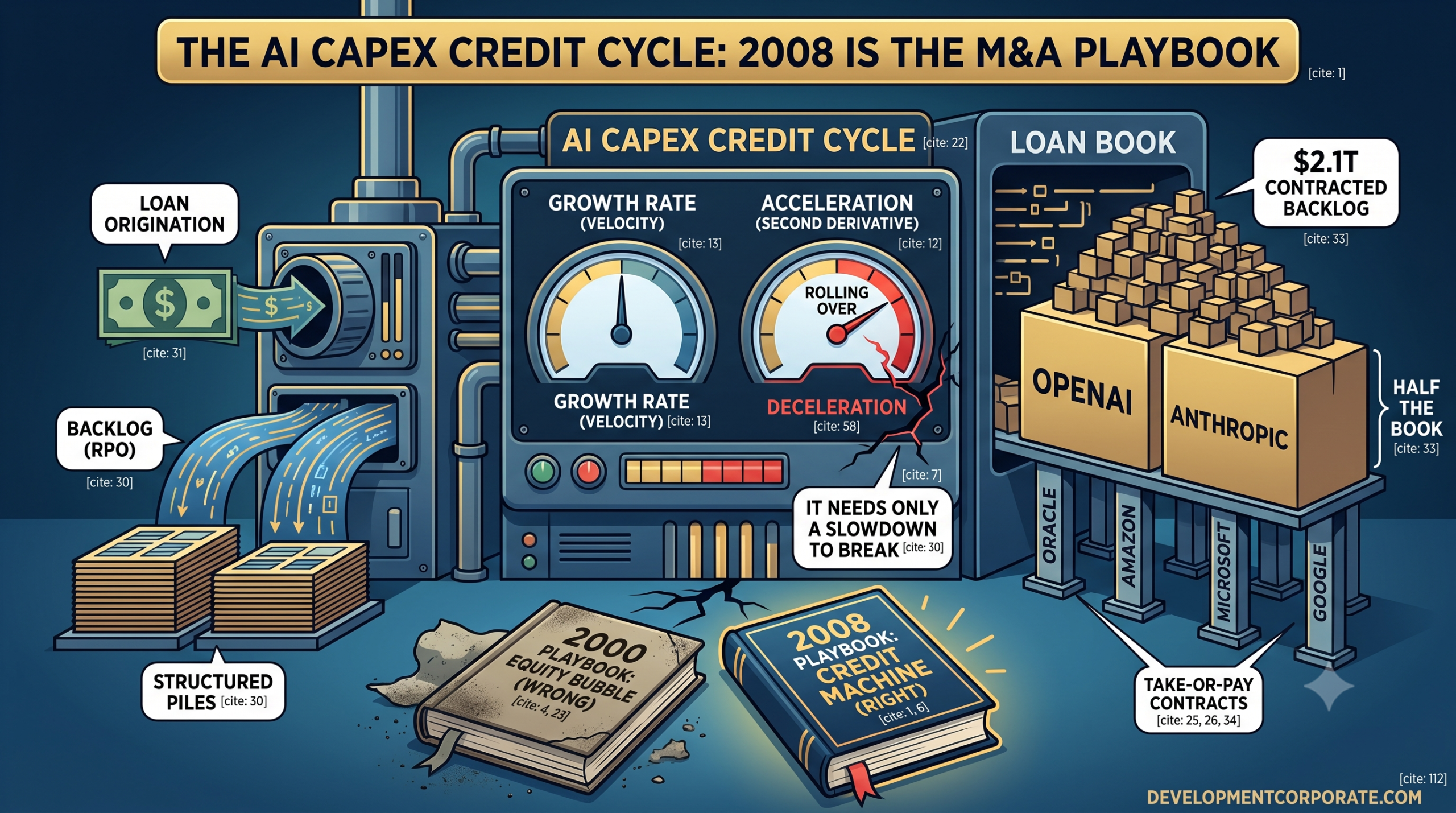

The AI Capex Credit Cycle Runs on a Loan Book Nobody Calls a Loan Book

The reason the 2000 analogy fails is that the dot-com era was an equity event: overpriced stocks, thin balance sheets, almost no debt. Equity is patient — it can de-rate slowly and recover. The AI build-out is financed differently: take-or-pay capacity contracts, GPU-collateralized term loans, off-balance-sheet vehicles, and asset-backed notes sold to insurers. In Groundbreaker’s words, this is “a real estate business that happens to compute” — debt-financed construction, leases disguised as contracts, and long build lags that guarantee supply lands after demand turns.

Reduce a frontier-lab compute contract to its skeleton and it is a loan. The provider — Oracle, CoreWeave, a hyperscaler — advances capital in kind (a building full of chips) against the lab’s multi-year commitment to pay. The data center is the collateral; the contracted payments are the debt service. The provider books the promise as remaining performance obligation (RPO), reports it to Wall Street as demand visibility, and borrows against it to build more. Capex, in this reading, is origination volume.

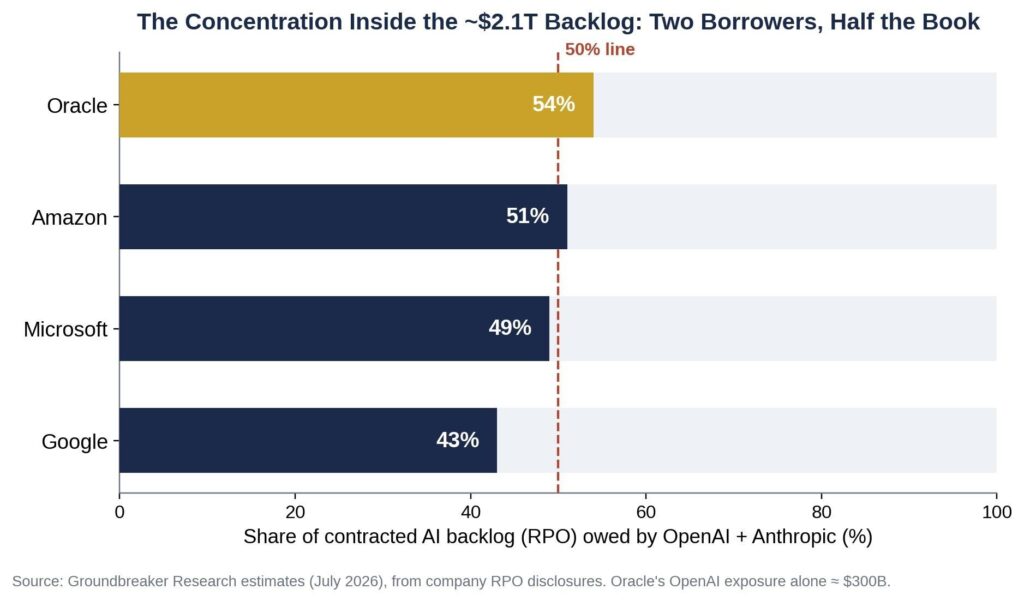

The credit quality of that book is the number that matters. Groundbreaker estimates roughly $2.1 trillion in aggregate contracted backlog across the four big platforms — and about half of it owed by just two borrowers, OpenAI and Anthropic. By its estimates, roughly 54% of Oracle’s book, 51% of Amazon’s, 49% of Microsoft’s, and 43% of Google’s traces to these two names. Moody’s corroborates the direction: hyperscalers added roughly $700 billion in RPOs over just two quarters, with much of the growth attributed to OpenAI and Anthropic. Wall Street prices this backlog as diversified forward revenue. In economic substance, it is a concentrated credit facility extended to tenants — one of which has no operating income to service it.

Figure 1: Estimated share of each platform’s contracted AI backlog owed by OpenAI and Anthropic. Source: Groundbreaker Research estimates, July 2026.

| FOR PE/VC INVESTORSThe RPO concentration data reframes portfolio exposure mapping. If the backlog is a loan book, your AI-adjacent positions are credit positions:Map look-through exposure: any portfolio company whose revenue depends on hyperscaler capex — directly or one counterparty removed — carries OpenAI refinancing risk it never underwrote.Credit reprices before equity. The 6–18 month lag we documented in ARR lending applies here at macro scale: GPU-backed paper and neocloud debt will signal before software multiples move.The distressed opportunity is real: stranded data center capacity and orphaned AI assets will clear at deep discounts if the reflexive flip arrives. Dry powder positioned for that scenario buys at pennies. |

OpenAI Is the Borrower Whose Markup Is the Cash Flow

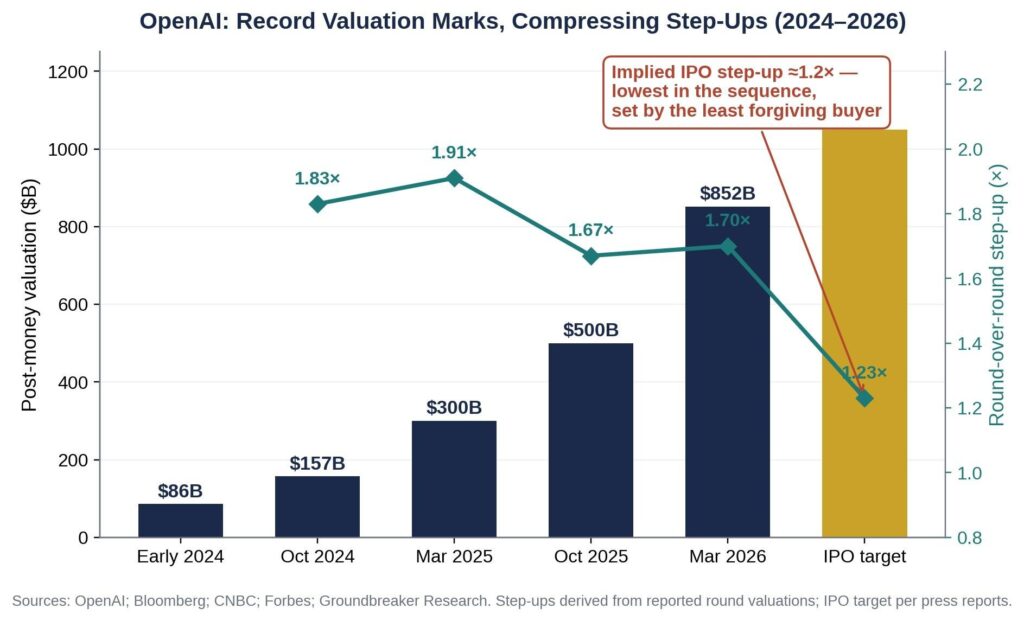

Every subprime cycle has a borrower who can only refinance, never repay. Groundbreaker’s candidate is OpenAI — and the reported numbers make the case uncomfortable to dismiss. The company closed a $122 billion round at an $852 billion post-money valuation in March 2026, anchored by Amazon ($50B), Nvidia ($30B), and SoftBank ($30B) — the same counterparties whose compute the proceeds will buy. Revenue is real and large — roughly $2 billion per month — but the company remains unprofitable, with 2026 cash burn estimates running from $14 billion to $27 billion depending on the source, against compute commitments in the hundreds of billions.

Because those commitments cannot be serviced from earnings, they are serviced from financing — and financing for a borrower in this position is available on one condition: each round must price above the last. The valuation markup is not a scorecard; it is the funding event itself. Measured as levels, OpenAI’s marks are the most remarkable appreciation in private-market history: roughly $86 billion in early 2024, then $157 billion, $300 billion, $500 billion, and $852 billion. Measured as rates of change, the same series inverts: step-ups of roughly 1.8× and 1.9× compress to 1.7×, and the implied step-up to the reported $1 trillion IPO target is barely 1.2× — the lowest in the sequence, and the one set by the deepest, least forgiving pool of capital.

Figure 2: OpenAI’s valuation marks keep printing records while round-over-round step-ups compress toward the public-market hurdle. Sources: OpenAI, Bloomberg, CNBC, Forbes; step-ups derived.

Two corroborating signals landed this spring. First, OpenAI confidentially filed its S-1 in June but is reportedly leaning toward a 2027 listing — a delay that is hard to explain if the mark clears easily. Second, and more telling: Microsoft restructured its OpenAI agreement in April 2026, ending exclusivity, ending its own revenue-share payments to OpenAI, and — per its own 10-Q — having already surrendered its right of first refusal on compute in October 2025. Microsoft kept its ~27% equity upside while shedding structural entanglement with OpenAI’s obligations. The most informed counterparty in the complex — the one that saw the books from inside — is behaving like a lender shortening duration.

| The most informed counterparty in the AI complex is behaving like a lender shortening duration on a borrower it has decided not to underwrite. |

The Second Derivative of AI Capex Has Already Rolled Over

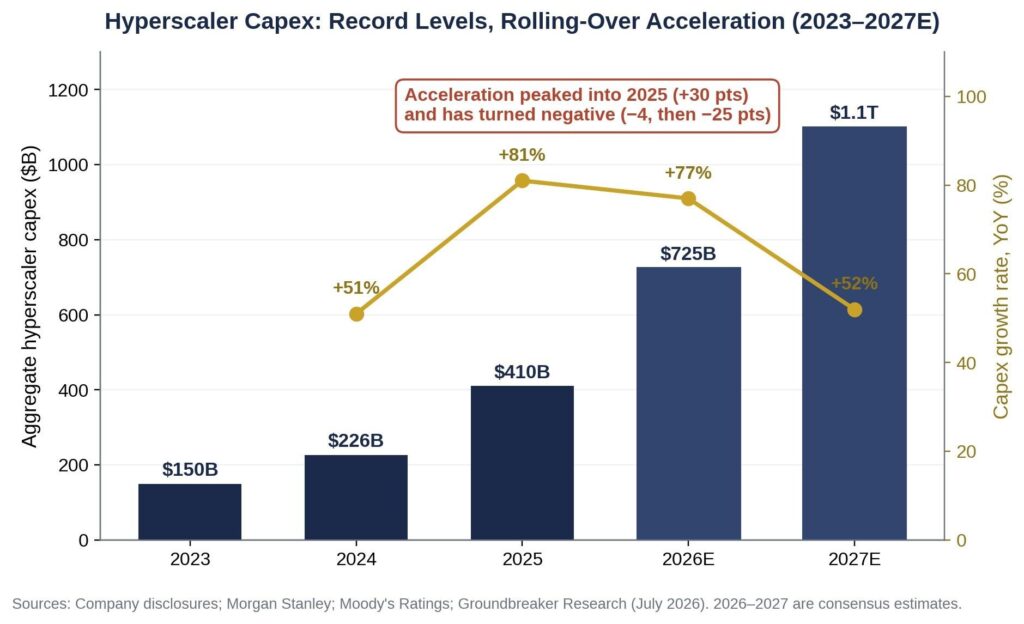

Here is the arithmetic the level-watchers miss. Aggregate hyperscaler capex ran roughly $150 billion in 2023, $226 billion in 2024, $410 billion in 2025, with 2026 guidance around $725 billion and Morgan Stanley projecting $1.1 trillion for 2027. As levels, these are records — the largest private capital-formation event in history. As growth rates, they read +51%, +81%, +77%, +52%. As acceleration, the series peaked at roughly +30 percentage points into 2025 and has turned negative: about −4 points, then roughly −25. The level is at records. The velocity is high. The acceleration — the number the entire financing architecture is a bet on — has already rolled over.

Figure 3: Hyperscaler capex levels keep setting records while the growth rate — and especially its acceleration — has already peaked. Sources: company disclosures; Morgan Stanley; Moody’s; Groundbreaker Research.

There is a recursion inside these numbers that makes the second derivative even more important: hyperscaler capex is not merely a response to AI demand — to a substantial degree it is the demand. Frontier-lab revenue is heavily hyperscaler spending recycled through cloud credits and compute commitments; Nvidia’s revenue is hyperscaler capex; the neoclouds’ revenue is hyperscaler capex, levered. Meanwhile, capex as a share of operating cash flow has climbed from ~30% in 2022 to ~60% in 2025, with consensus crossing 100% in 2026 — the point past which every marginal gigawatt is funded from the balance sheet, not from operations. Morgan Stanley pegs hyperscaler gross leverage at roughly 1.8 turns, double a year ago and now above the entire energy sector.

Groundbreaker’s sharpest observation is game-theoretic: the capex arms race holds only while the market rewards spending. The moment a hyperscaler announces a capex cut and its multiple expands on the news, every payoff on the board rewrites, and the equilibrium flips from “everyone spends” to “everyone cuts” — discontinuously, because it is a coordination game. In the boom regime, a take-or-pay contract is an asset to everyone who touches it. In the repriced regime, the identical contract is a liability to all of them simultaneously. Nothing physical has to break; the market only has to change its mind.

What the AI Credit Cycle Means for SaaS M&A

Groundbreaker writes for macro allocators. Our readers price companies. Three translation layers connect the second-derivative thesis to the deals crossing our desk right now.

1. The repricing arrives through credit before equity — and it already has

The most striking thing about the second-derivative framework is that the SaaS market has already run the experiment one level down. Private credit lenders abandoned ARR-based underwriting in early 2026 — all eight of Lincoln International’s early-2026 software loans priced on EBITDA — and JPMorgan marked down its software book preemptively, before defaults, on valuation logic alone. Both moves were driven by the same insight Groundbreaker formalizes: recurring-revenue durability is a growth-rate assumption wearing a level costume. Credit repricing has led equity M&A repricing by 6–18 months in every cycle we track. The AI capex credit cycle simply runs this sequence at civilization scale — and the credit leg has already begun moving.

2. AI-exposed ARR is the retail version of subprime RPO

A hyperscaler booking OpenAI take-or-pay commitments as backlog and a SaaS seller presenting seat-based ARR as durable collateral are making the same category error at different scales: both treat a growth-dependent promise as a bankable asset. As we argued in our analysis of Gartner’s $234 billion agentic AI exposure forecast, seat-derived ARR is a claim about the past, not a forecast of durable cash flow, once agents decouple usage from headcount. The 2026 benchmark data already shows seat-based pricing models posting sub-100% net revenue retention. If the macro deceleration Groundbreaker describes arrives, enterprise AI budgets — the marginal dollar funding a large share of SaaS expansion revenue — tighten first. Sellers whose growth story leans on AI-driven expansion are carrying second-derivative risk on their own cap table.

3. Counterparty look-through becomes standard diligence

The RPO concentration analysis — half of $2.1 trillion owed by two names — is a template for a diligence discipline the mid-market has never needed: tracing revenue quality through to the ultimate funding source. A vertical SaaS company selling into neoclouds, GPU brokers, AI-native startups, or data-center construction is, in look-through terms, an OpenAI creditor. The roll-up reset that took E2open out at 3.4× showed how brutally buyers now discount revenue whose durability they cannot verify. Expect the same discount to reach any book of business whose customers are funded by the AI capex machine rather than by their own operating cash flow.

| FOR SAAS FOUNDERSIf you are 12–24 months from a process, the second-derivative thesis changes your preparation, whether or not the crash arrives:Segment your ARR by funding source. Revenue from customers who are themselves venture-funded AI companies will be diligenced as credit exposure, not recurring revenue. Know that number before your buyer computes it.Stress-test expansion revenue against a 2027 AI budget freeze. Growth that survives the scenario is the growth a buyer will pay for.Decelerating growth at a high level is worth less than modest growth that is stable. Buyers now read the trajectory, not the print — sequence your exit before your own second derivative goes visibly negative. |

A Diligence Framework for the Deceleration Regime

Whether Groundbreaker’s break arrives in quarters or years — and the author concedes the timing is unknowable — the framework converts directly into diligence questions that cost nothing to ask now and are expensive to skip later.

Backlog quality over backlog size. Any target presenting contracted backlog, RPO, or multi-year commitments as demand proof should face the credit question: what is the standalone creditworthiness of the counterparties, and what fraction can service the commitment from operating cash flow rather than from future fundraising? A commitment is worth the credit of the entity behind it — nothing more.

Second-derivative reporting. Ask for growth-rate trajectories, not growth rates — quarterly sequential trends in new-logo ARR, expansion revenue, and pipeline creation. As we documented in our analysis of manufactured margins, the benchmark data cannot distinguish durable improvement from window dressing; the trajectory usually can.

Moat verification under deceleration. In a decelerating regime, the spread between AI-defensible and AI-exposed assets — the bifurcation at the center of our moat scorecard framework — widens from a valuation preference into a financeability line. Companies with proprietary data and embedded workflows stay transactable; generic functionality does not.

Operational earnings floor. The operational-alpha shift in private equity means buyers now underwrite EBITDA they can verify, not ARR they must trust. A deceleration regime accelerates that migration. Sellers should arrive with normalized, accrual-based earnings and evidence that margin came from operating leverage.

| FOR ENTERPRISE CTOs & CPOsThe credit-cycle reading of AI infrastructure has direct vendor-risk implications for your 2026–2027 planning:Underwrite your AI vendors like counterparties. A neocloud or AI-native vendor dependent on continuous fundraising can disappear mid-contract; demand escrow, portability, and data-egress terms accordingly.The deceleration scenario is a buyer’s market for compute. If the reflexive flip arrives, inference and capacity pricing fall hard — avoid long-duration commitments signed at boom-regime prices.Multi-vendor architecture is now a balance-sheet hedge, not just a technical one. Microsoft’s own shift to shorter-duration compute agreements is the reference behavior. |

The Bottom Line

The market is making three stacked errors, per Groundbreaker: pricing AI as a technology cycle when its financing is credit-and-real-estate machinery; watching levels and velocity while the structure breaks on acceleration; and treating a concentrated single-borrower loan book as diversified forward demand. Each alone might be survivable. Together they reconstruct the anatomy of 2008 — negative convexity, originate-to-distribute plumbing, and a correlation of one hiding inside apparent diversification.

We would add a fourth error, specific to our market: assuming the repricing will announce itself before it reaches the mid-market. It will not. It will arrive the way it always does — through lender behavior, through diligence questions that didn’t exist last cycle, and through a widening bid-ask spread on any asset whose growth story depends on someone else’s ability to refinance. The credit market has already started asking those questions. The equity M&A market has 6–18 months to catch up.

The structure does not need a crash. It needs only a deceleration — and the deceleration is already in the data.

Preparing to buy or sell an enterprise software company in a repricing market? DevelopmentCorporate advises PE firms, founders, and corporate development teams on SaaS M&A strategy, valuation, and diligence. Contact us at developmentcorporate.com.